Earnings results often indicate what direction a company will take in the months ahead. With Q2 behind us, let’s have a look at Zeta Global (NYSE:ZETA) and its peers.

The digital advertising market is large, growing, and becoming more diverse, both in terms of audiences and media. As a result, there is a growing need for software that enables advertisers to use data to automate and optimize ad placements.

The 7 advertising software stocks we track reported a satisfactory Q2. As a group, revenues beat analysts’ consensus estimates by 2.6% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady as they are up 2.2% on average since the latest earnings results.

Best Q2: Zeta Global (NYSE:ZETA)

Powered by an AI engine that processes over one trillion consumer signals monthly, Zeta Global (NYSE:ZETA) operates a data-driven cloud platform that helps companies target, connect, and engage with consumers through personalized marketing across channels like email, social media, and video.

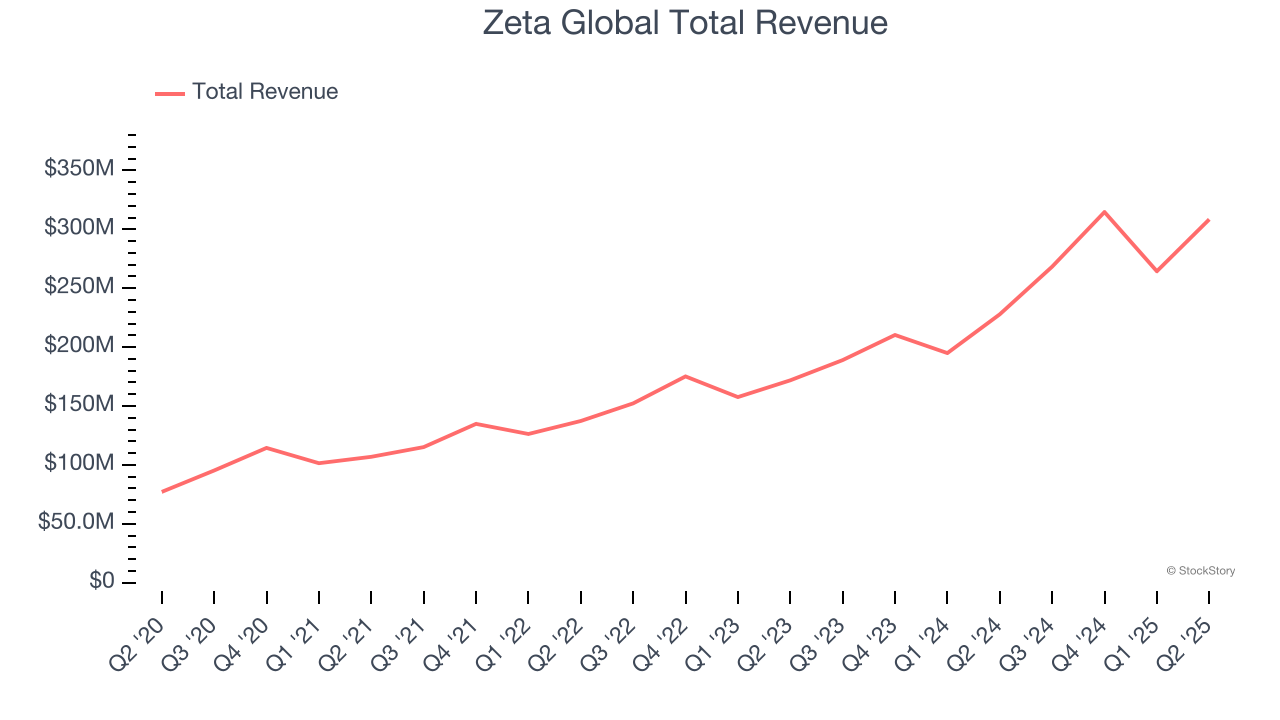

Zeta Global reported revenues of $308.4 million, up 35.4% year on year. This print exceeded analysts’ expectations by 3.9%. Overall, it was a very strong quarter for the company with an impressive beat of analysts’ EBITDA estimates and full-year EBITDA guidance exceeding analysts’ expectations.

Zeta Global achieved the fastest revenue growth and highest full-year guidance raise of the whole group. Unsurprisingly, the stock is up 20.9% since reporting and currently trades at $19.20.

DoubleVerify (NYSE:DV)

Using advanced analytics to evaluate over 17 billion digital ad transactions daily, DoubleVerify (NYSE:DV) provides AI-powered technology that verifies digital ads are viewable, fraud-free, brand-suitable, and displayed in the intended geographic location.

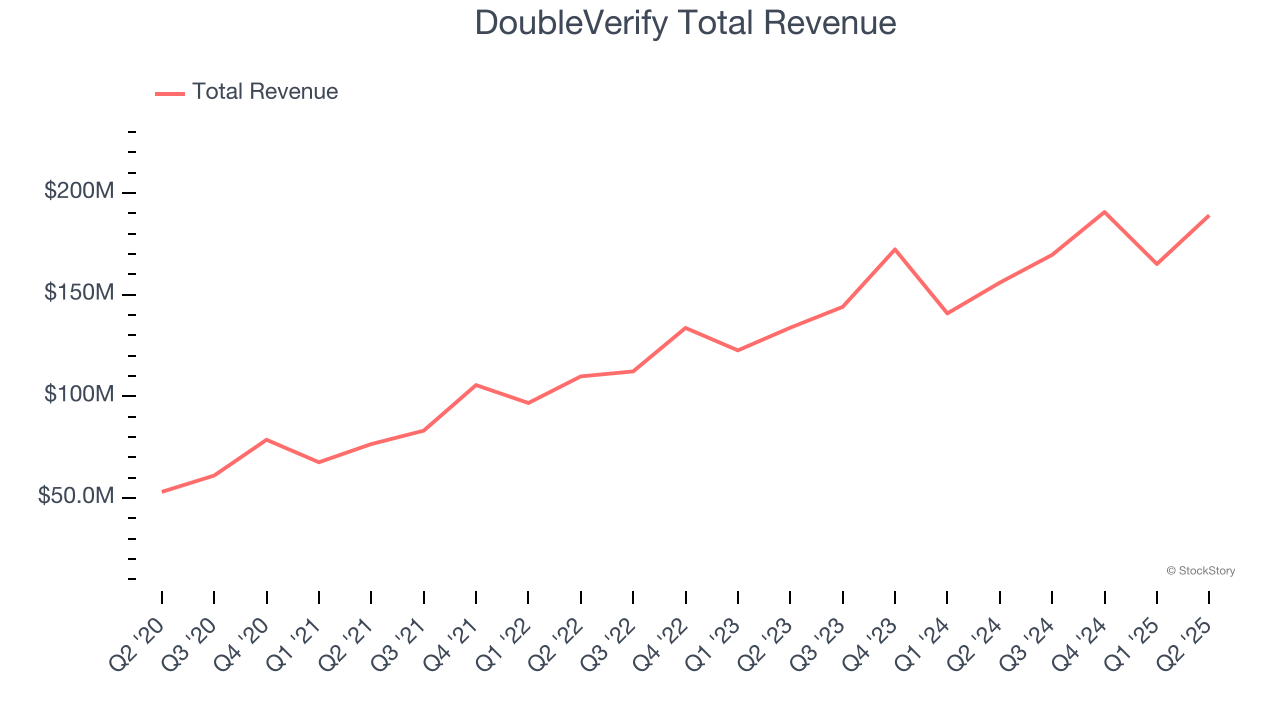

DoubleVerify reported revenues of $189 million, up 21.3% year on year, outperforming analysts’ expectations by 4.5%. The business had a strong quarter with an impressive beat of analysts’ EBITDA estimates and EBITDA guidance for next quarter slightly topping analysts’ expectations.

DoubleVerify delivered the biggest analyst estimates beat among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 26.7% since reporting. It currently trades at $11.34.

Is now the time to buy DoubleVerify? Access our full analysis of the earnings results here, it’s free.

Slowest Q2: AppLovin (NASDAQ:APP)

Sitting at the crossroads of the mobile advertising ecosystem with over 200 free-to-play games in its portfolio, AppLovin (NASDAQ:APP) provides software solutions that help mobile app developers market, monetize, and grow their apps through AI-powered advertising and analytics tools.

AppLovin reported revenues of $1.26 billion, up 16.5% year on year, falling short of analysts’ expectations by 1.2%. It was a slower quarter as it posted revenue guidance for next quarter slightly missing analysts’ expectations.

AppLovin delivered the weakest performance against analyst estimates in the group. Interestingly, the stock is up 74.9% since the results and currently trades at $684.12.

Read our full analysis of AppLovin’s results here.

The Trade Desk (NASDAQ:TTD)

Built as an alternative to "walled garden" advertising ecosystems, The Trade Desk (NASDAQ:TTD) provides a cloud-based platform that helps advertisers and agencies plan, manage, and optimize digital advertising campaigns across multiple channels and devices.

The Trade Desk reported revenues of $694 million, up 18.7% year on year. This result surpassed analysts’ expectations by 1.2%. More broadly, it was a mixed quarter as it also recorded an impressive beat of analysts’ EBITDA estimates but a miss of analysts’ billings estimates.

The stock is down 42.3% since reporting and currently trades at $50.95.

Read our full, actionable report on The Trade Desk here, it’s free.

LiveRamp (NYSE:RAMP)

Serving as the digital middleman in an increasingly privacy-conscious world, LiveRamp (NYSE:RAMP) provides technology that helps companies securely share and connect their customer data with trusted partners while maintaining privacy compliance.

LiveRamp reported revenues of $194.8 million, up 10.7% year on year. This number topped analysts’ expectations by 1.9%. Zooming out, it was a mixed quarter as it also produced a solid beat of analysts’ EBITDA estimates but a miss of analysts’ annual recurring revenue estimates.

LiveRamp had the weakest full-year guidance update among its peers. The company lost 1 enterprise customer paying more than $1 million annually and ended up with a total of 127. The stock is down 17.4% since reporting and currently trades at $26.92.

Read our full, actionable report on LiveRamp here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.