Video sharing platform Rumble (NASDAQGM:RUM) reported Q1 CY2025 results exceeding the market’s revenue expectations, with sales up 33.7% year on year to $23.71 million. Its GAAP loss of $0.01 per share was 90% above analysts’ consensus estimates.

Is now the time to buy Rumble? Find out by accessing our full research report, it’s free.

Rumble (RUM) Q1 CY2025 Highlights:

- Revenue: $23.71 million vs analyst estimates of $22.77 million (33.7% year-on-year growth, 4.1% beat)

- EPS (GAAP): -$0.01 vs analyst estimates of -$0.10 (90% beat)

- Adjusted EBITDA: -$22.71 million vs analyst estimates of -$16.51 million (-95.8% margin, 37.5% miss)

- Operating Margin: -153%, up from -190% in the same quarter last year

- Free Cash Flow was -$14.63 million compared to -$34.28 million in the same quarter last year

- Market Capitalization: $2.63 billion

Rumble's Chairman and CEO, Chris Pavlovski, commented, “Rumble reported strong first-quarter 2025 results, highlighted by 34% year-over-year revenue growth to $23.7 million, driven by increased subscription revenue and monetization across our video and advertising platforms. MAUs of 59 million reflect improved user retention and continued product momentum following the U.S. election cycle. Key partnerships with major brands like Netflix, Crypto.com, and Chevron marked early wins for Rumble advertising, while progress in the Rumble Cloud business included new government and sports vertical clients, such as El Salvador and the Tampa Bay Buccaneers. With these new announcements and developments on the sales front, we remain energized by the potential for this business. We also further advanced the Rumble Wallet, which we plan to release later this year, supporting our international expansion. With our balance sheet fortified, significant tailwinds supporting our business, and Tether now closed, we have entered a new era for Rumble.”

Company Overview

Founded in 2013 as a champion for content creator rights and free expression, Rumble (NASDAQ:RUM) is a video sharing platform that positions itself as a free speech alternative to mainstream platforms, offering creators more favorable revenue-sharing opportunities.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

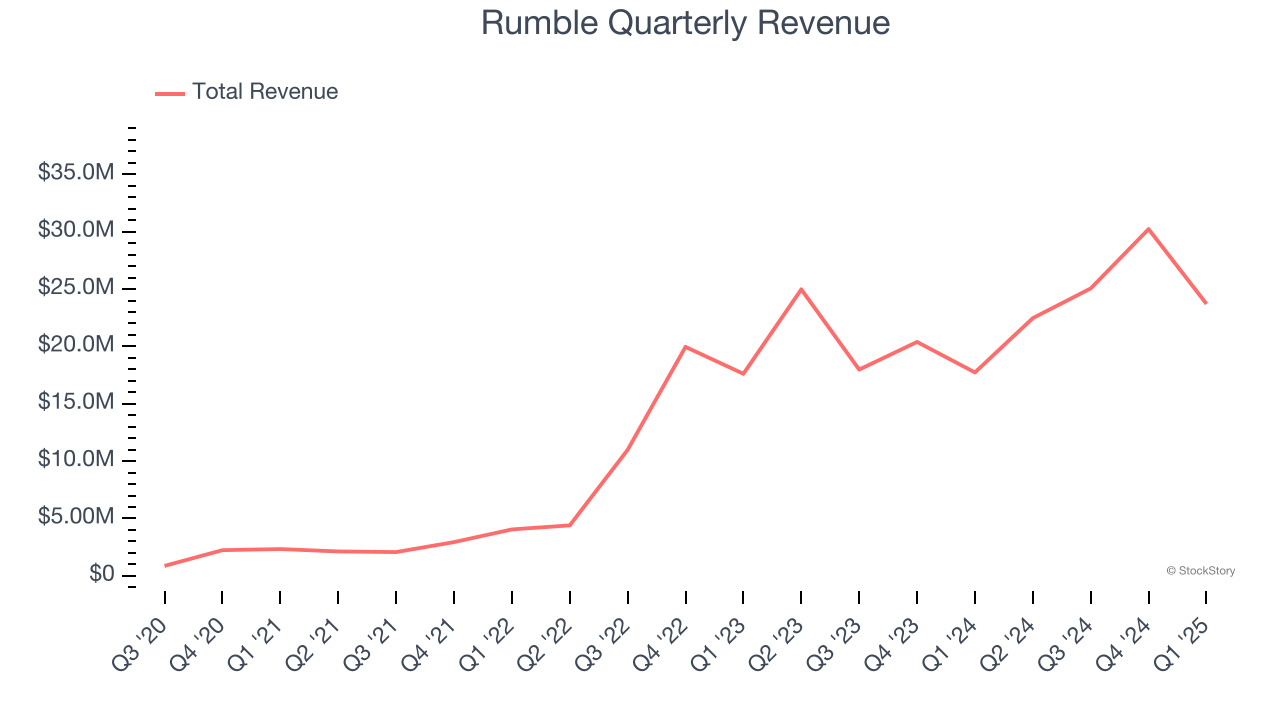

With $101.5 million in revenue over the past 12 months, Rumble is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

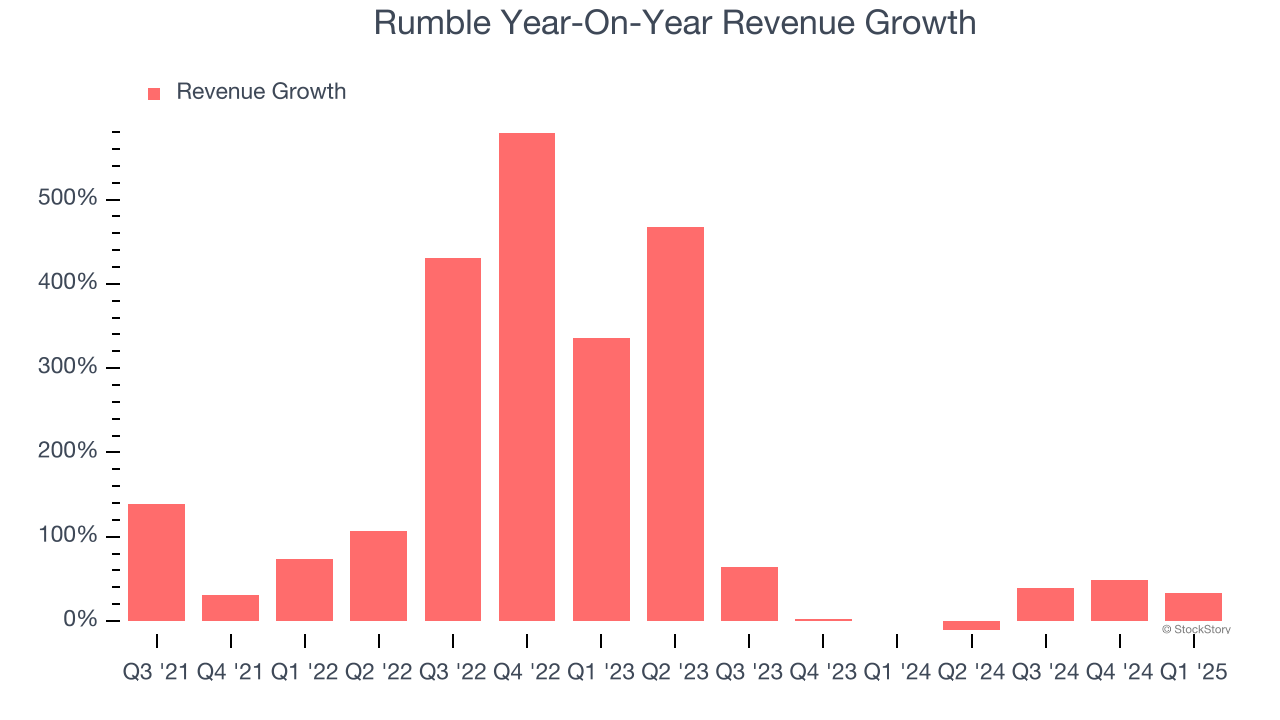

As you can see below, Rumble’s sales grew at an incredible 95.2% compounded annual growth rate over the last four years. This shows it had high demand, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a stretched historical view may miss recent innovations or disruptive industry trends. Rumble’s annualized revenue growth of 38.4% over the last two years is below its four-year trend, but we still think the results suggest healthy demand.

This quarter, Rumble reported wonderful year-on-year revenue growth of 33.7%, and its $23.71 million of revenue exceeded Wall Street’s estimates by 4.1%.

We also like to judge companies based on their projected revenue growth, but not enough Wall Street analysts cover the company for it to have reliable consensus estimates.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

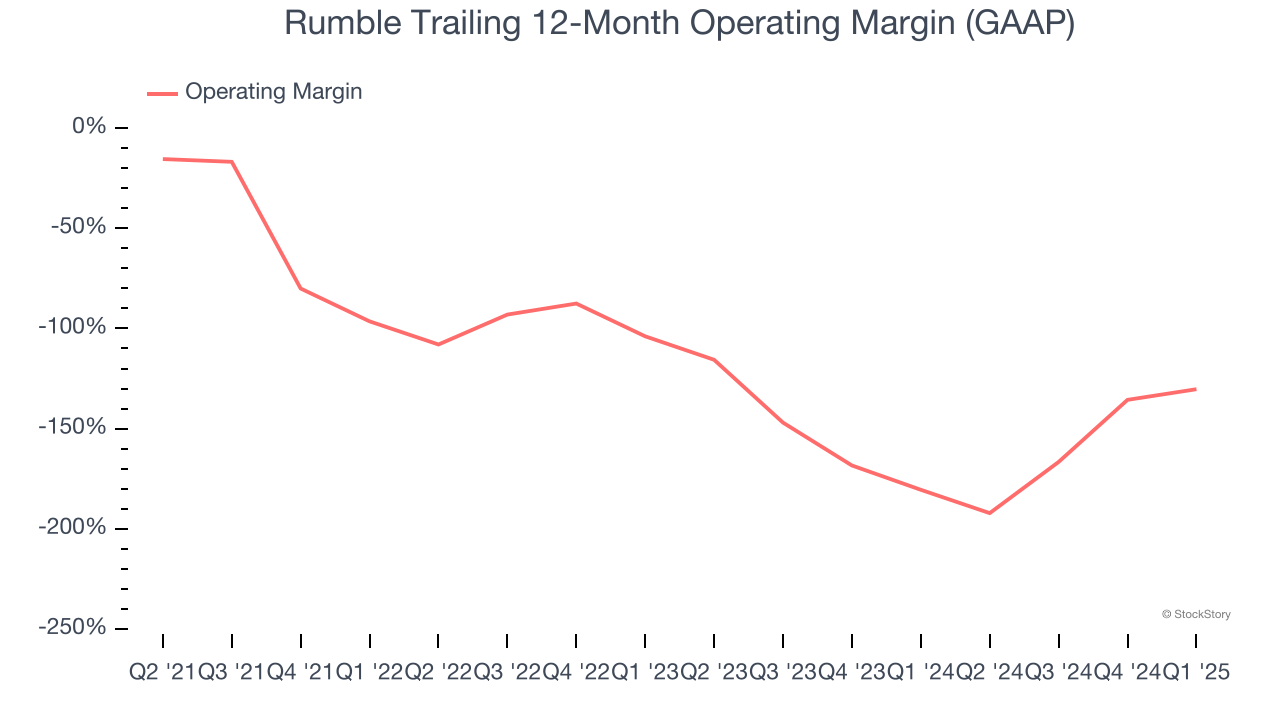

Rumble’s high expenses have contributed to an average operating margin of negative 137% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, Rumble’s operating margin decreased significantly over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Rumble’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Rumble generated a negative 153% operating margin. The company's consistent lack of profits raise a flag.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

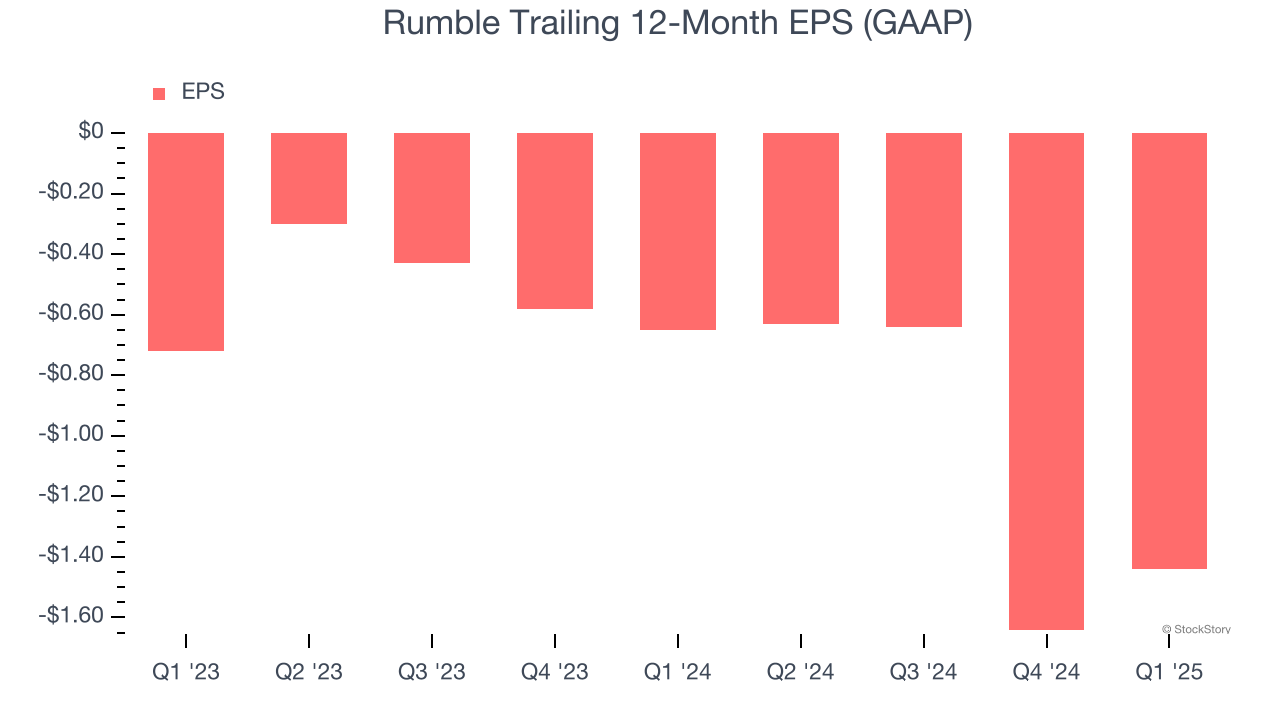

Rumble’s earnings losses deepened over the last two years as its EPS dropped 41.4% annually. We’ll keep a close eye on the company as diminishing earnings could imply changing secular trends and preferences.

In Q1, Rumble reported EPS at negative $0.01, up from negative $0.21 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data. This signals Rumble could be a hidden gem because it doesn’t have much coverage among professional brokers.

Key Takeaways from Rumble’s Q1 Results

We were impressed by how significantly Rumble blew past analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 3% to $8 immediately following the results.

Indeed, Rumble had a rock-solid quarterly earnings result, but is this stock a good investment here? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.