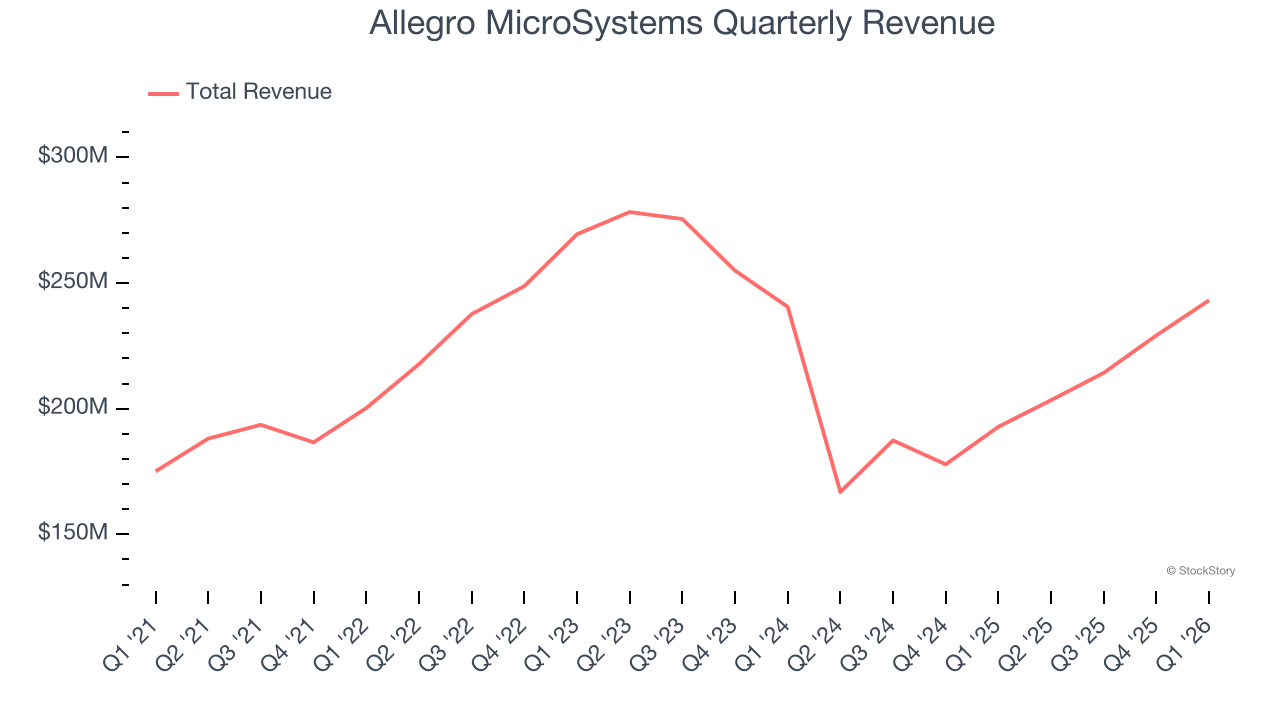

Chip designer Allegro MicroSystems (NASDAQ:ALGM) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 26.1% year on year to $243.2 million. Guidance for next quarter’s revenue was better than expected at $250 million at the midpoint, 1.9% above analysts’ estimates. Its GAAP loss of $0.09 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Allegro MicroSystems? Find out by accessing our full research report, it’s free.

Allegro MicroSystems (ALGM) Q1 CY2026 Highlights:

- Revenue: $243.2 million vs analyst estimates of $235.5 million (26.1% year-on-year growth, 3.2% beat)

- EPS (GAAP): -$0.09 vs analyst estimates of $0.05 (significant miss)

- Adjusted EBITDA: $49.69 million vs analyst estimates of $55.43 million (20.4% margin, 10.4% miss)

- Revenue Guidance for Q2 CY2026 is $250 million at the midpoint, above analyst estimates of $245.4 million

- EPS (GAAP) guidance for Q2 CY2026 is $0.21 at the midpoint, beating analyst estimates by 129%

- Operating Margin: 2.2%, up from -6.8% in the same quarter last year

- Free Cash Flow Margin: 7.7%, similar to the same quarter last year

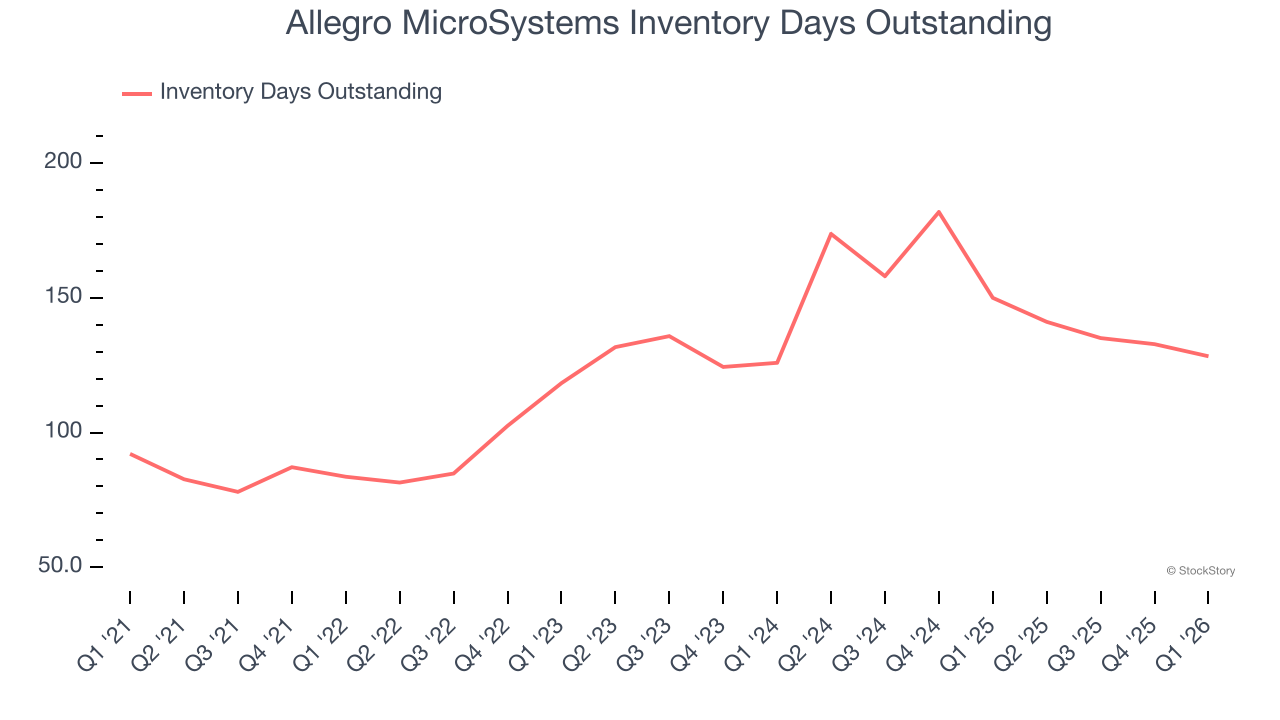

- Inventory Days Outstanding: 128, down from 133 in the previous quarter

- Market Capitalization: $9.52 billion

“We finished fiscal year 2026 with strong momentum, delivering a fifth consecutive quarter of sales growth at $243 million. Non-GAAP EPS nearly tripled year-over-year to $0.17. For the full year, sales grew 23% to $890 million and non-GAAP EPS more than doubled to $0.54. These results reflect strength in Focus Auto sales - including xEV and ADAS – and Data Center, which reached a record 14% of total Q4 sales,” said Mike Doogue, President and CEO of Allegro MicroSystems.

Company Overview

The result of a spinoff from Sanken in Japan, Allegro MicroSystems (NASDAQ:ALGM) is a designer of power management chips and distance sensors used in electric vehicles and data centers.

Revenue Growth

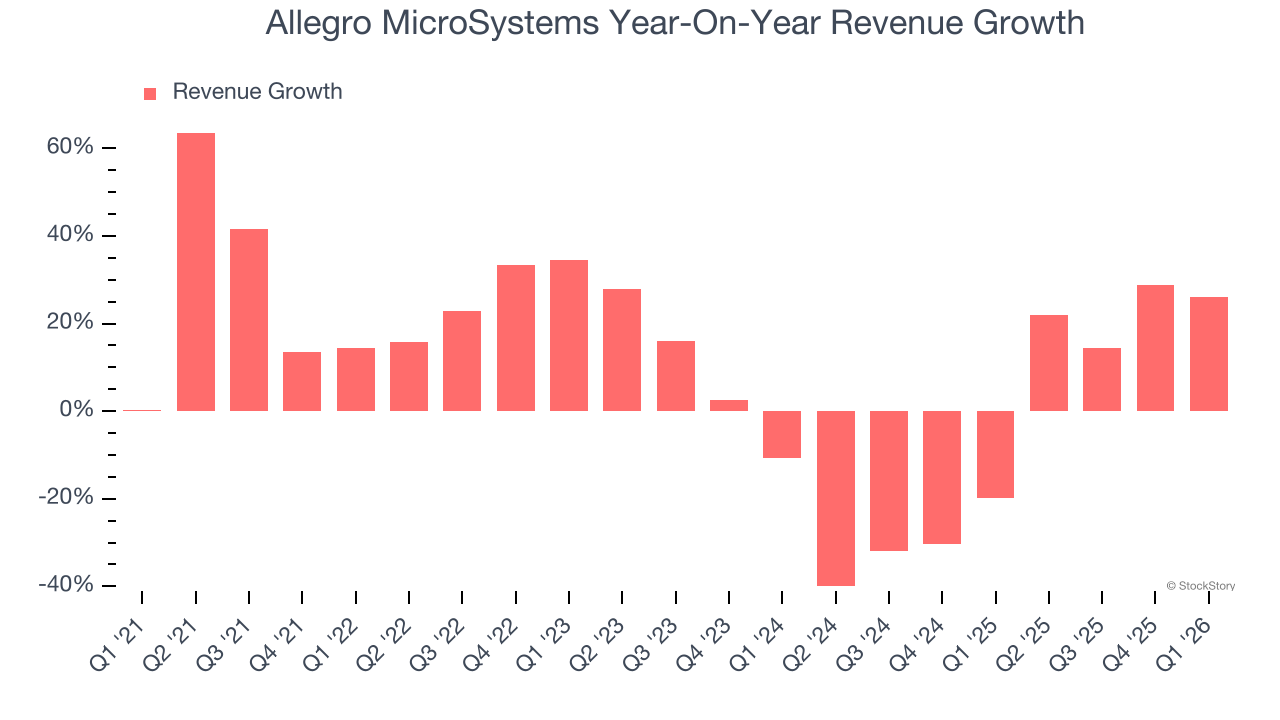

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, Allegro MicroSystems’s sales grew at a decent 8.5% compounded annual growth rate over the last five years. Its growth was slightly above the average semiconductor company and shows its offerings resonate with customers. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

We at StockStory place the most emphasis on long-term growth, but within semiconductors, a half-decade historical view may miss new demand cycles or industry trends like AI. Allegro MicroSystems’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 7.9% over the last two years.

This quarter, Allegro MicroSystems reported robust year-on-year revenue growth of 26.1%, and its $243.2 million of revenue topped Wall Street estimates by 3.2%. Beyond the beat, this marks 4 straight quarters of growth, implying that Allegro MicroSystems is in the middle of its cycle - a typical upcycle generally lasts 8-10 quarters. Company management is currently guiding for a 22.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 16.5% over the next 12 months. Although this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Allegro MicroSystems’s DIO came in at 128, which is 6 days above its five-year average. These numbers suggest that despite the recent decrease, the company’s inventory levels are higher than what we’ve seen in the past.

Key Takeaways from Allegro MicroSystems’s Q1 Results

It was encouraging to see Allegro MicroSystems beat analysts’ revenue expectations this quarter. We were also happy its adjusted operating income outperformed Wall Street’s estimates. On the other hand, its EPS missed. Zooming out, we think this was a mixed quarter. The market seemed to be hoping for more, and the stock traded down 4.8% to $48.89 immediately following the results.

Big picture, is Allegro MicroSystems a buy here and now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).