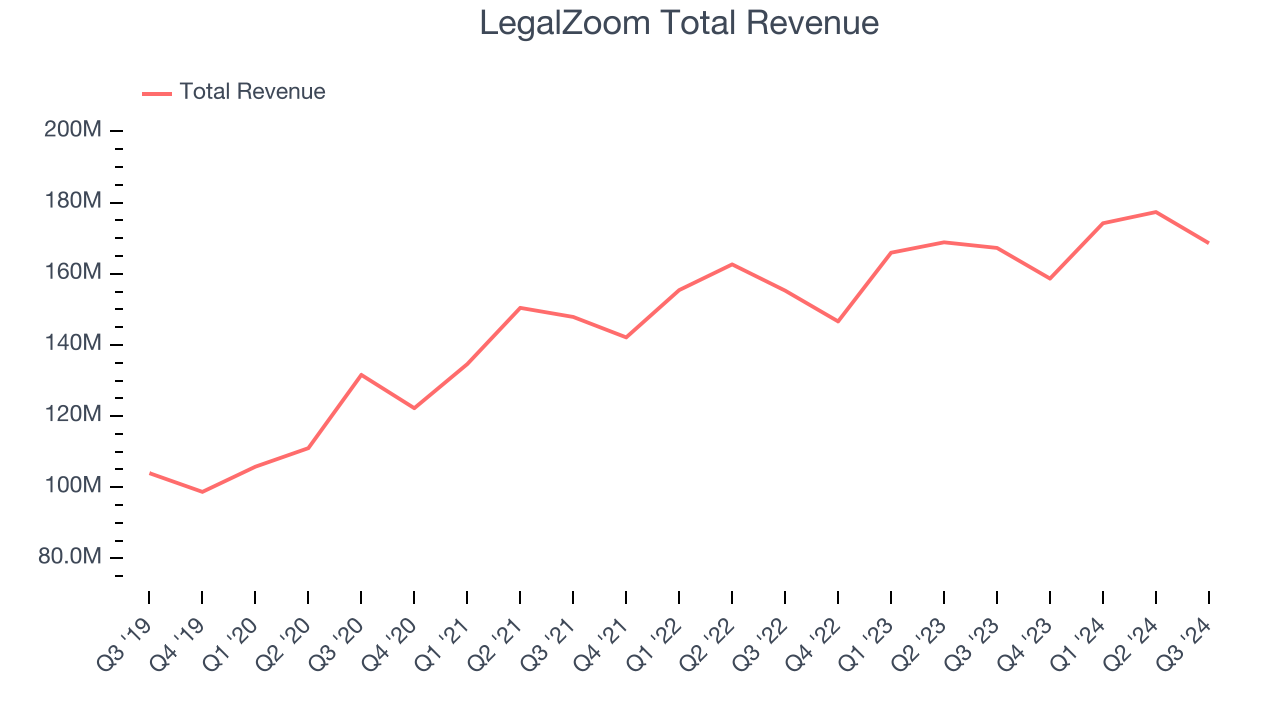

Online legal service provider LegalZoom (NASDAQ:LZ) met Wall Street’s revenue expectations in Q3 CY2024, but sales were flat year on year at $168.6 million. On the other hand, next quarter’s revenue guidance of $160 million was less impressive, coming in 1.3% below analysts’ estimates. Its GAAP profit of $0.06 per share was 29.4% above analysts’ consensus estimates.

Is now the time to buy LegalZoom? Find out by accessing our full research report, it’s free.

LegalZoom (LZ) Q3 CY2024 Highlights:

- Revenue: $168.6 million vs analyst estimates of $167.7 million (in line)

- EPS: $0.06 vs analyst estimates of $0.05 (29.4% beat)

- EBITDA: $47.1 million vs analyst estimates of $39.61 million (18.9% beat)

- Revenue Guidance for Q4 CY2024 is $160 million at the midpoint, below analyst estimates of $162.1 million

- EBITDA guidance for the full year is $146 million at the midpoint, above analyst estimates of $138.7 million

- Gross Margin (GAAP): 67.5%, up from 64.6% in the same quarter last year

- Operating Margin: 9.6%, up from 6.1% in the same quarter last year

- EBITDA Margin: 27.9%, up from 20.2% in the same quarter last year

- Free Cash Flow Margin: 13%, up from 9.8% in the previous quarter

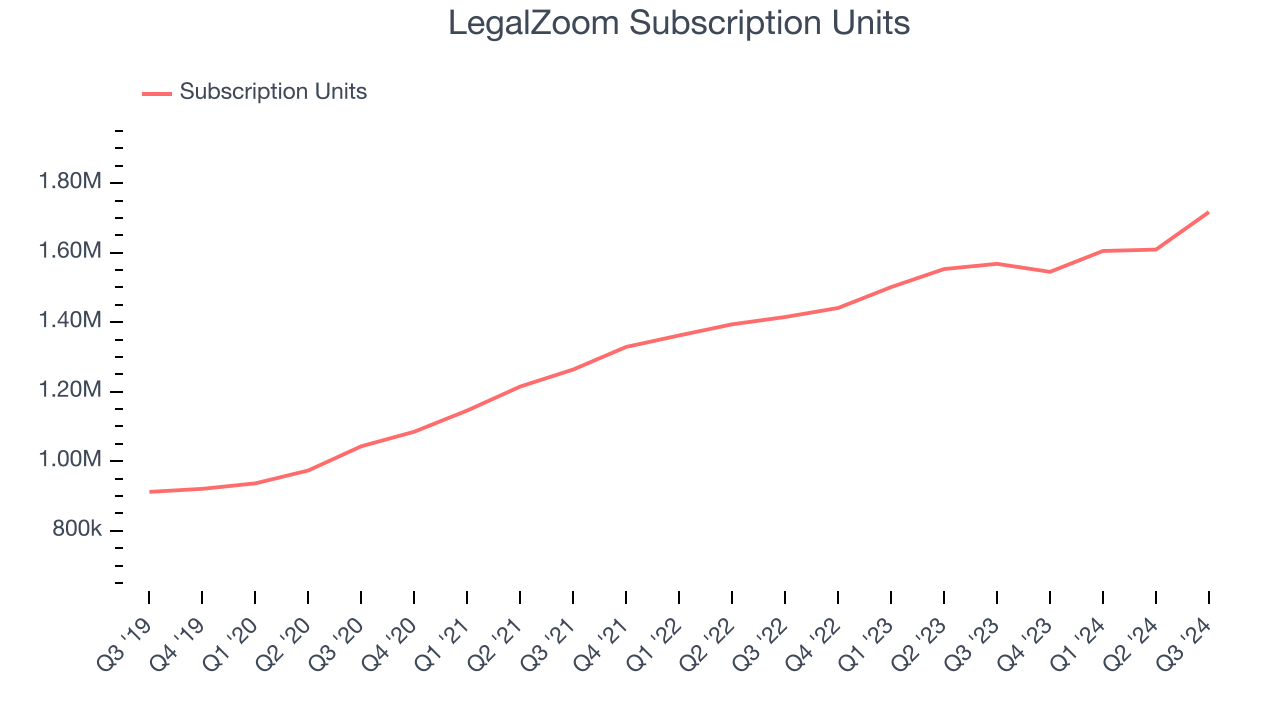

- Subscription Units: 1.72 million, up 149,000 year on year

- Market Capitalization: $1.33 billion

“I am pleased with the early strides we are making against our key execution priorities,” said Jeff Stibel, Chairman and Chief Executive Officer of LegalZoom.

Company Overview

Founded by famous lawyer Robert Shapiro, LegalZoom (NASDAQ:LZ) offers online legal services and documentation assistance for individuals and businesses.

Online Marketplace

Marketplaces have existed for centuries. Where once it was a main street in a small town or a mall in the suburbs, sellers benefitted from proximity to one another because they could draw customers by offering convenience and selection. Today, a myriad of online marketplaces fulfill that same role, aggregating large customer bases, which attracts commission-paying sellers, generating flywheel scale effects that feed back into further customer acquisition.

Sales Growth

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Unfortunately, LegalZoom’s 6.9% annualized revenue growth over the last three years was tepid. This shows it failed to expand in any major way, a rough starting point for our analysis.

This quarter, LegalZoom’s $168.6 million of revenue was flat year on year and in line with Wall Street’s estimates. Management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 1.5% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and illustrates the market believes its products and services will face some demand challenges.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Subscription Units

User Growth

As an online marketplace, LegalZoom generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Over the last two years, LegalZoom’s subscription units, a key performance metric for the company, increased by 8.5% annually to 1.72 million in the latest quarter. This growth rate is decent for a consumer internet business and indicates people enjoy using its offerings.

In Q3, LegalZoom added 149,000 subscription units, leading to 9.5% year-on-year growth. The quarterly print isn’t too different from its two-year result, suggesting its new initiatives aren’t accelerating user growth just yet.

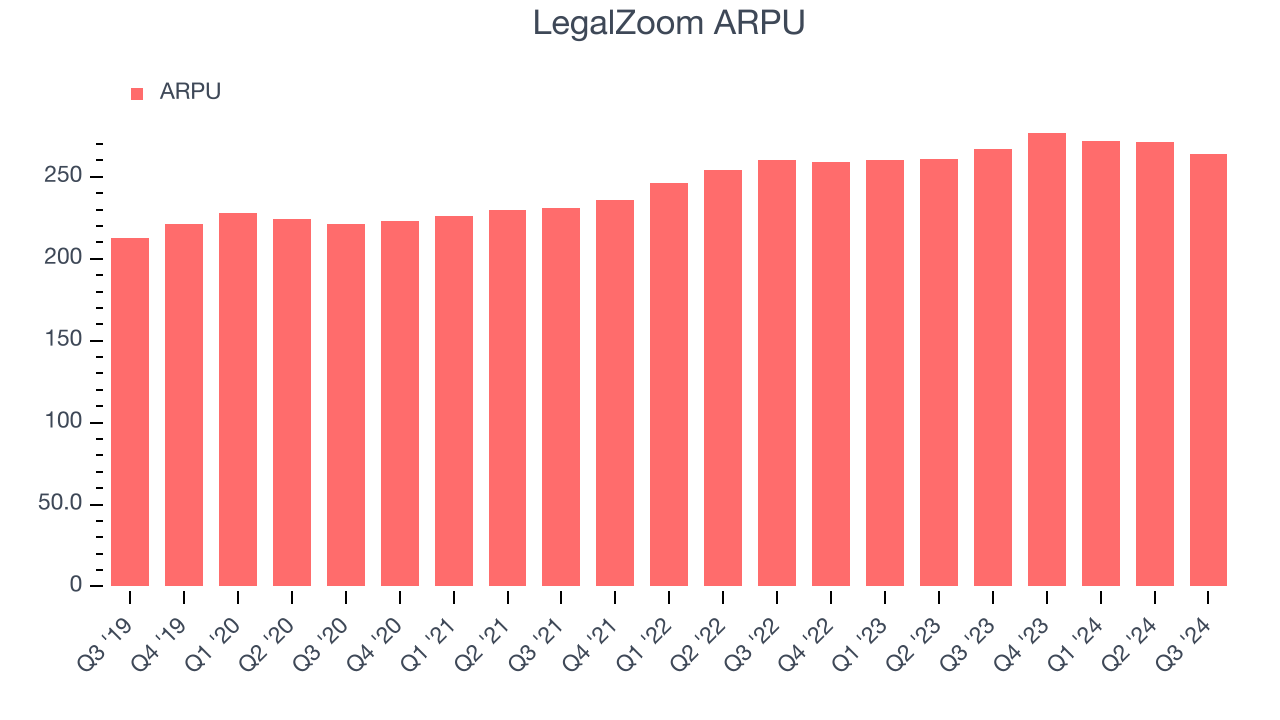

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track for consumer internet businesses like LegalZoom because it measures how much the company earns in transaction fees from each user. ARPU also gives us unique insights into a user’s average order size and LegalZoom’s take rate, or "cut", on each order.

LegalZoom’s ARPU growth has been mediocre over the last two years, averaging 4.4%. This isn’t great, but the increase in subscription units is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if LegalZoom tries boosting ARPU by taking a more aggressive approach to monetization, it’s unclear whether users can continue growing at the current pace.

This quarter, LegalZoom’s ARPU clocked in at $264. It declined 1.1% year on year, worse than the change in its subscription units.

Key Takeaways from LegalZoom’s Q3 Results

We were impressed by how significantly LegalZoom blew past analysts’ EPS and EBITDA expectations this quarter. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed. Overall, this quarter had some key positives. The stock traded up 6.5% to $8.66 immediately after reporting.

So should you invest in LegalZoom right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.