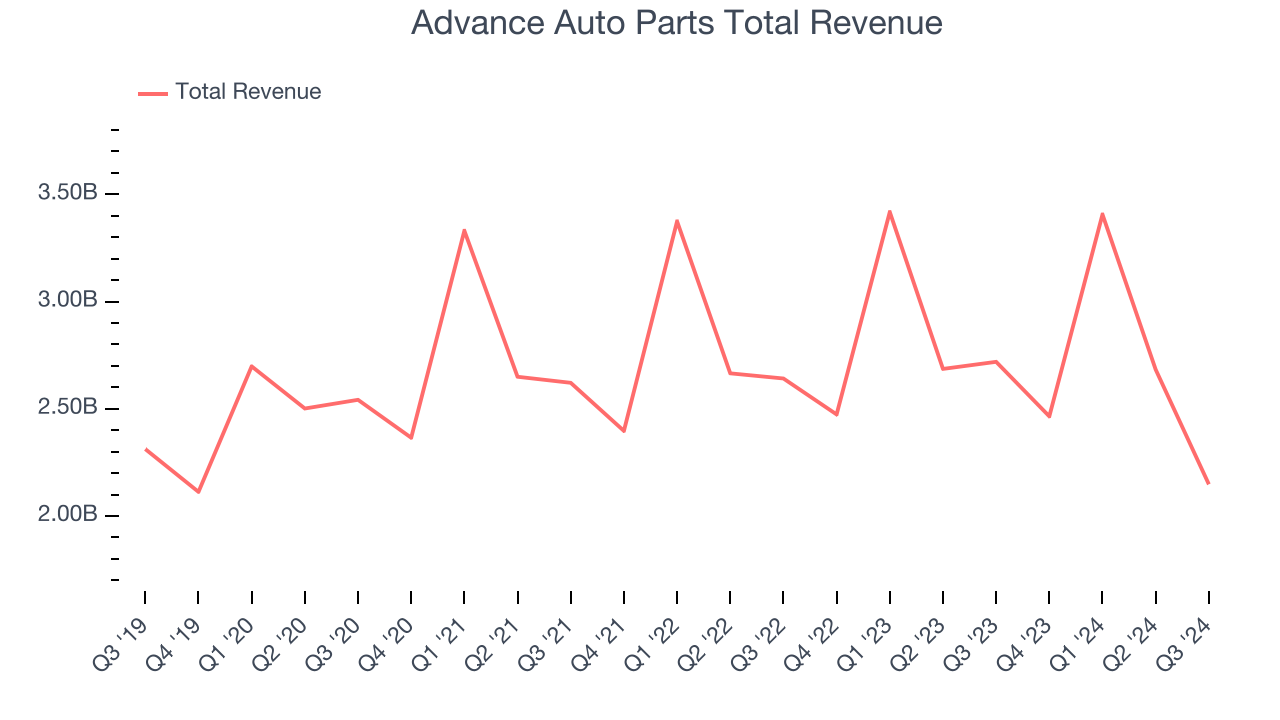

Auto parts and accessories retailer Advance Auto Parts (NYSE:AAP) missed Wall Street’s revenue expectations in Q3 CY2024, with sales falling 21% year on year to $2.15 billion. The company’s full-year revenue guidance of $9 billion at the midpoint came in 7.2% below analysts’ estimates. Its non-GAAP loss of $0.04 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Advance Auto Parts? Find out by accessing our full research report, it’s free.

Advance Auto Parts (AAP) Q3 CY2024 Highlights:

- Revenue: $2.15 billion vs analyst estimates of $2.67 billion (19.6% miss)

- Adjusted EPS: -$0.04 vs analyst estimates of $0.06 (significant miss)

- Adjusted EBITDA: $83.97 million vs analyst estimates of $138.6 million (39.4% miss)

- The company dropped its revenue guidance for the full year to $9 billion at the midpoint from $11.2 billion, a 19.6% decrease

- Adjusted EPS guidance for the full year is -$0.30 at the midpoint, missing analyst estimates by 118%

- Gross Margin (GAAP): 42.3%, up from 36.3% in the same quarter last year

- Operating Margin: 0%, up from -2.2% in the same quarter last year

- EBITDA Margin: 3.9%, up from 2.8% in the same quarter last year

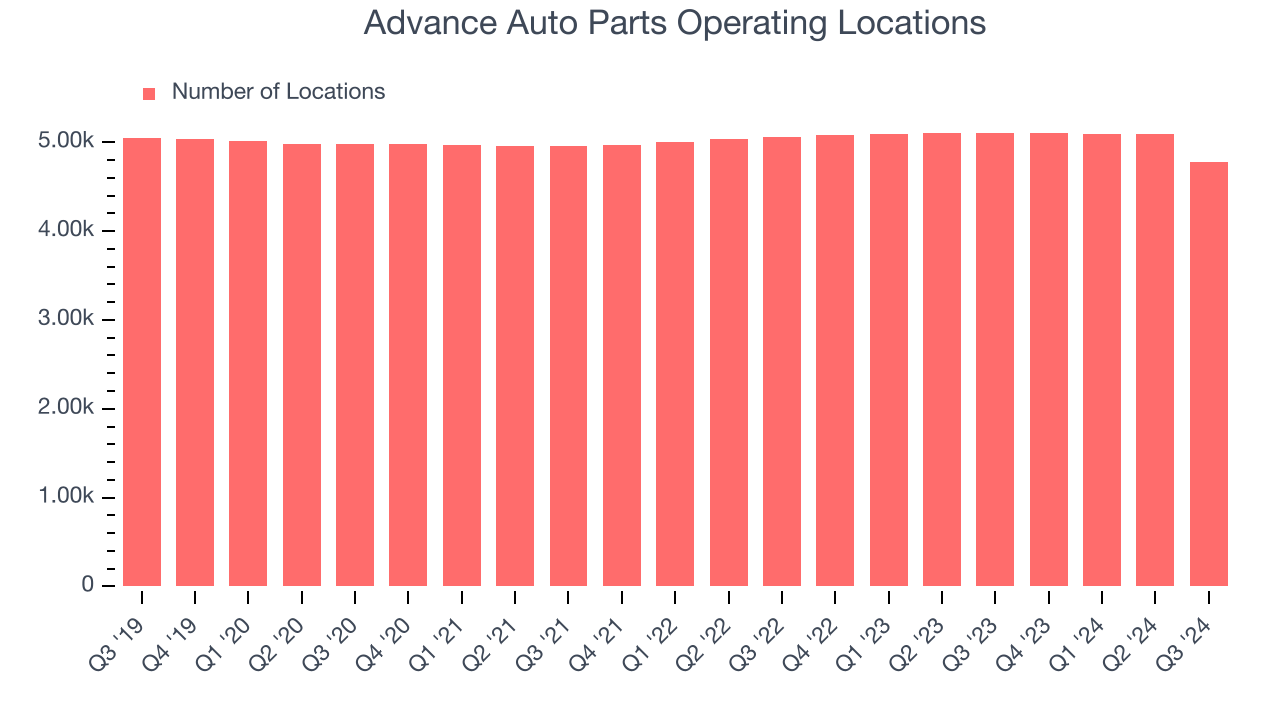

- Locations: 4,781 at quarter end, down from 5,105 in the same quarter last year

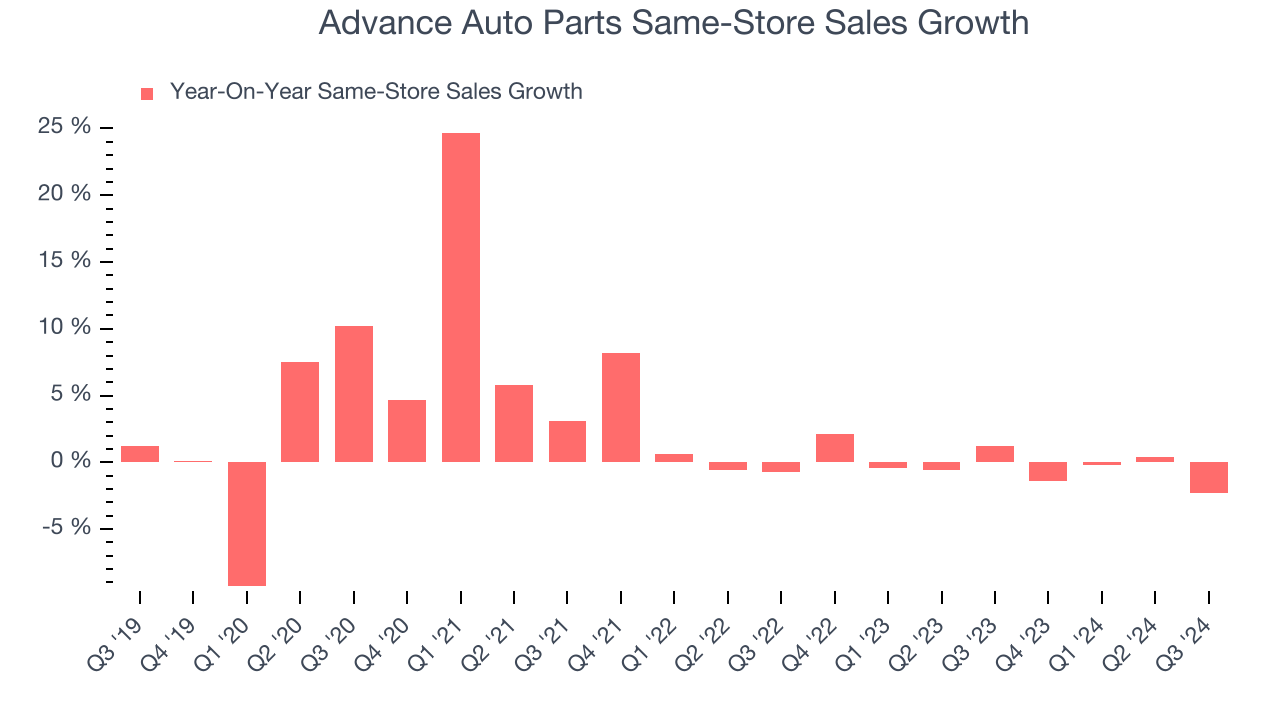

- Same-Store Sales fell 2.3% year on year (1.2% in the same quarter last year)

- Market Capitalization: $2.43 billion

"We are pleased to have made progress on our strategic actions, including the completion of the sale of Worldpac and a comprehensive operational productivity review of our business,” said Shane O’Kelly, president and chief executive officer.

Company Overview

Founded in Virginia in 1932, Advance Auto Parts (NYSE:AAP) is an auto parts and accessories retailer that sells everything from carburetors to motor oil to car floor mats.

Auto Parts Retailer

Cars are complex machines that need maintenance and occasional repairs, and auto parts retailers cater to the professional mechanic as well as the do-it-yourself (DIY) fixer. Work on cars may entail replacing fluids, parts, or accessories, and these stores have the parts and accessories or these jobs. While e-commerce competition presents a risk, these stores have a leg up due to the combination of broad and deep selection as well as expertise provided by sales associates. Another change on the horizon could be the increasing penetration of electric vehicles.

Sales Growth

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

Advance Auto Parts is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Advance Auto Parts’s sales grew at a sluggish 2% compounded annual growth rate over the last five years (we compare to 2019 to normalize for COVID-19 impacts) as it didn’t open many new stores.

This quarter, Advance Auto Parts missed Wall Street’s estimates and reported a rather uninspiring 21% year-on-year revenue decline, generating $2.15 billion of revenue.

Looking ahead, sell-side analysts expect revenue to decline 12.8% over the next 12 months, a deceleration versus the last five years. This projection doesn't excite us and implies its products will face some demand challenges.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Store Performance

Number of Stores

Advance Auto Parts listed 4,781 locations in the latest quarter and has kept its store count flat over the last two years while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Advance Auto Parts’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and we’d be skeptical if Advance Auto Parts starts opening new stores to artificially boost revenue growth.

In the latest quarter, Advance Auto Parts’s same-store sales fell by 2.3% year on year. This decrease represents a further deceleration from its historical levels. We hope the business can get back on track.

Key Takeaways from Advance Auto Parts’s Q3 Results

We enjoyed seeing Advance Auto Parts exceed analysts’ gross margin expectations this quarter. On the other hand, its full-year revenue guidance missed significantly and its full-year EPS guidance fell meaningfully short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 13.2% to $35.50 immediately after reporting.

Advance Auto Parts didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.