Over the past six months, Quanex’s shares (currently trading at $28.81) have posted a disappointing 9.6% loss, well below the S&P 500’s 13% gain. This might have investors contemplating their next move.

Is there a buying opportunity in Quanex, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.Even with the cheaper entry price, we're swiping left on Quanex for now. Here are three reasons why NX doesn't excite us and a stock we'd rather own.

Why Is Quanex Not Exciting?

Starting in the seamless tube industry, Quanex (NYSE:NX) manufactures building products like window, door, kitchen, and bath cabinet components.

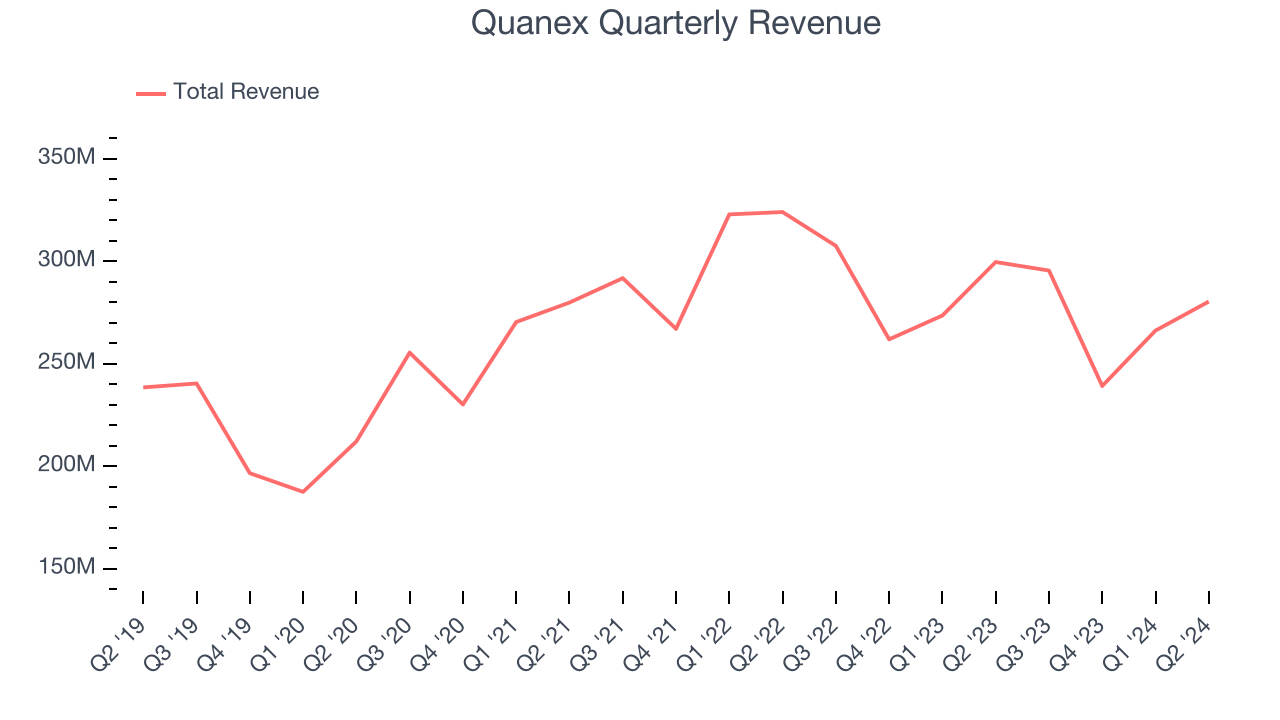

1. Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Quanex’s sales grew at a sluggish 3.8% compounded annual growth rate over the last five years. This fell short of our benchmark for the industrials sector.

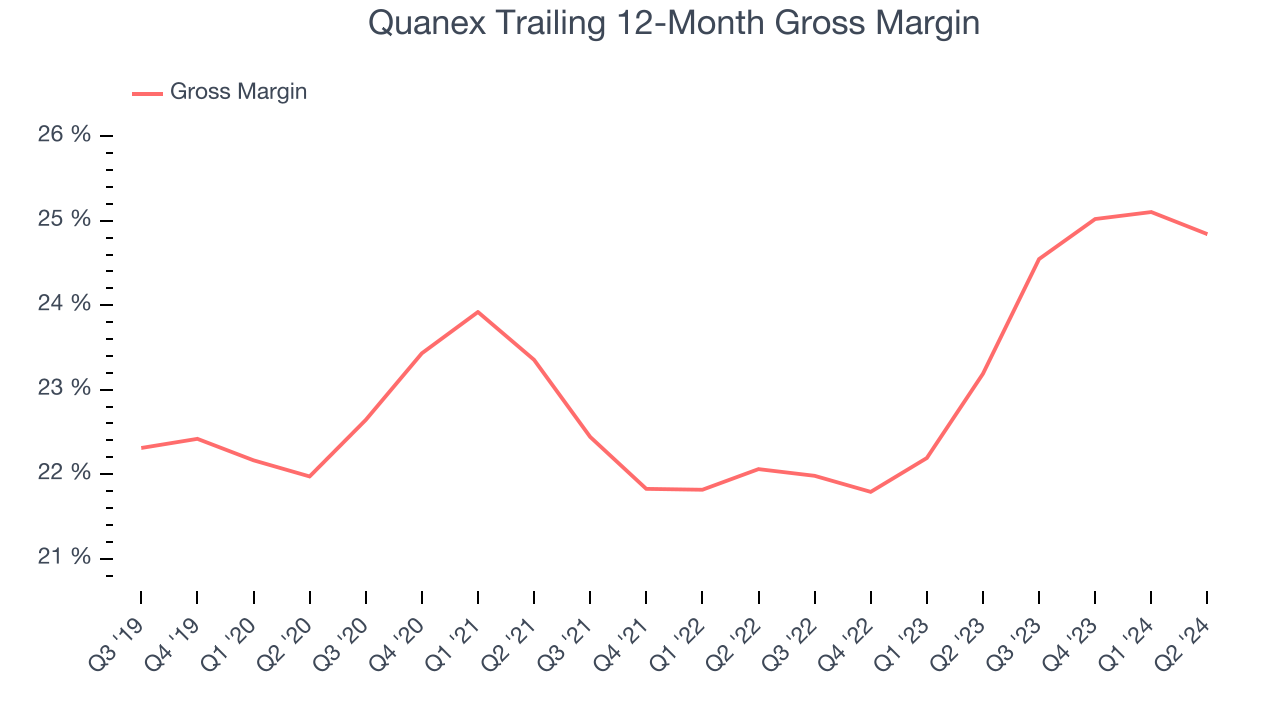

2. Low Gross Margin Reveals Weak Structural Profitability

Gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

Quanex has weak unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 23.1% gross margin over the last five years. That means Quanex paid its suppliers a lot of money ($76.89 for every $100 in revenue) to run its business.

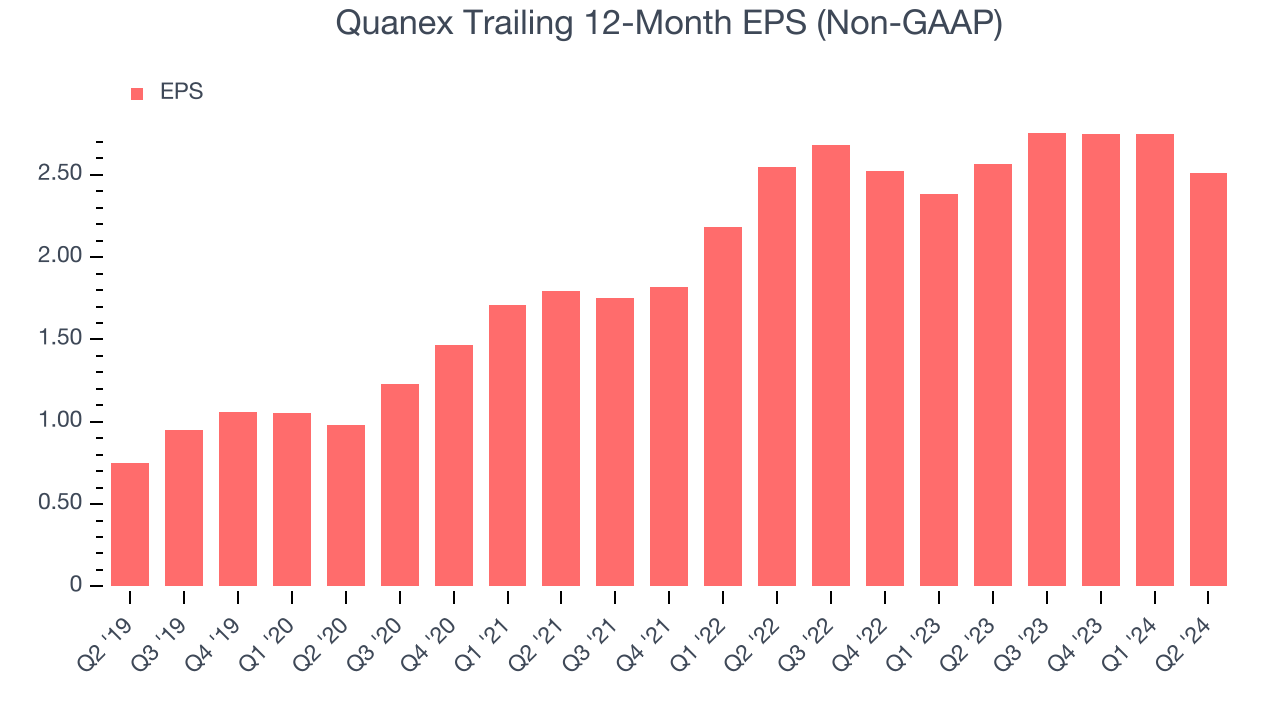

3. EPS Growth Has Stalled Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Quanex’s flat EPS over the last two years was weak. On the bright side, this performance was better than its 5.3% annualized revenue declines.

Final Judgment

Quanex’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 10.4x forward price-to-earnings (or $28.81 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now. Let us point you toward Costco, one of Charlie Munger’s all-time favorite businesses.

Stocks We Would Buy Instead of Quanex

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.