Higher education company Grand Canyon Education (NASDAQ:LOPE) will be reporting results tomorrow after market close. Here’s what investors should know.

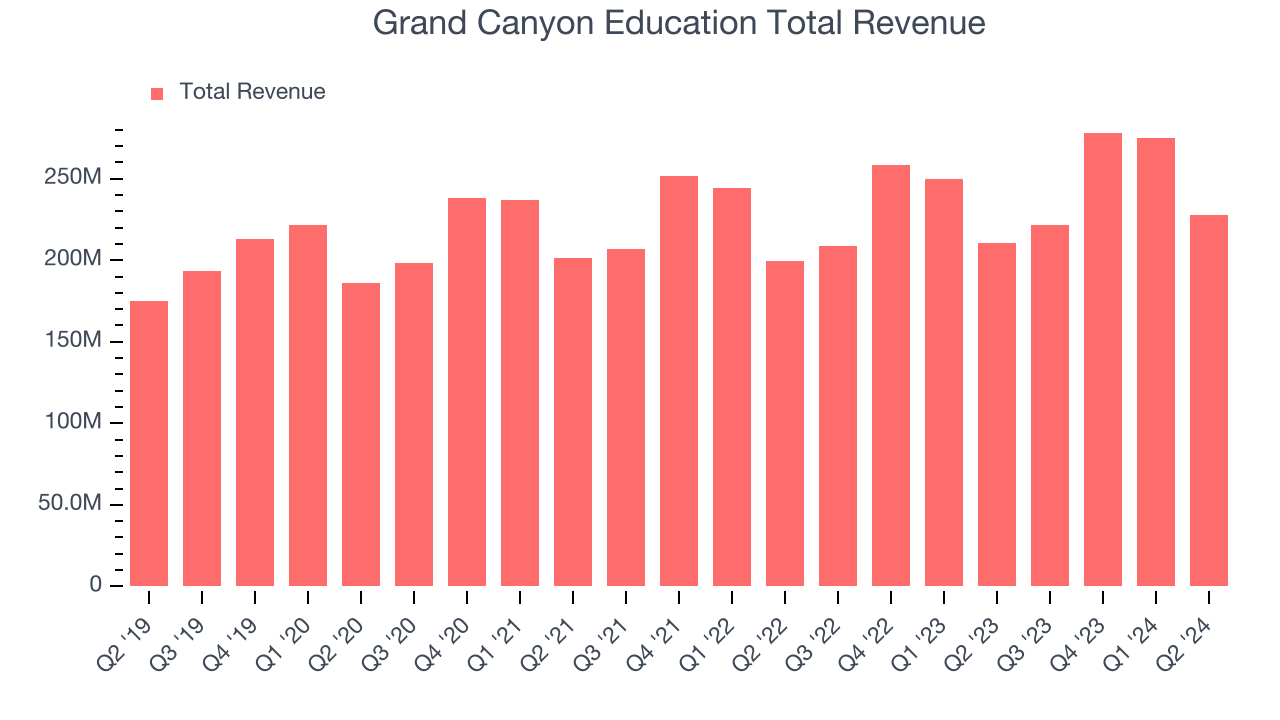

Grand Canyon Education beat analysts’ revenue expectations by 1.7% last quarter, reporting revenues of $227.5 million, up 8% year on year. It was a strong quarter for the company, with an impressive beat of analysts’ operating margin estimates. It reported 106,307 total students, up 6.8% year on year.

Is Grand Canyon Education a buy or sell going into earnings? Read our full analysis here, it’s free.

This quarter, analysts are expecting Grand Canyon Education’s revenue to grow 8% year on year to $239.7 million, improving from the 6.3% increase it recorded in the same quarter last year. Adjusted earnings are expected to come in at $1.47 per share.

Analysts covering the company have generally reconfirmed their estimates over the last 30 days, suggesting they anticipate the business to stay the course heading into earnings. Grand Canyon Education has a history of exceeding Wall Street’s expectations, beating revenue estimates every single time over the past two years by 0.9% on average.

Looking at Grand Canyon Education’s peers in the education services segment, some have already reported their Q3 results, giving us a hint as to what we can expect. Adtalem delivered year-on-year revenue growth of 13.2%, beating analysts’ expectations by 5%, and Laureate Education reported revenues up 2%, topping estimates by 1.9%. Adtalem’s stock price was unchanged after the results, and Laureate Education’s price followed a similar reaction.

Read our full analysis of Adtalem’s results here and Laureate Education’s results here.

Investors in the education services segment have had steady hands going into earnings, with share prices up 2% on average over the last month. Grand Canyon Education’s stock price was unchanged during the same time and is heading into earnings with an average analyst price target of $162.33 (compared to the current share price of $137.33).

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.