Shareholders of Bill.com would probably like to forget the past six months even happened. The stock dropped 24.7% and now trades at $40.60. This may have investors wondering how to approach the situation.

Given the weaker price action, is now the time to buy BILL? Find out in our full research report, it’s free.

Why Does Bill.com Spark Debate?

Started by René Lacerte in 2006 after selling his previous payroll and accounting software company PayCycle to Intuit, Bill.com (NYSE:BILL) is a software as a service platform that aims to make payments and billing processes easier for small and medium-sized businesses.

Two Positive Attributes:

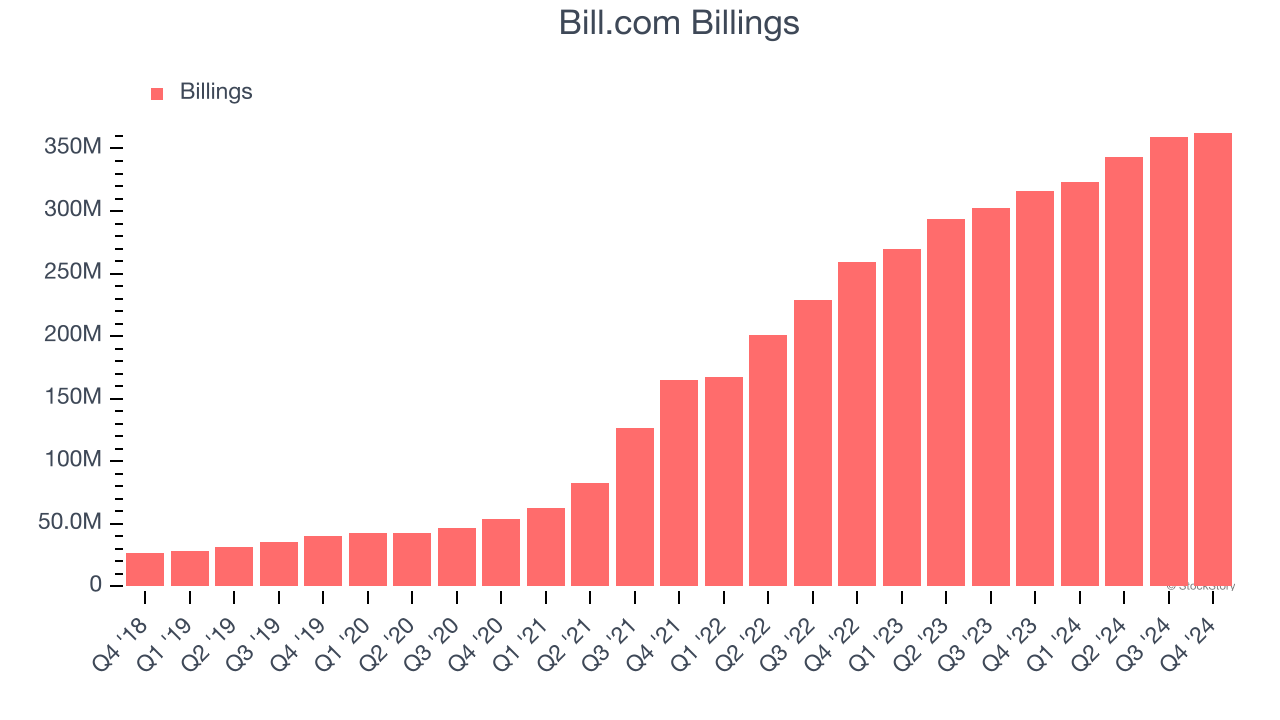

1. Billings Growth Boosts Cash On Hand

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Bill.com’s billings punched in at $362.7 million in Q4, and over the last four quarters, its year-on-year growth averaged 17.6%. This performance was solid, indicating robust customer demand. The cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

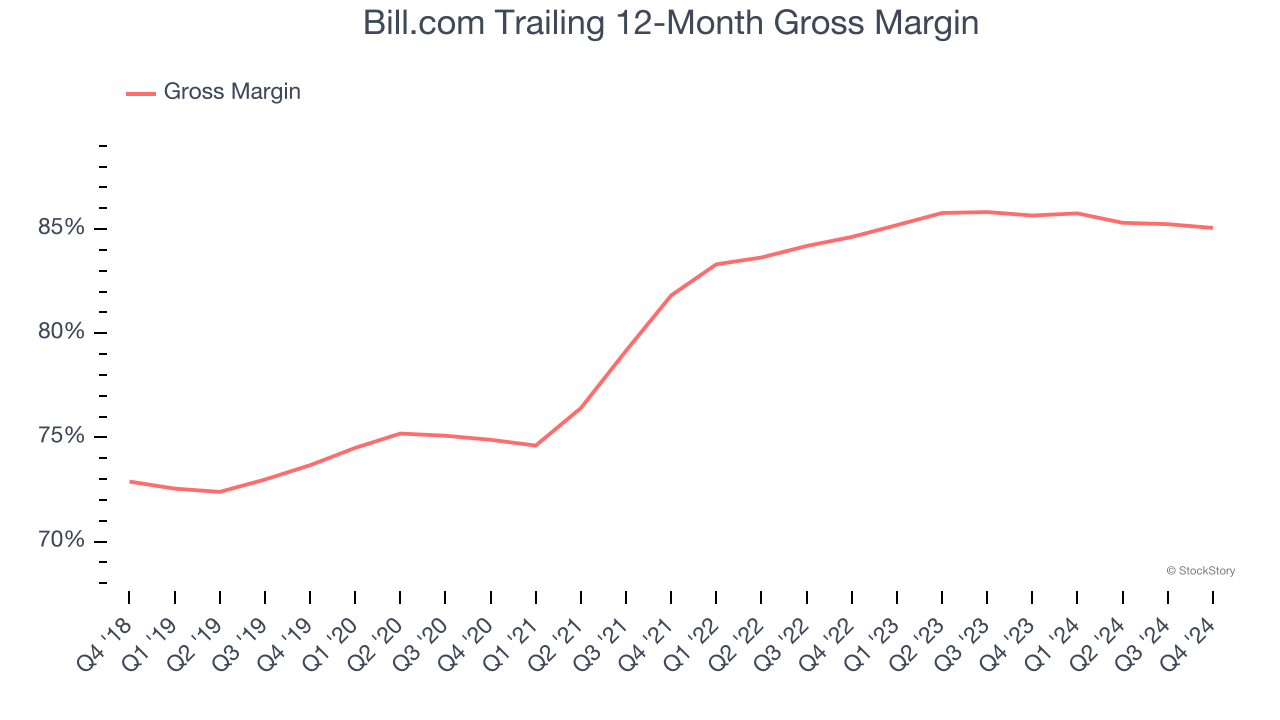

2. Elite Gross Margin Powers Best-In-Class Business Model

Software is eating the world. It’s one of our favorite business models because once you develop the product, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

Bill.com’s gross margin is one of the highest in the software sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in new products and sales during periods of rapid growth to achieve outsized profits at scale. As you can see below, it averaged an elite 85.1% gross margin over the last year. That means Bill.com only paid its providers $14.95 for every $100 in revenue.

One Reason to be Careful:

Customer Churn Hurts Long-Term Outlook

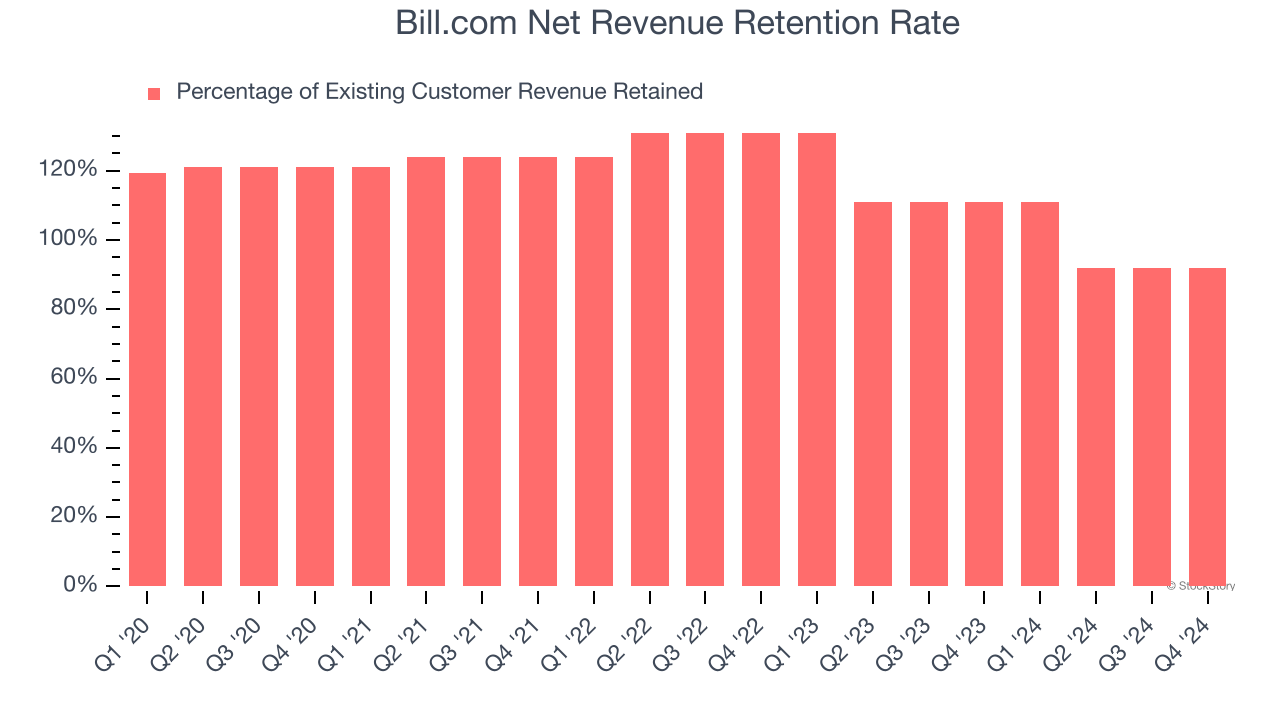

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Bill.com’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 96.8% in Q4. This means Bill.com’s revenue would’ve decreased by 3.2% over the last 12 months if it didn’t win any new customers.

Bill.com’s already weak net retention rate has been dropping the last year, signaling that some customers aren’t satisfied with its products, leading to lost contracts and revenue streams.

Final Judgment

Bill.com’s positive characteristics outweigh the negatives. With the recent decline, the stock trades at 2.7× forward price-to-sales (or $40.60 per share). Is now the right time to buy? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Bill.com

The market surged in 2024 and reached record highs after Donald Trump’s presidential victory in November, but questions about new economic policies are adding much uncertainty for 2025.

While the crowd speculates what might happen next, we’re homing in on the companies that can succeed regardless of the political or macroeconomic environment. Put yourself in the driver’s seat and build a durable portfolio by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.