Over the past six months, Clover Health has been a great trade. While the S&P 500 was flat, the stock price has climbed by 9.5% to $3.33 per share. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Clover Health, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Clover Health Not Exciting?

Despite the momentum, we're cautious about Clover Health. Here are three reasons why we avoid CLOV and a stock we'd rather own.

1. Revenue Tumbling Downwards

We at StockStory place the most emphasis on long-term growth, but within healthcare, a stretched historical view may miss recent innovations or disruptive industry trends. Clover Health’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 28.7% over the last two years.

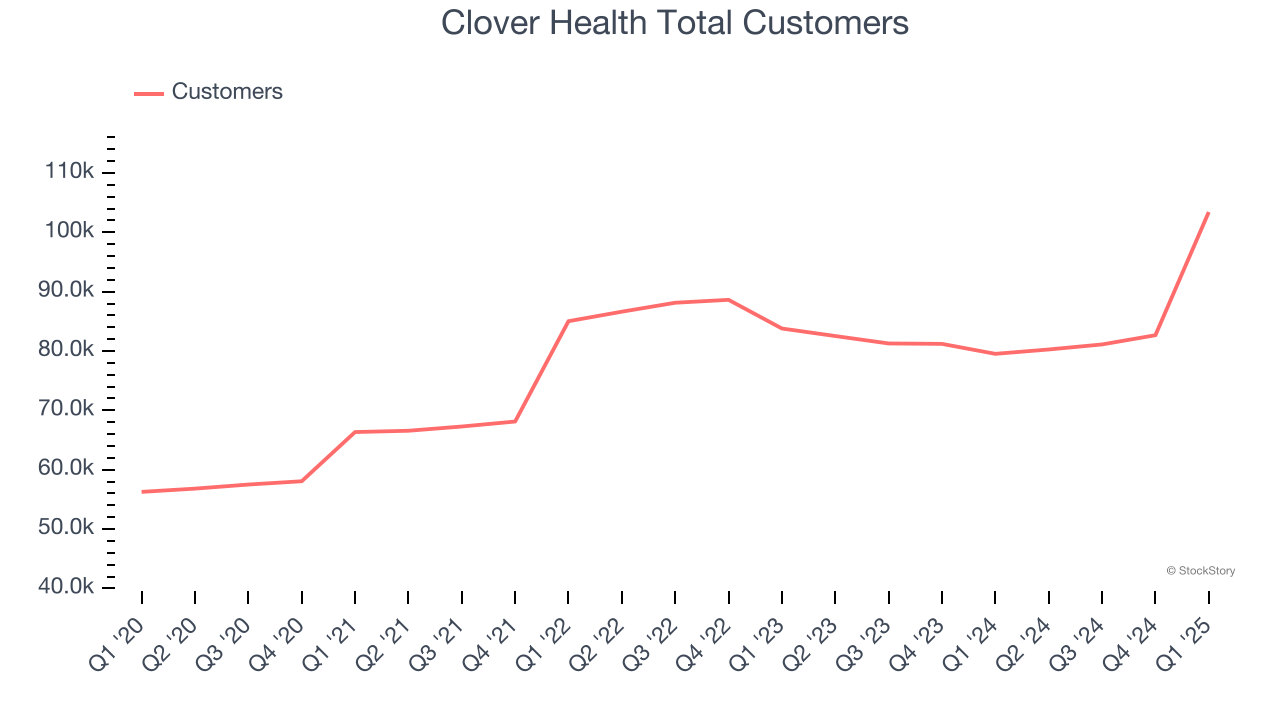

2. Customer Base Hits a Plateau

Revenue growth can be broken down into the number of customers and the average spend per customer. Both are important because an increasing customer base leads to more upselling opportunities while the revenue per customer shows how successful a company was in executing its upselling strategy.

Over the last two years, Clover Health’s total customers were flat, coming in at 103,418 in the latest quarter. This performance was underwhelming and shows the company faced challenges in landing new contracts. It also suggests there may be increasing competition or market saturation.

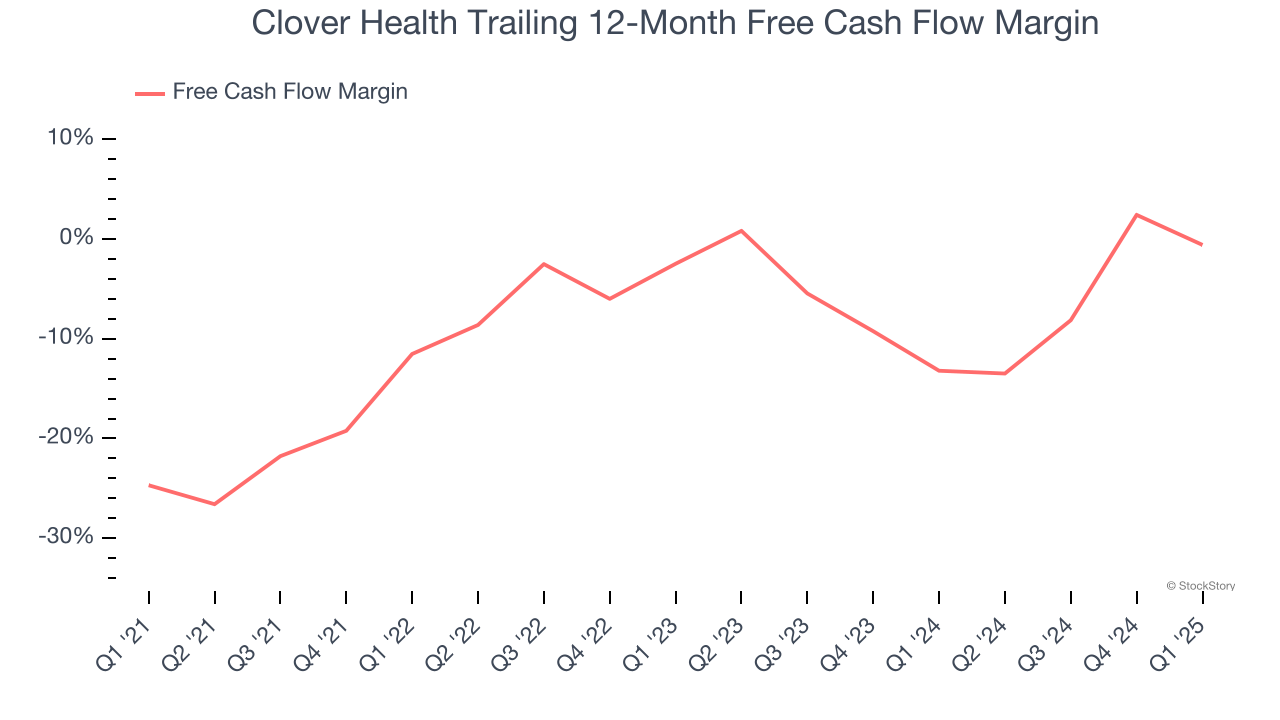

3. Cash Burn Ignites Concerns

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Clover Health’s demanding reinvestments have consumed many resources over the last five years, contributing to an average free cash flow margin of negative 7.9%. This means it lit $7.87 of cash on fire for every $100 in revenue.

Final Judgment

Clover Health isn’t a terrible business, but it doesn’t pass our bar. With its shares topping the market in recent months, the stock trades at 45.2× forward EV-to-EBITDA (or $3.33 per share). This multiple tells us a lot of good news is priced in - you can find better investment opportunities elsewhere. We’d suggest looking at our favorite semiconductor picks and shovels play.

Stocks We Like More Than Clover Health

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 176% over the last five years.

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.