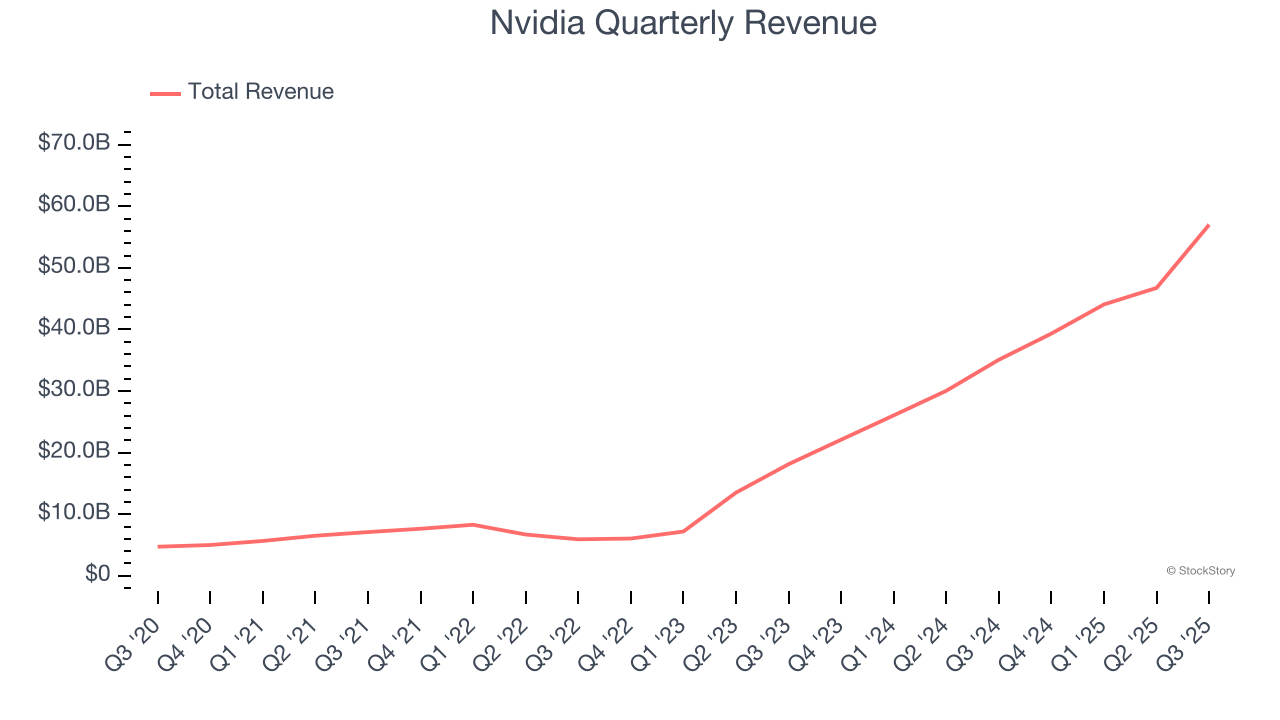

Leading designer of graphics chips Nvidia (NASDAQ:NVDA) reported Q3 CY2025 results topping the market’s revenue expectations, with sales up 62.5% year on year to $57.01 billion. On top of that, next quarter’s revenue guidance ($65 billion at the midpoint) was surprisingly good and 4.2% above what analysts were expecting. Its non-GAAP profit of $1.30 per share was 3.8% above analysts’ consensus estimates.

Is now the time to buy Nvidia? Find out by accessing our full research report, it’s free for active Edge members.

Nvidia (NVDA) Q3 CY2025 Highlights:

- Revenue: $57.01 billion vs analyst estimates of $55.45 billion (62.5% year-on-year growth, 2.8% beat)

- Adjusted EPS: $1.30 vs analyst estimates of $1.25 (3.8% beat)

- Adjusted Operating Income: $37.75 billion vs analyst estimates of $36.14 billion (66.2% margin, 4.5% beat)

- Revenue Guidance for Q4 CY2025 is $65 billion at the midpoint, above analyst estimates of $62.38 billion

- Operating Margin: 63.2%, in line with the same quarter last year

- Free Cash Flow Margin: 38.7%, down from 47.9% in the same quarter last year

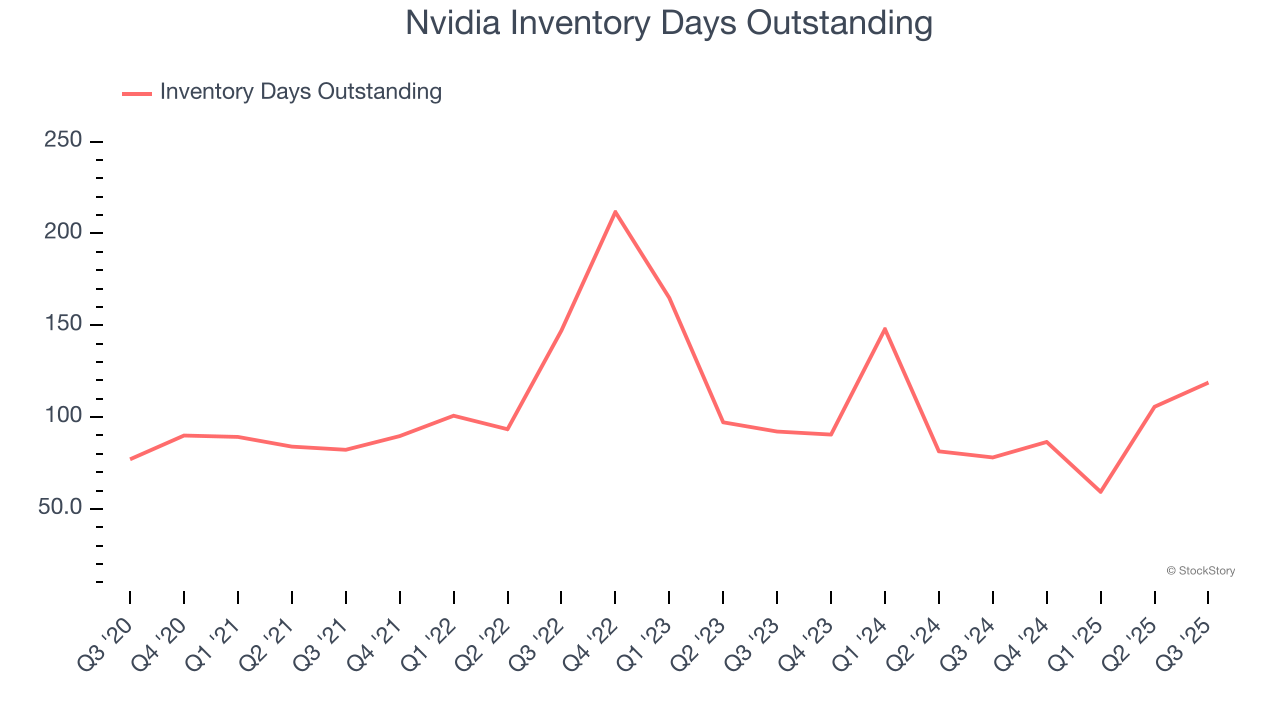

- Inventory Days Outstanding: 119, up from 106 in the previous quarter

- Market Capitalization: $4.41 trillion

“Blackwell sales are off the charts, and cloud GPUs are sold out,” said Jensen Huang, founder and CEO of NVIDIA.

Company Overview

Founded in 1993 by Jensen Huang and two former Sun Microsystems engineers, Nvidia (NASDAQ:NVDA) is a leading fabless designer of chips used in gaming, PCs, data centers, automotive, and a variety of end markets.

Revenue Growth

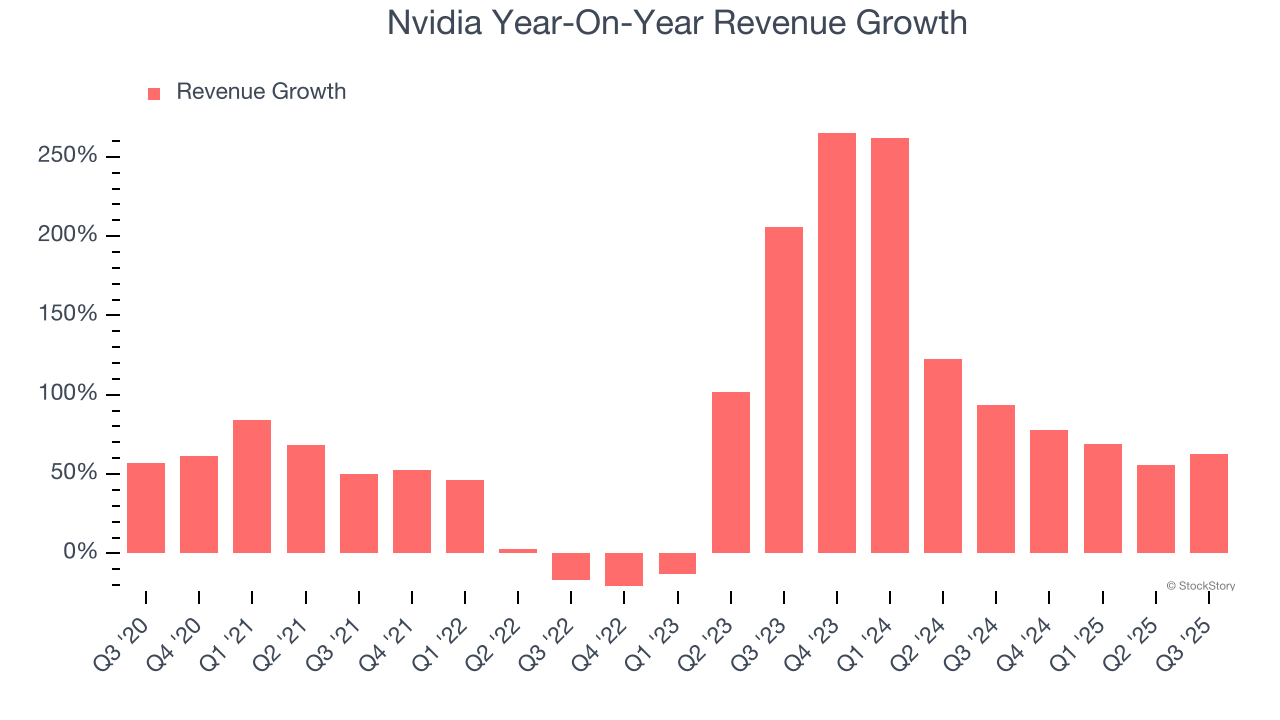

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Nvidia grew its sales at an incredible 66.2% compounded annual growth rate. Its growth surpassed the average semiconductor company and shows its offerings resonate with customers, a great starting point for our analysis. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions (which can sometimes offer opportune times to buy).

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. Nvidia’s annualized revenue growth of 104% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Nvidia reported magnificent year-on-year revenue growth of 62.5%, and its $57.01 billion of revenue beat Wall Street’s estimates by 2.8%. Beyond the beat, this marks 10 straight quarters of growth, showing that the current upcycle has had a good run - a typical upcycle usually lasts 8-10 quarters. Company management is currently guiding for a 65.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 49.1% over the next 12 months, a deceleration versus the last two years. Still, this projection is eye-popping given its scale and implies the market sees success for its products and services.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Nvidia’s DIO came in at 119, which is 13 days above its five-year average, suggesting that the company’s inventory has grown to higher levels than we’ve seen in the past.

Key Takeaways from Nvidia’s Q3 Results

It was great to see Nvidia’s revenue guidance for next quarter top analysts’ expectations. We were also glad its adjusted operating income outperformed Wall Street’s estimates. On the other hand, its inventory levels materially increased. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 2.3% to $191.20 immediately following the results.

Nvidia put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.