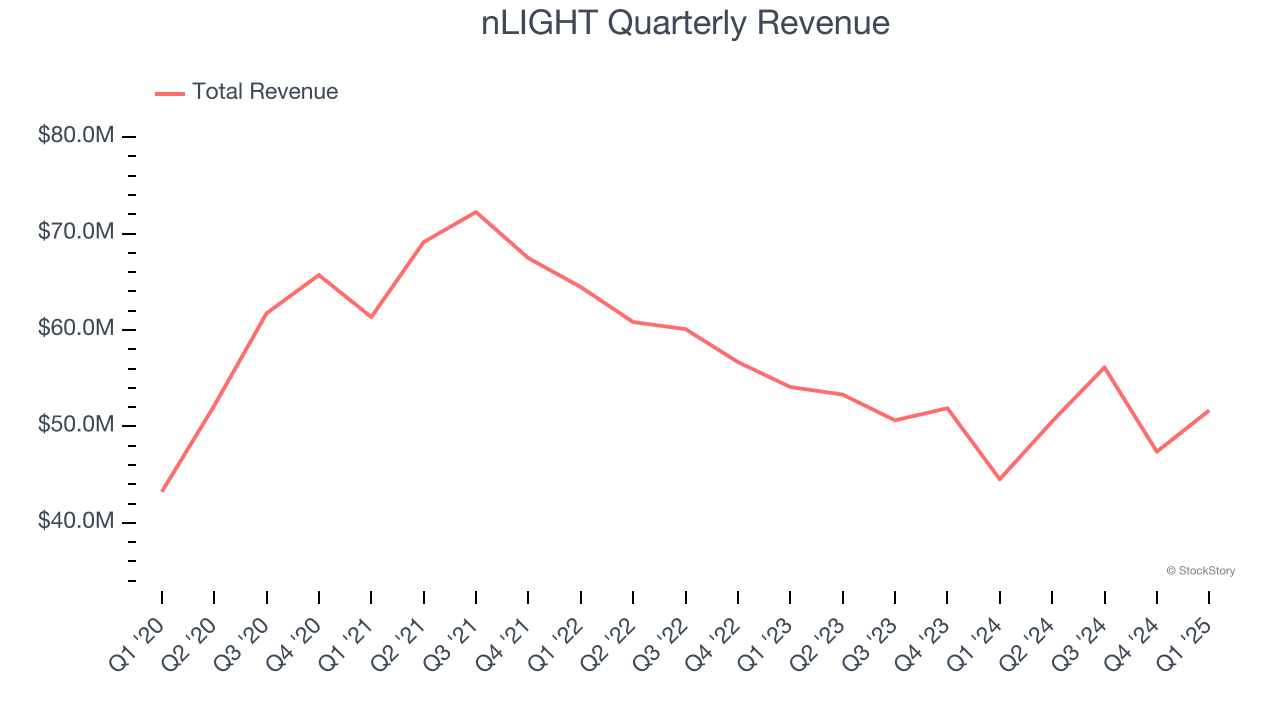

Laser company nLIGHT (NASDAQ:LASR) reported Q1 CY2025 results exceeding the market’s revenue expectations, with sales up 16% year on year to $51.67 million. On top of that, next quarter’s revenue guidance ($56 million at the midpoint) was surprisingly good and 11.7% above what analysts were expecting. Its non-GAAP loss of $0.04 per share was 78.7% above analysts’ consensus estimates.

Is now the time to buy nLIGHT? Find out by accessing our full research report, it’s free.

nLIGHT (LASR) Q1 CY2025 Highlights:

- Revenue: $51.67 million vs analyst estimates of $47.34 million (16% year-on-year growth, 9.1% beat)

- Adjusted EPS: -$0.04 vs analyst estimates of -$0.19 (78.7% beat)

- Adjusted EBITDA: $116,000 vs analyst estimates of -$5.14 million (0.2% margin, significant beat)

- Revenue Guidance for Q2 CY2025 is $56 million at the midpoint, above analyst estimates of $50.15 million

- EBITDA guidance for the full year is -$1.5 million at the midpoint, above analyst estimates of -$11.98 million

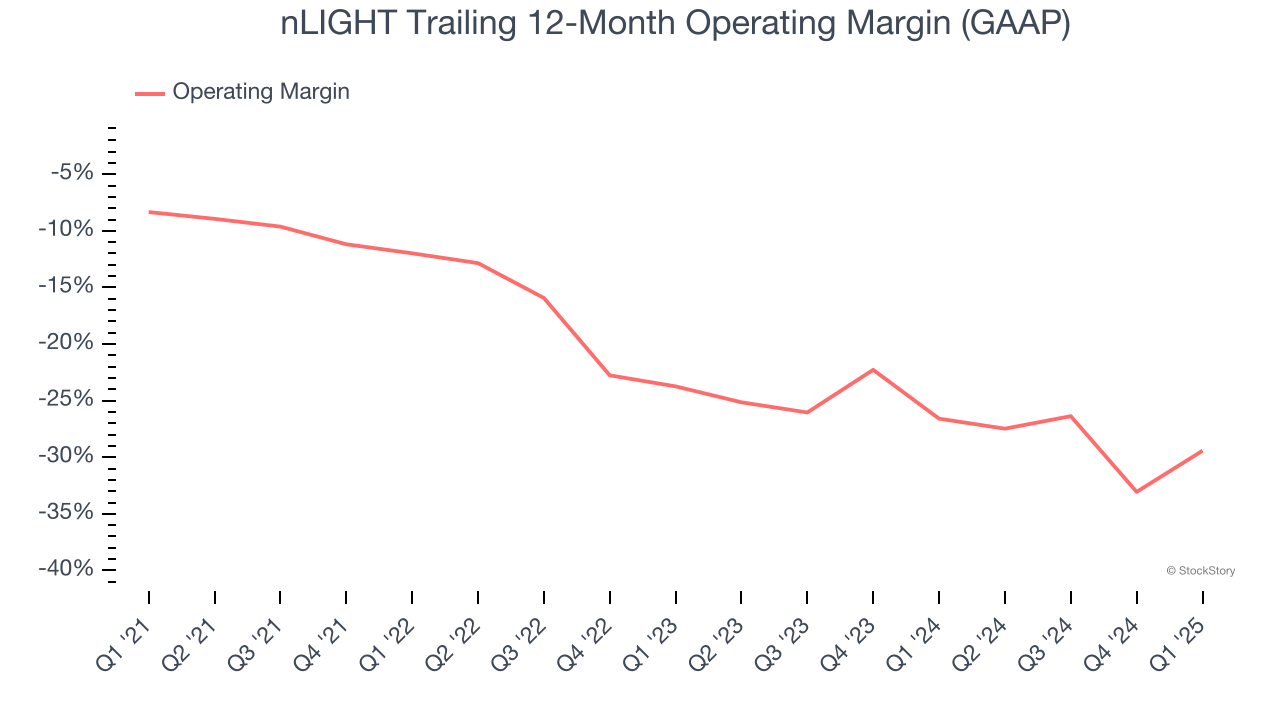

- Operating Margin: -18.6%, up from -33.1% in the same quarter last year

- Free Cash Flow was -$2.30 million, down from $9.82 million in the same quarter last year

- Market Capitalization: $425.7 million

Company Overview

Founded by a former CEO and Harvard-educated entrepreneur Scott Keeneyn, nLIGHT (NASDAQ:LASR) offers semiconductor and fiber lasers to the industrial, aerospace & defense, and medical sectors.

Sales Growth

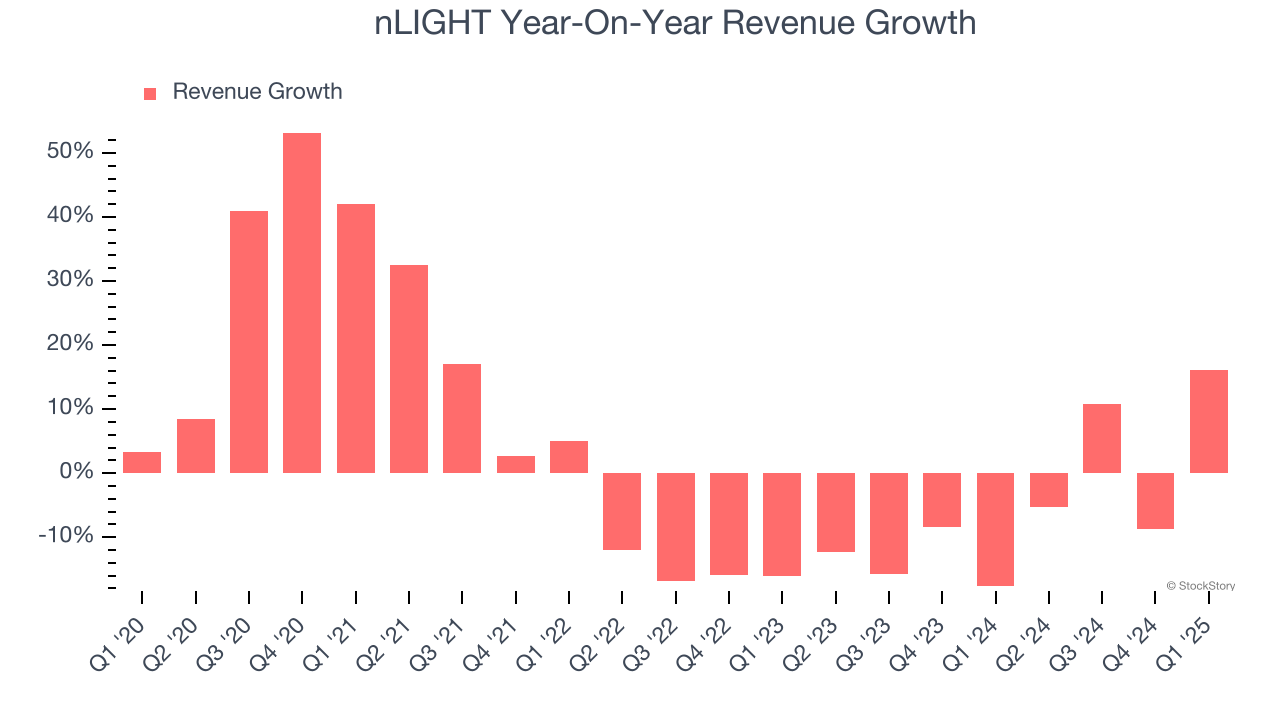

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, nLIGHT’s 2.9% annualized revenue growth over the last five years was sluggish. This fell short of our benchmarks and is a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. nLIGHT’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 5.8% annually. nLIGHT isn’t alone in its struggles as the Electronic Components industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

We can better understand the company’s revenue dynamics by analyzing its most important segments, Laser Products and Advanced Developments, which are 69.1% and 30.9% of revenue. Over the last two years, nLIGHT’s Laser Products revenue (lasers, amplifiers, and directed energy products) averaged 10.4% year-on-year declines. On the other hand, its Advanced Developments revenue (R&D contracts) averaged 13.4% growth.

This quarter, nLIGHT reported year-on-year revenue growth of 16%, and its $51.67 million of revenue exceeded Wall Street’s estimates by 9.1%. Company management is currently guiding for a 10.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.3% over the next 12 months. While this projection implies its newer products and services will catalyze better top-line performance, it is still below average for the sector.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

nLIGHT’s high expenses have contributed to an average operating margin of negative 19.2% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, nLIGHT’s operating margin decreased by 21.1 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. nLIGHT’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, nLIGHT generated a negative 18.6% operating margin. The company's consistent lack of profits raise a flag.

Earnings Per Share

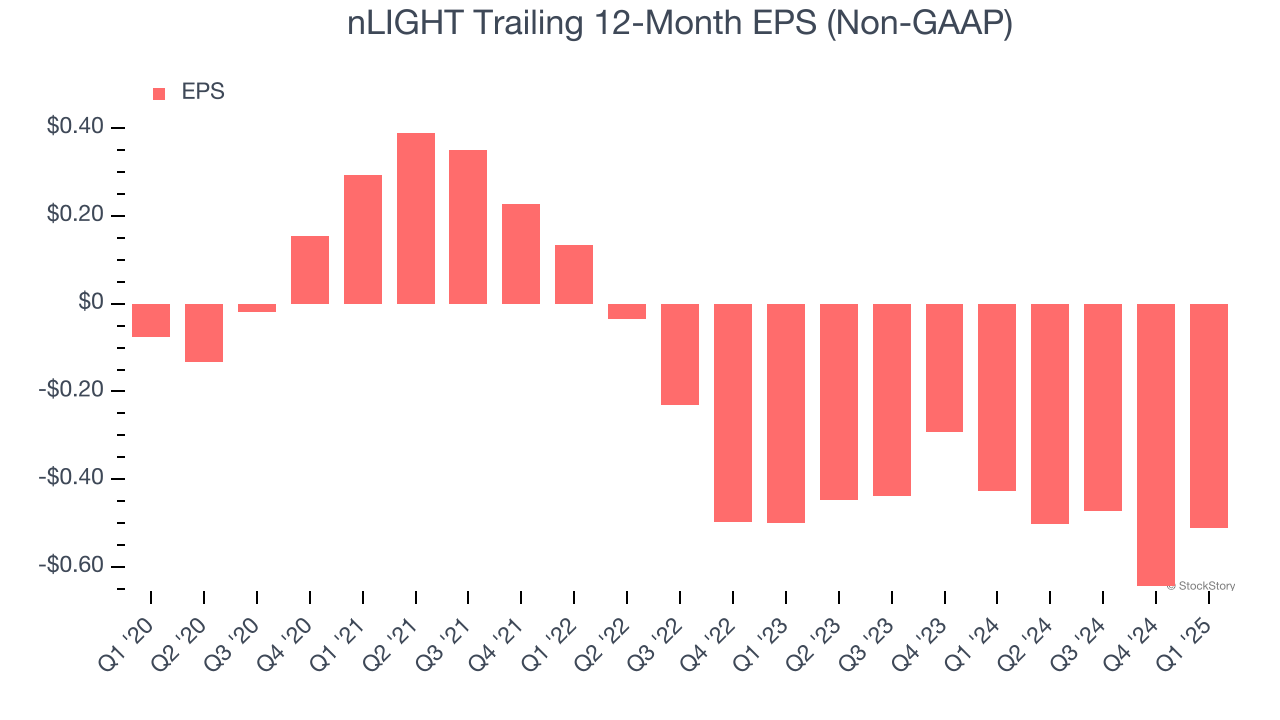

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

nLIGHT’s earnings losses deepened over the last five years as its EPS dropped 46.6% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, nLIGHT’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For nLIGHT, its two-year annual EPS declines of 1.1% show it’s still underperforming. These results were bad no matter how you slice the data.

In Q1, nLIGHT reported EPS at negative $0.04, up from negative $0.17 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street is optimistic. Analysts forecast nLIGHT’s full-year EPS of negative $0.51 will reach break even.

Key Takeaways from nLIGHT’s Q1 Results

We were impressed by how significantly nLIGHT blew past analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 16.3% to $10 immediately after reporting.

nLIGHT had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.