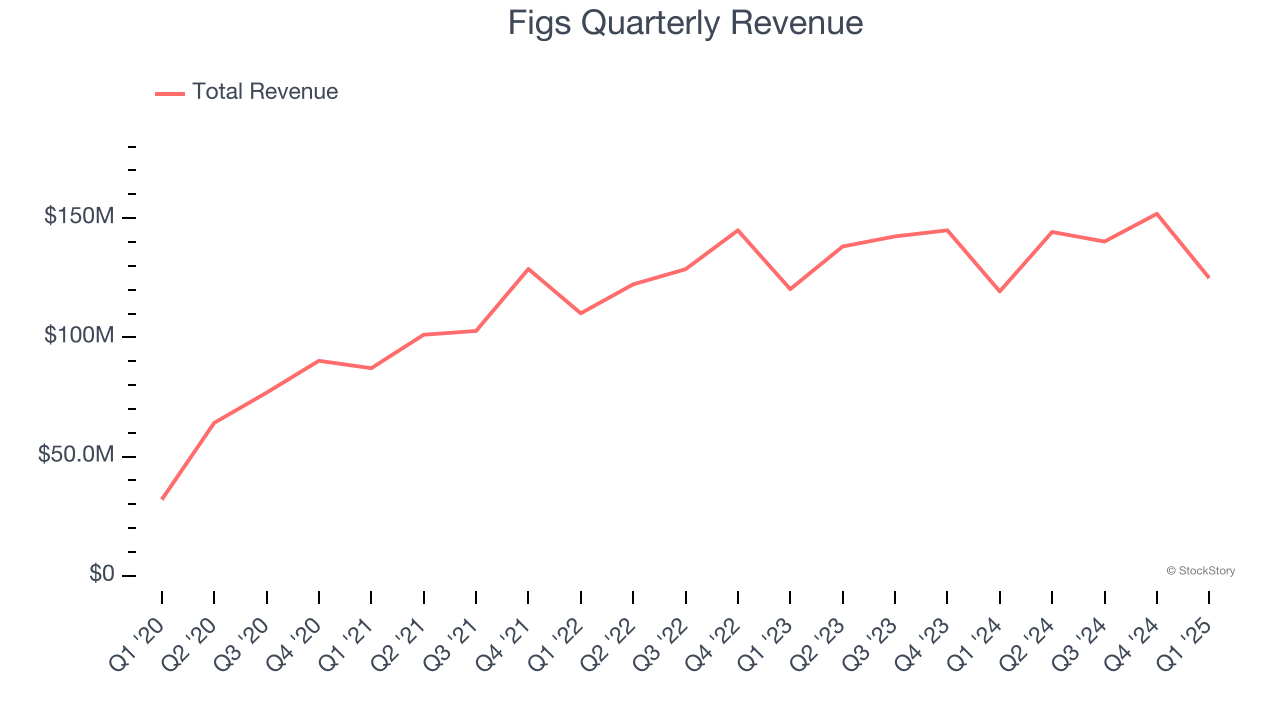

Healthcare apparel company Figs (NYSE:FIGS) beat Wall Street’s revenue expectations in Q1 CY2025, with sales up 4.7% year on year to $124.9 million. Its GAAP profit of $0.01 per share was $0.01 above analysts’ consensus estimates.

Is now the time to buy Figs? Find out by accessing our full research report, it’s free.

Figs (FIGS) Q1 CY2025 Highlights:

- Revenue: $124.9 million vs analyst estimates of $119.2 million (4.7% year-on-year growth, 4.8% beat)

- EPS (GAAP): $0.01 vs analyst estimates of $0 ($0.01 beat)

- Adjusted EBITDA: $9.00 million vs analyst estimates of $8.00 million (7.2% margin, 12.5% beat)

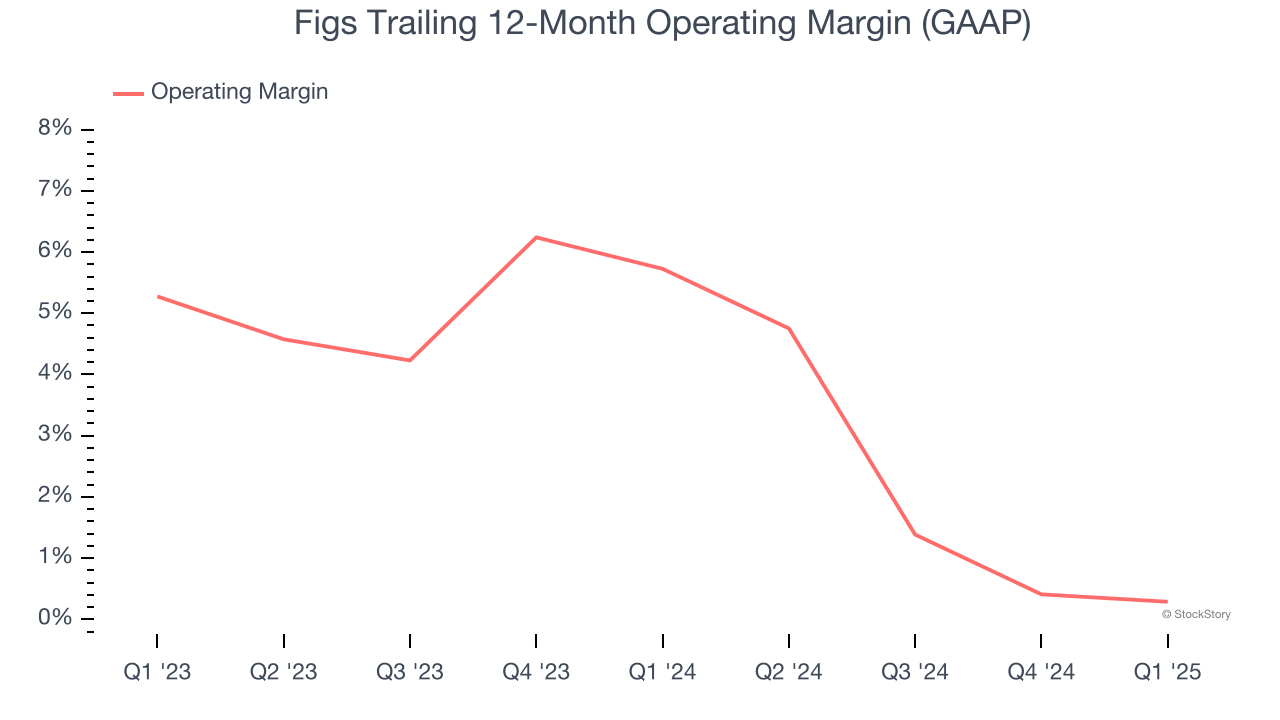

- Operating Margin: -0.2%, in line with the same quarter last year

- Free Cash Flow Margin: 6.3%, down from 9.3% in the same quarter last year

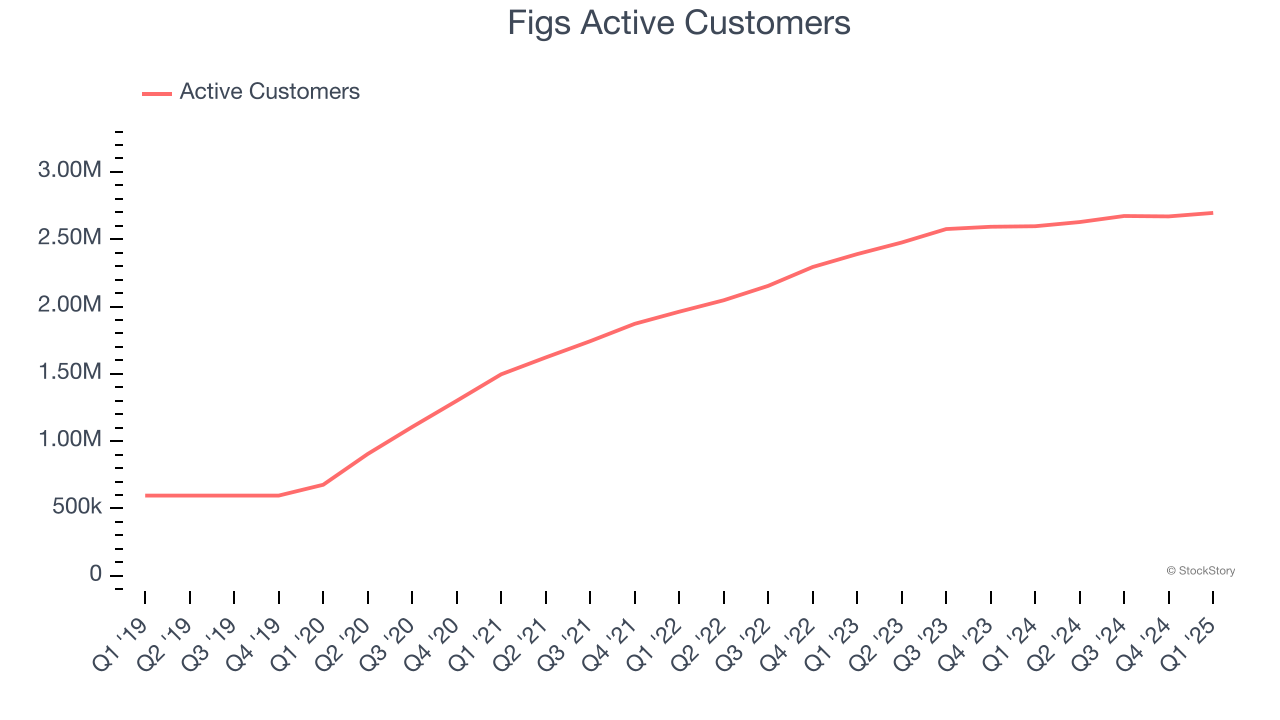

- Active Customers: 2.7 million, up 99,000 year on year

- Market Capitalization: $794.7 million

“First quarter results were ahead of expectations, supported by customer growth, strong full-priced selling, record AOV, and ultimately, a return to growth in the U.S.,” said Trina Spear, Chief Executive Officer and Co-Founder.

Company Overview

Rising to fame via TikTok and founded in 2013 by Heather Hasson and Trina Spear, Figs (NYSE:FIGS) is a healthcare apparel company known for its stylish approach to medical attire and uniforms.

Sales Growth

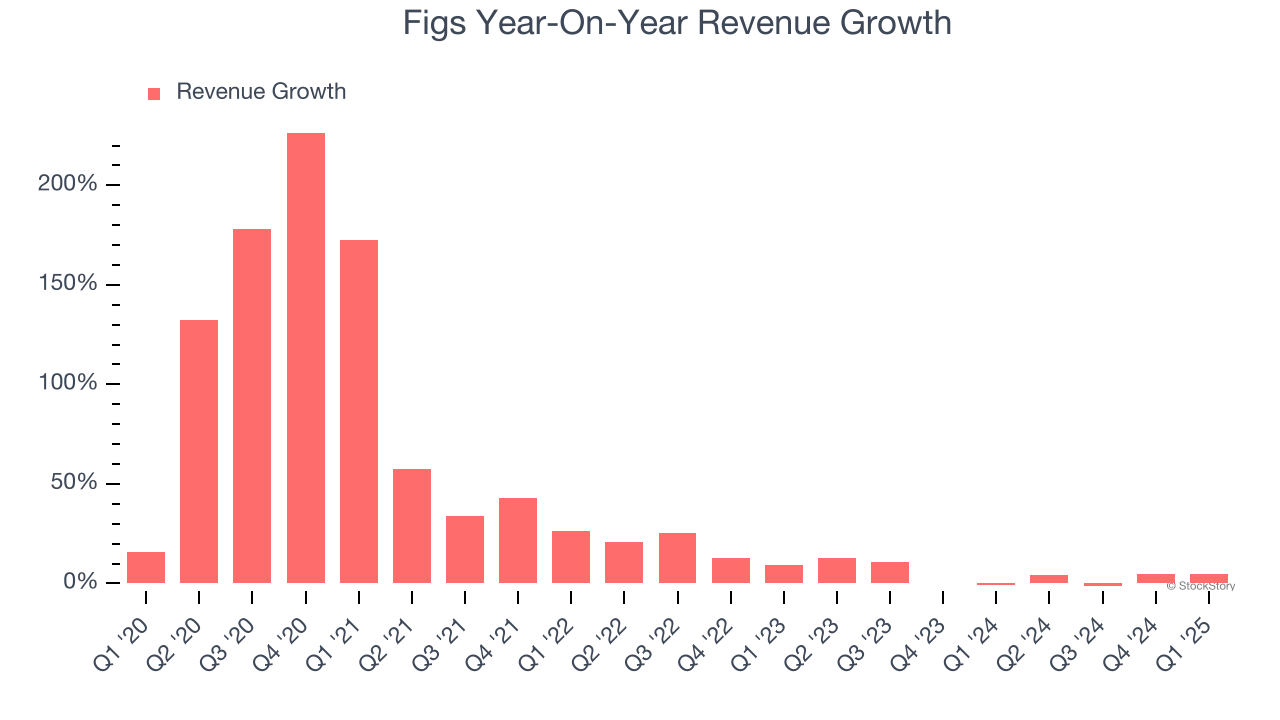

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, Figs’s sales grew at an incredible 37.3% compounded annual growth rate over the last five years. Its growth beat the average consumer discretionary company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Figs’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 4.3% over the last two years was well below its five-year trend.

Figs also discloses its number of active customers, which reached 2.7 million in the latest quarter. Over the last two years, Figs’s active customers averaged 9.9% year-on-year growth. Because this number is higher than its revenue growth during the same period, we can see the company’s monetization has fallen.

This quarter, Figs reported modest year-on-year revenue growth of 4.7% but beat Wall Street’s estimates by 4.8%.

Looking ahead, sell-side analysts expect revenue to decline by 2.2% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Figs’s operating margin has shrunk over the last 12 months and averaged 3% over the last two years. Although this result isn’t good, the company’s elite historical revenue growth suggests it ramped up investments to capture market share. We’ll keep a close eye to see if this strategy pays off.

In Q1, Figs’s breakeven margin was in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

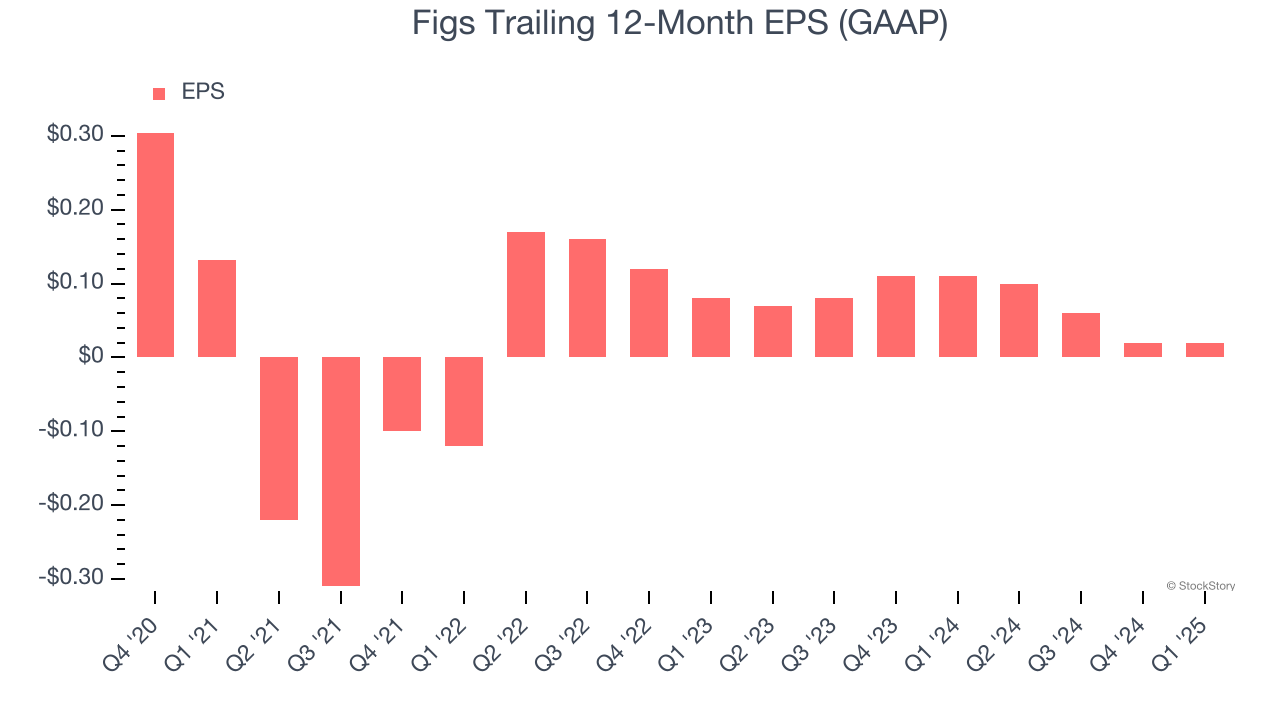

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Figs’s full-year EPS dropped 259%, or 37.6% annually, over the last four years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. Consumer Discretionary companies are particularly exposed to this, and if the tide turns unexpectedly, Figs’s low margin of safety could leave its stock price susceptible to large downswings.

In Q1, Figs reported EPS at $0.01, in line with the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Figs to perform poorly. Analysts forecast its full-year EPS of $0.02 will hit $0.07.

Key Takeaways from Figs’s Q1 Results

The quarter itself was fine, with revenue and EBITDA beating. However, full-year EBITDA margin guidance missed and likely raises fears of tariff or macro impacts. The stock traded down 13.4% to $4.35 immediately after reporting.

Should you buy the stock or not? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.