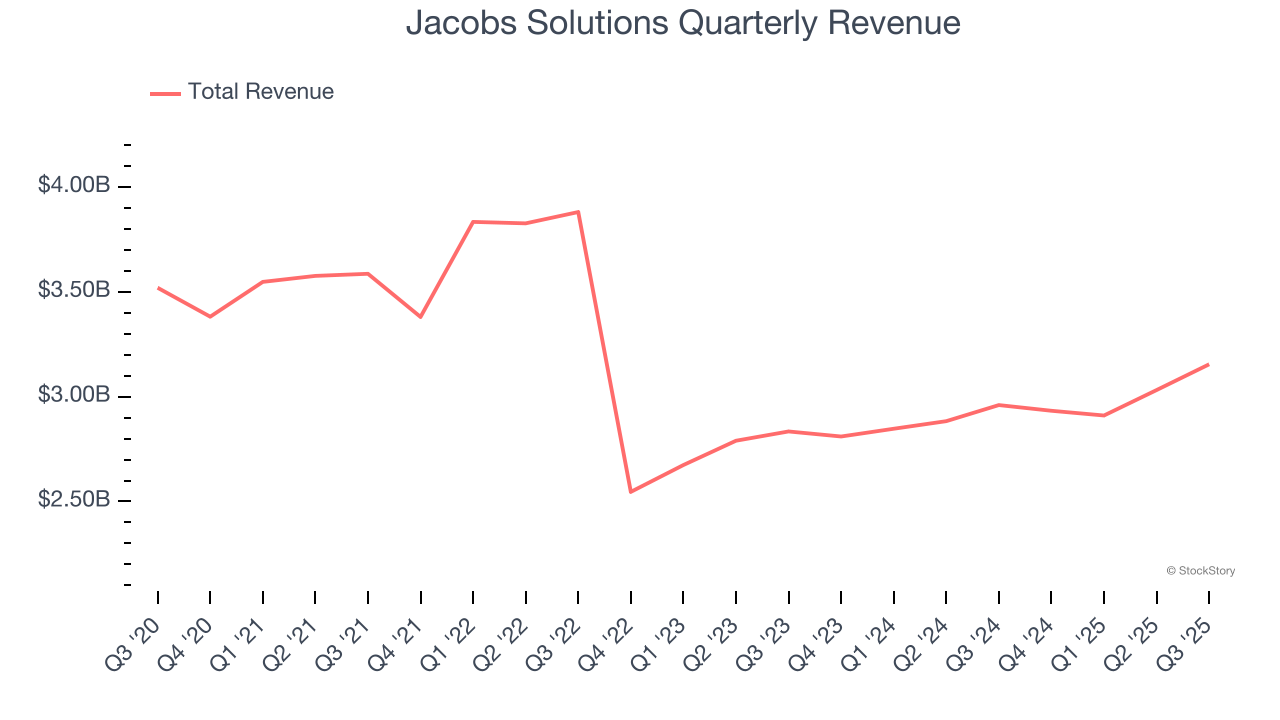

Global professional services company Jacobs Solutions (NYSE:J) announced better-than-expected revenue in Q3 CY2025, with sales up 6.6% year on year to $3.15 billion. Its non-GAAP profit of $1.75 per share was 4.2% above analysts’ consensus estimates.

Is now the time to buy Jacobs Solutions? Find out by accessing our full research report, it’s free for active Edge members.

Jacobs Solutions (J) Q3 CY2025 Highlights:

- Revenue: $3.15 billion vs analyst estimates of $3.13 billion (6.6% year-on-year growth, 0.7% beat)

- Adjusted EPS: $1.75 vs analyst estimates of $1.68 (4.2% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $7.10 at the midpoint, beating analyst estimates by 1.3%

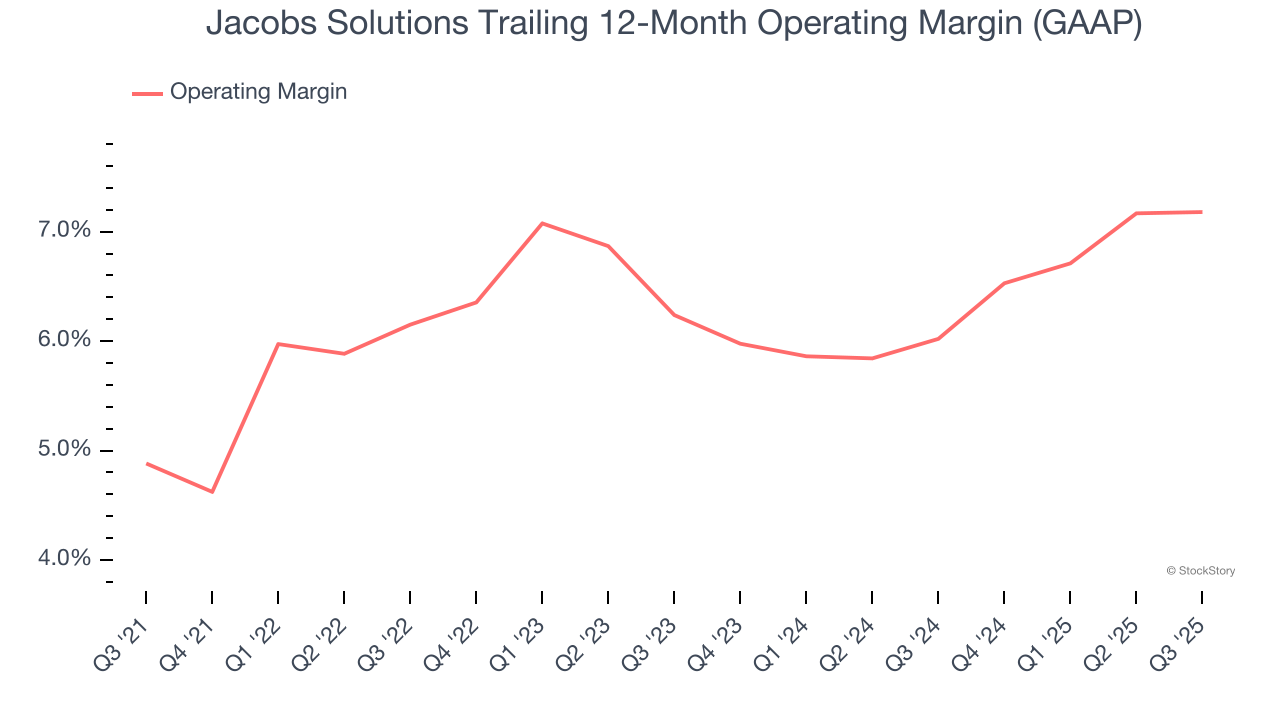

- Operating Margin: 6.7%, in line with the same quarter last year

- Free Cash Flow Margin: 11.2%, up from 5.3% in the same quarter last year

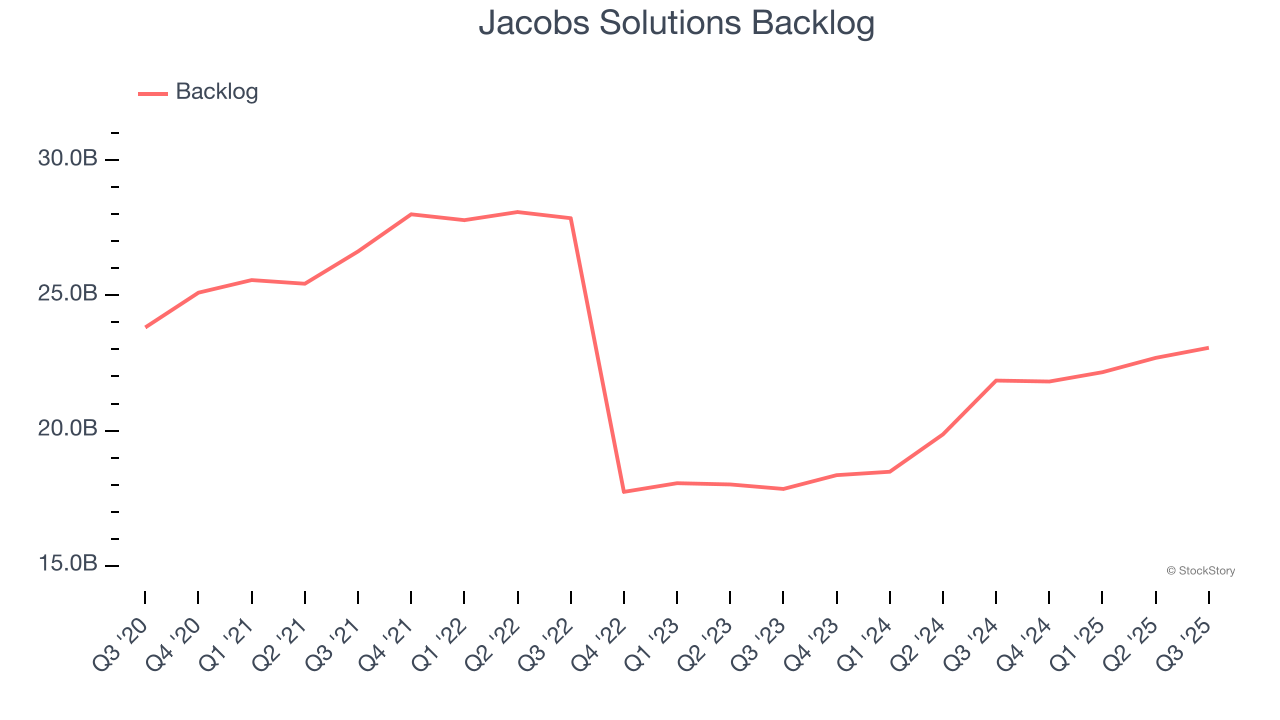

- Backlog: $23.06 billion at quarter end, up 5.6% year on year

- Market Capitalization: $17.34 billion

Jacobs' Chair and CEO Bob Pragada commented, "We are pleased to have met or exceeded all our key metrics for FY25. We grew revenue organically mid-single-digits year-over-year and expanded our operating margin meaningfully. The Life Sciences, Data Center, Water, Energy & Power and Transportation sectors drove Infrastructure & Advanced Facilities' (I&AF) revenue growth in FY25, and we anticipate these sectors will remain strong in FY26 and beyond. Additionally, PA Consulting saw revenue growth accelerate during the fiscal year, contributing positively to consolidated results. We enter FY26 with multiple secular tailwinds, clear line-of-sight to continued synergistic expansion with PA Consulting and a record backlog, positioning us for profitable growth."

Company Overview

With a workforce of approximately 45,000 professionals tackling complex challenges from water scarcity to cybersecurity, Jacobs Solutions (NYSE:J) provides engineering, consulting, and technical services focused on infrastructure, sustainability, and advanced technology solutions.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $12.03 billion in revenue over the past 12 months, Jacobs Solutions is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when you’ve penetrated most of the market. For Jacobs Solutions to boost its sales, it likely needs to adjust its prices, launch new offerings, or lean into foreign markets.

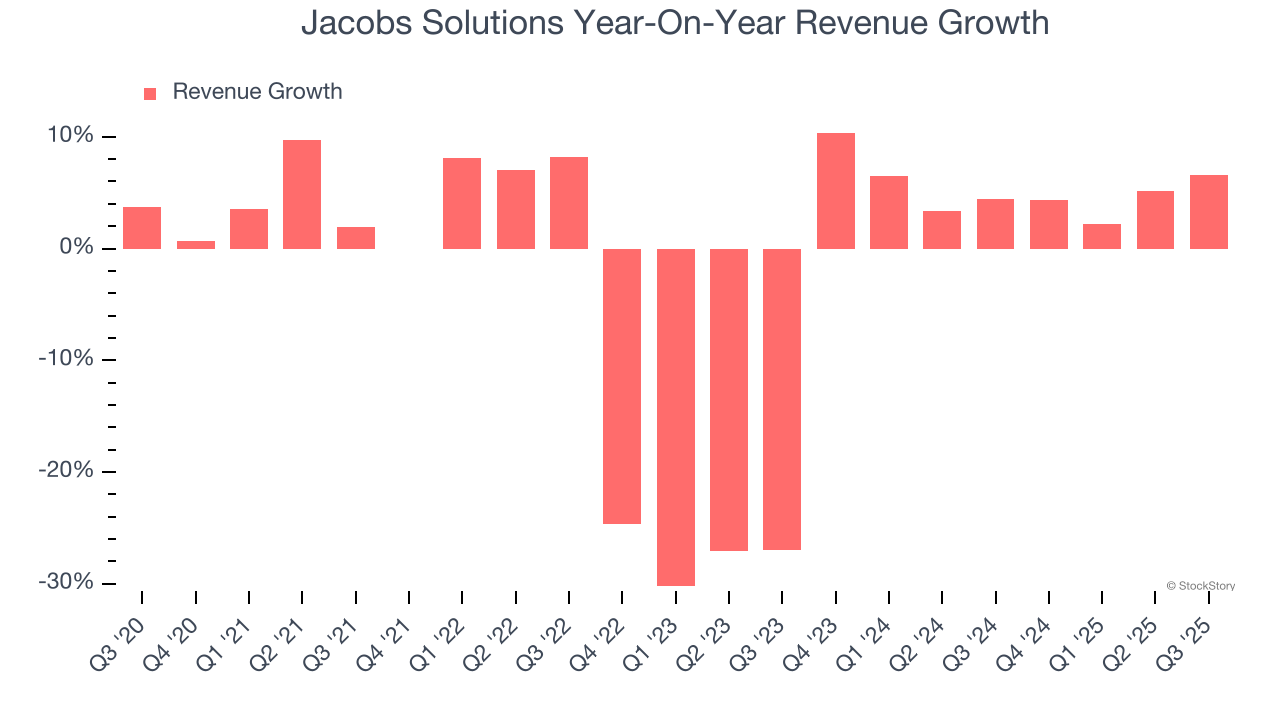

As you can see below, Jacobs Solutions struggled to generate demand over the last five years. Its sales dropped by 2.4% annually, a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Jacobs Solutions’s annualized revenue growth of 5.3% over the last two years is above its five-year trend, suggesting some bright spots.

We can dig further into the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Jacobs Solutions’s backlog reached $23.06 billion in the latest quarter and averaged 12.2% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Jacobs Solutions’s products and services but raises concerns about capacity constraints.

This quarter, Jacobs Solutions reported year-on-year revenue growth of 6.6%, and its $3.15 billion of revenue exceeded Wall Street’s estimates by 0.7%.

Looking ahead, sell-side analysts expect revenue to grow 6.9% over the next 12 months, an improvement versus the last two years. This projection is above the sector average and indicates its newer products and services will spur better top-line performance.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Jacobs Solutions was profitable over the last five years but held back by its large cost base. Its average operating margin of 6.1% was weak for a business services business.

On the plus side, Jacobs Solutions’s operating margin rose by 2.3 percentage points over the last five years.

In Q3, Jacobs Solutions generated an operating margin profit margin of 6.7%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Jacobs Solutions, its EPS and revenue declined by 1.1% and 2.4% annually over the last five years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Jacobs Solutions’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Jacobs Solutions, its two-year annual EPS growth of 1.1% was higher than its five-year trend. Accelerating earnings growth is almost always an encouraging data point.

In Q3, Jacobs Solutions reported adjusted EPS of $1.75, up from $1.41 in the same quarter last year. This print beat analysts’ estimates by 4.2%. Over the next 12 months, Wall Street expects Jacobs Solutions’s full-year EPS of $6.05 to grow 17.1%.

Key Takeaways from Jacobs Solutions’s Q3 Results

It was good to see Jacobs Solutions beat analysts’ EPS expectations this quarter. We were also happy its full-year EPS guidance narrowly outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock traded up 1.4% to $147.10 immediately following the results.

Sure, Jacobs Solutions had a solid quarter, but if we look at the bigger picture, is this stock a buy? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.