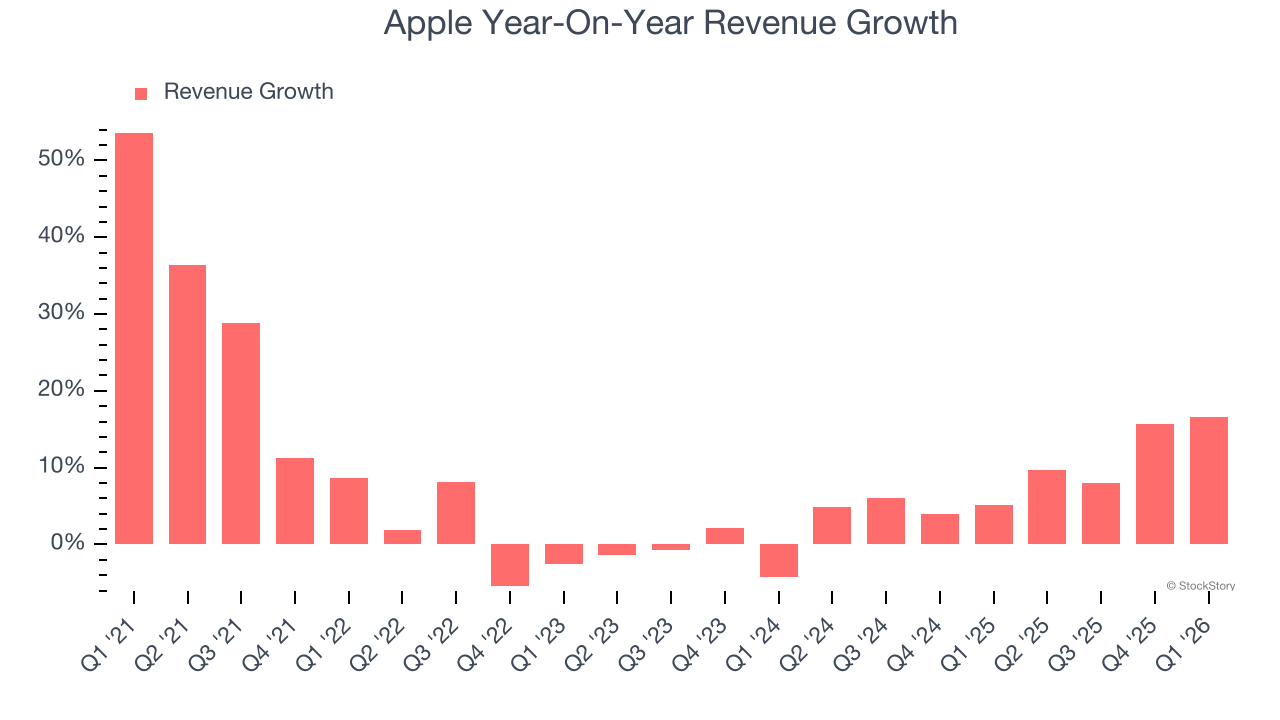

iPhone and iPad maker Apple (NASDAQ:AAPL) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 16.6% year on year to $111.2 billion. Its GAAP profit of $2.01 per share was 3.6% above analysts’ consensus estimates.

Is now the time to buy Apple? Find out by accessing our full research report, it’s free.

Apple (AAPL) Q1 CY2026 Highlights:

- Revenue: $111.2 billion vs analyst estimates of $109.3 billion (1.7% beat)

- iPhone revenue missed, but Services revenue beat

- EPS (GAAP): $2.01 vs analyst estimates of $1.94 (3.6% beat)

- Guidance: AAPL said on the earnings call that revenue in the June quarter will increase between 14% and 17% year-on-year, better than analysts expectations of 10% growth

- Gross Margin: 49.3%, up from 47.1% in the same quarter last year (beat)

- Operating Margin: 32.3%, up from 31% in the same quarter last year

- Free Cash Flow Margin: 24%, up from 21.9% in the same quarter last year

- Market Capitalization: $3.97 trillion

Revenue Growth

Although Apple - with its installed base of 2 billion+ devices - displayed epic growth in its early days, its scale has begun to weigh on its expansion. The company’s revenue has only grown at a mediocre 6.8% annualized rate over the last five years, reaching $451.4 billion in the last year. This performance shows its market is maturing and that it must find a new hit product or service to re-accelerate growth.

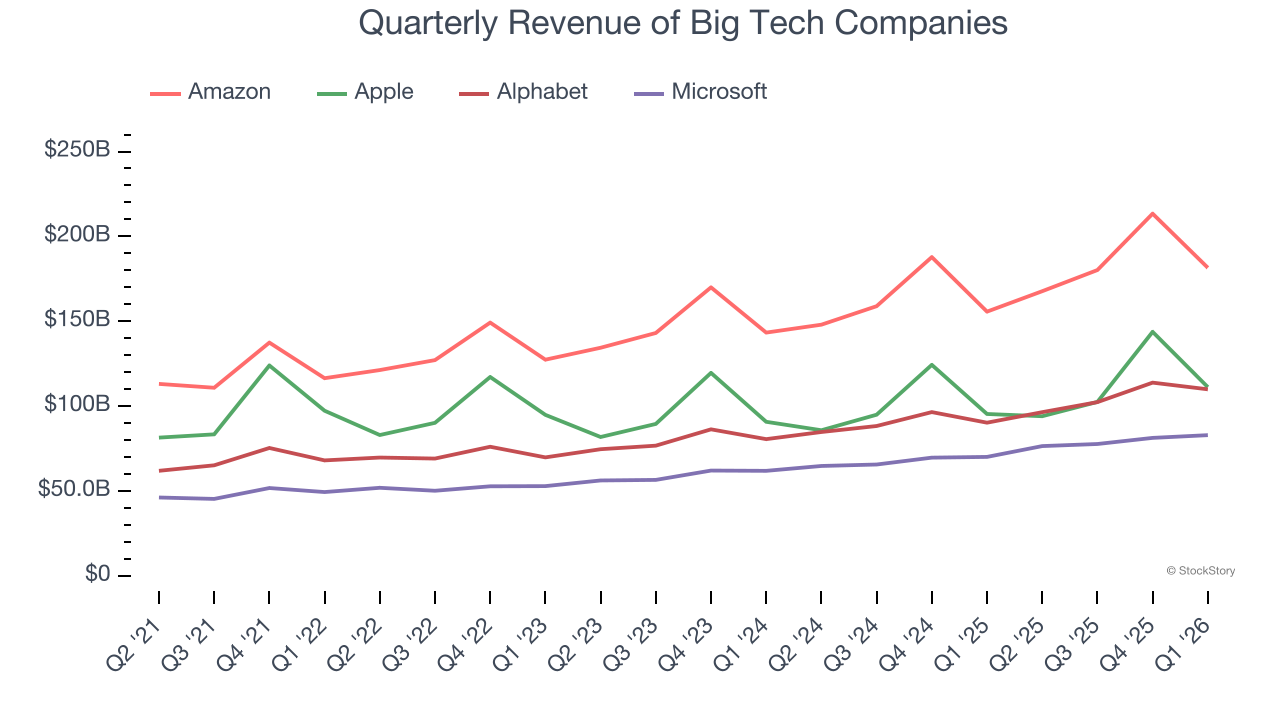

Apple’s growth over the same period also trailed its big tech peers, Amazon (12.1%), Alphabet (16.5%), and Microsoft (14.8%) over the same period. This is an important consideration because investors often use the comparisons as a starting point for their valuations. When adjusting for these benchmarks, we think Apple is a bit expensive.

Long-term growth reigns supreme in fundamentals, but for big tech companies, a half-decade historical view may miss emerging trends in AI. Apple’s annualized revenue growth of 8.8% over the last two years is above its five-year trend, suggesting some bright spots.

This quarter, Apple reported year-on-year revenue growth of 16.6%, and its $111.2 billion of revenue exceeded Wall Street’s estimates by 1.7%. Looking ahead, sell-side This projection illustrates the market sees limited near-term success for its newer AI-enabling products.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

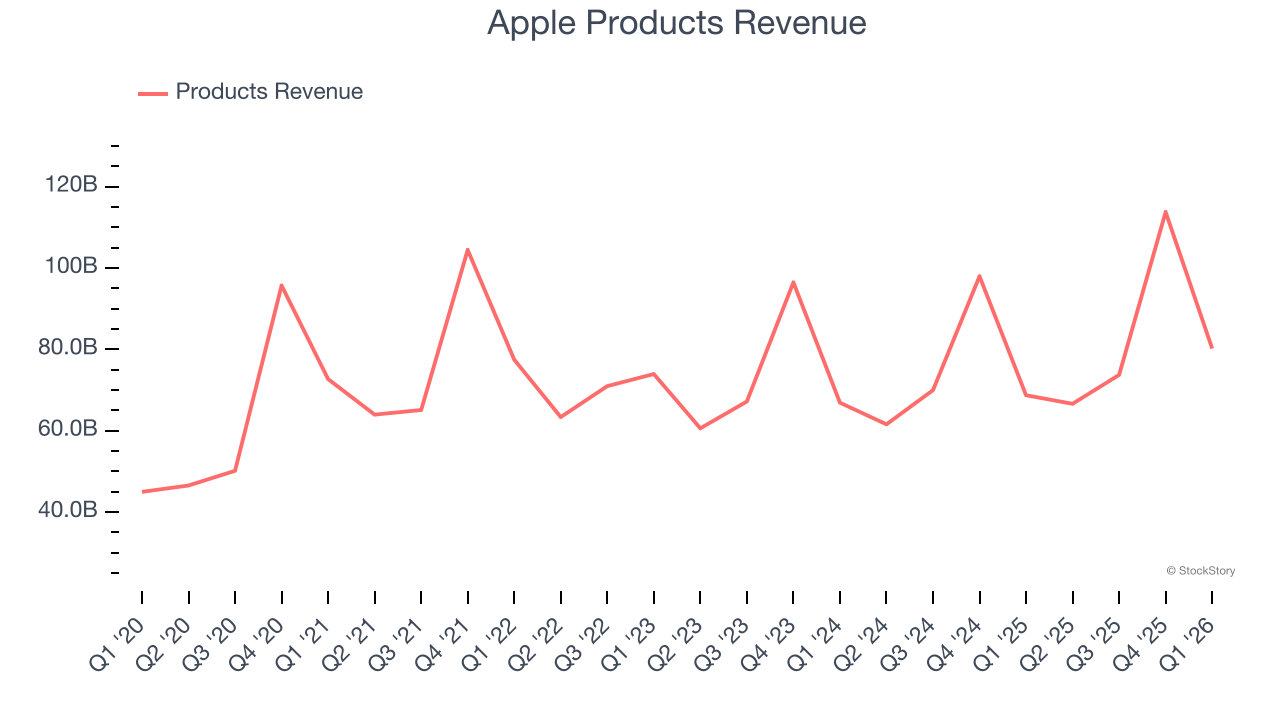

Products: Steve Jobs’s Legacy

Apple’s Products segment includes everything from its flagship iPhone, iPad, and MacBook computers to AirPods and Apple Watch. We are closely monitoring whether the GenAI-powered Apple Intelligence, which was released in September 2024 but has limited interoperability with older devices, can spur an upgrade cycle for the company.

Products sales are by far the biggest chunk of Apple’s revenue at 74%, and they grew by 4.8% annually over the last five years, slower than total revenue. Recently, sales have accelerated, growing at an annual clip of 7.2% over the last two years.

This quarter, Products sales were up 16.7% year on year. Holding aside expectations, the recently improving rate of change shows that more customers are upgrading their devices than before. We’ll be watching to see if Apple Intelligence and iOS 18 can accelerate this trend. Wall Street seems to believe it won't move the needle.

Key Takeaways from Apple’s Q1 Results

It was encouraging to see Apple beat analysts’ revenue expectations this quarter. We were also happy its EPS outperformed Wall Street’s estimates. On the earnings call, management guided to EPS growth next quarter above expectations. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 3.4% to $280.87 immediately following the results.

Apple put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).