Earnings results often indicate what direction a company will take in the months ahead. With Q4 behind us, let’s have a look at Nike (NYSE:NKE) and its peers.

Before the advent of the internet, styles changed, but consumers mainly bought shoes by visiting local brick-and-mortar shoe, department, and specialty stores. Today, not only do styles change more frequently as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some footwear companies have made concerted efforts to adapt while those who are slower to move may fall behind.

The 7 footwear stocks we track reported a mixed Q4. As a group, revenues beat analysts’ consensus estimates by 2.3% while next quarter’s revenue guidance was 0.5% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 22.2% since the latest earnings results.

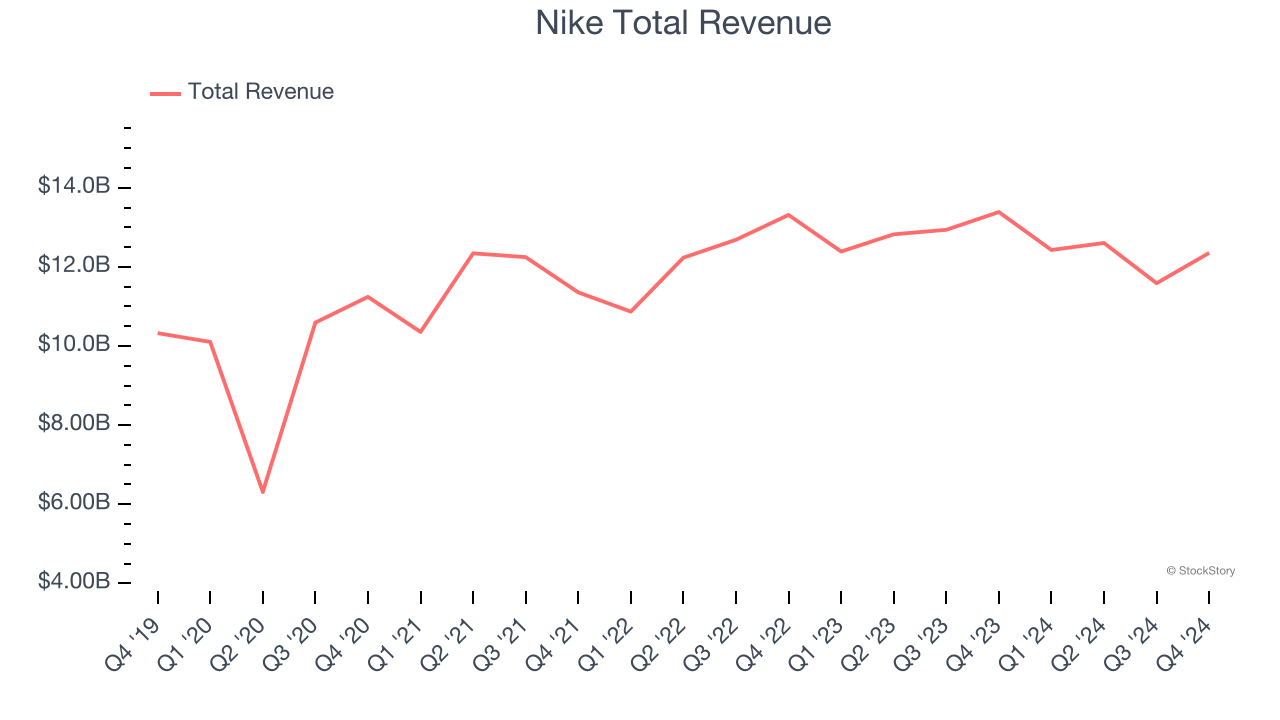

Best Q4: Nike (NYSE:NKE)

Originally selling Japanese Onitsuka Tiger sneakers as Blue Ribbon Sports, Nike (NYSE:NKE) is a global titan in athletic footwear, apparel, equipment, and accessories.

Nike reported revenues of $12.35 billion, down 7.7% year on year. This print exceeded analysts’ expectations by 1.8%. Overall, it was an exceptional quarter for the company with an impressive beat of analysts’ adjusted operating income estimates and a solid beat of analysts’ EPS estimates.

Nike delivered the slowest revenue growth of the whole group. The stock is down 4.7% since reporting and currently trades at $73.46.

Is now the time to buy Nike? Access our full analysis of the earnings results here, it’s free.

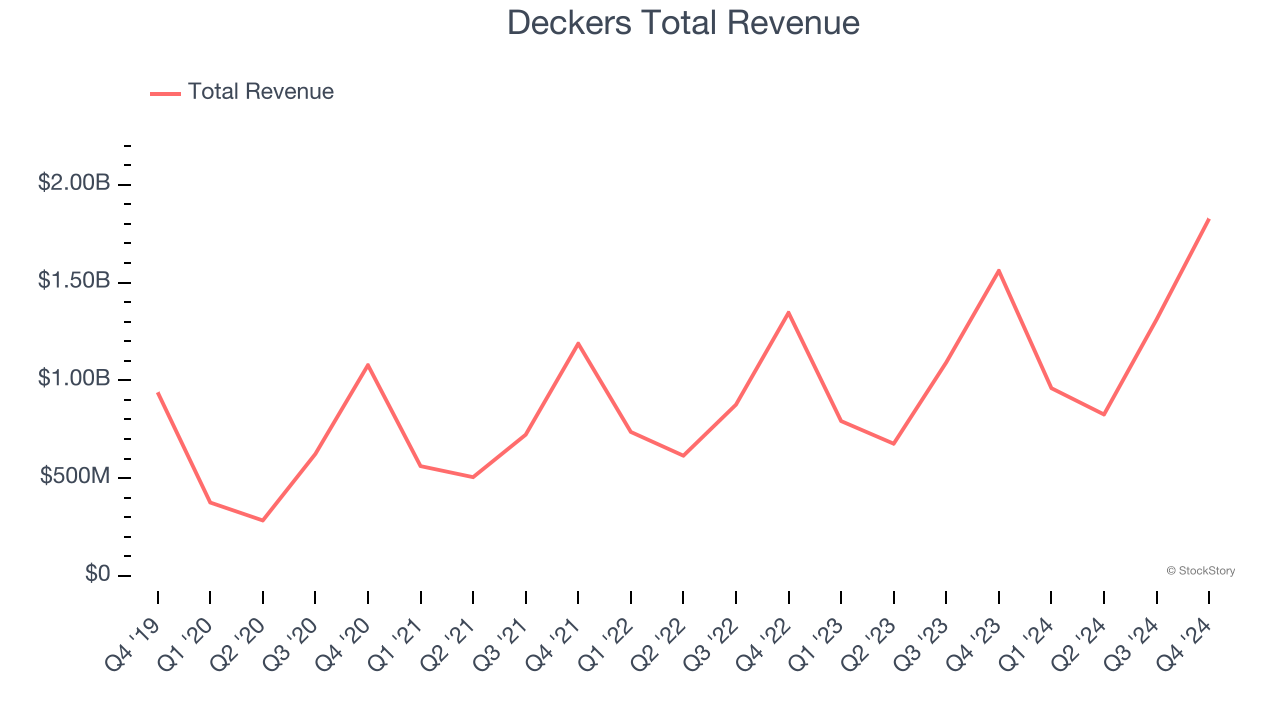

Deckers (NYSE:DECK)

Established in 1973, Deckers (NYSE:DECK) is a footwear and apparel conglomerate with a portfolio of lifestyle and performance brands.

Deckers reported revenues of $1.83 billion, up 17.1% year on year, outperforming analysts’ expectations by 5.5%. The business had a strong quarter with an impressive beat of analysts’ constant currency revenue estimates and a solid beat of analysts’ EPS estimates.

Deckers pulled off the fastest revenue growth and highest full-year guidance raise among its peers. Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 45.6% since reporting. It currently trades at $121.03.

Is now the time to buy Deckers? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Genesco (NYSE:GCO)

Spanning a broad range of styles, brands, and prices, Genesco (NYSE:GCO) sells footwear, apparel, and accessories through multiple brands and banners.

Genesco reported revenues of $745.9 million, flat year on year, falling short of analysts’ expectations by 5%. It was a softer quarter as it posted adjusted operating income in line with analysts’ estimates.

Genesco delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 34.6% since the results and currently trades at $21.22.

Read our full analysis of Genesco’s results here.

Crocs (NASDAQ:CROX)

Founded in 2002, Crocs (NASDAQ:CROX) sells casual footwear and is known for its iconic clog shoe.

Crocs reported revenues of $989.8 million, up 3.1% year on year. This number beat analysts’ expectations by 2.8%. Overall, it was a strong quarter as it also produced a solid beat of analysts’ constant currency revenue estimates and a decent beat of analysts’ EPS estimates.

The stock is up 14.7% since reporting and currently trades at $101.85.

Read our full, actionable report on Crocs here, it’s free.

Wolverine Worldwide (NYSE:WWW)

Founded in 1883, Wolverine Worldwide (NYSE:WWW) is a global footwear company with a diverse portfolio of brands including Merrell, Hush Puppies, and Saucony.

Wolverine Worldwide reported revenues of $494.7 million, up 3% year on year. This result surpassed analysts’ expectations by 5.9%. However, it was a slower quarter as it logged full-year EPS guidance missing analysts’ expectations.

Wolverine Worldwide delivered the biggest analyst estimates beat but had the weakest full-year guidance update among its peers. The stock is down 28.2% since reporting and currently trades at $13.44.

Read our full, actionable report on Wolverine Worldwide here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.