Wayfair Inc. (NYSE: W) is an e-commerce platform specializing in furniture and home goods. The components of its name, Way and Fair, imply a wide range of products at a fair price. The consumer discretionary company has launched a number of initiatives to give itself an edge over its competitors, including IKEA, Amazon.com Inc. (NASDAQ: AMZN), Overstock.com Inc. (NASDAQ: OSTK), Haverty Furniture Co. (NYSE: HVT), Walmart Inc. (NYSE: WMT) and Target Co. (NYSE: TGT).

Easy Access and Convenience are Performance Drivers

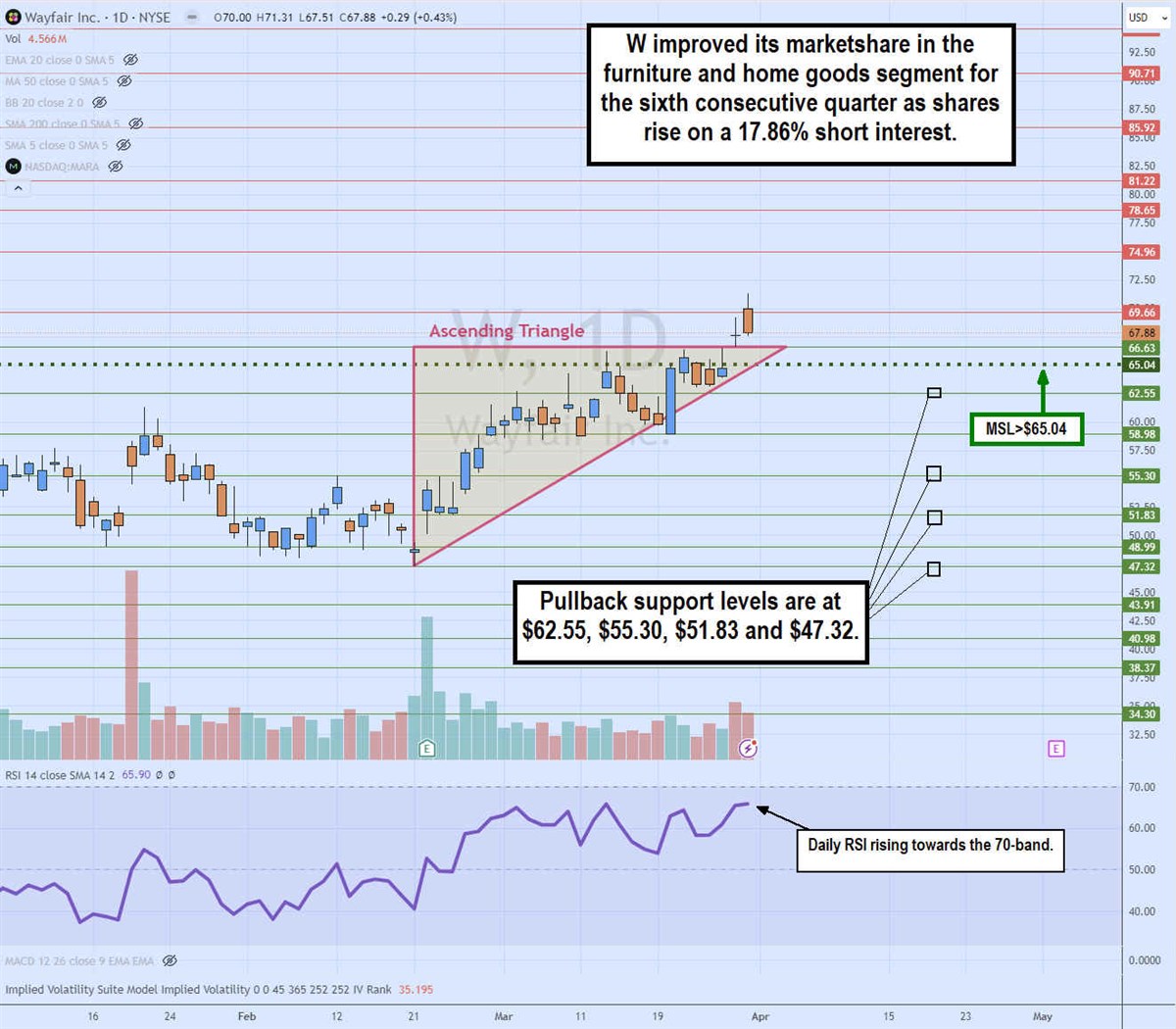

Wayfair makes furniture shopping convenient by giving consumers access to everything it offers with a few keystrokes, saving shoppers the time-consuming chore of physically walking through showrooms. It also allows consumers to filter by style, brand or item to find what they want. Wayfair often has 72-hour Clearout sales with savings of up to 60%. The company has been in a turnaround, and its financials continue to improve. Notably, it has a 17.86% short interest, making it susceptible to short squeezes.

Online Shopping Creates Tailwinds

High interest rates, elevated prices and a low supply of homes may have caused a slowdown in the housing market, but it can be a boon for home improvement and furnishings. Wayfair also benefits from tailwinds created by customers shifting to online furniture shopping and e-commerce over walking through a furniture store. This migration to internet shopping is driving Wayfair's outperformance of the home furnishing industry average. Free shipping, a loyalty program and white glove delivery further attract customers to the platform.

Flexing Stronger Financials

Wayfair announced a Q4 2023 EPS loss of 11 cents, which was 4 cents better than consensus analyst estimates. The company's net loss was $174 million, and non-GAAP adjusted EBITDA was $92 million — up from a loss of $71 million last year. Revenues rose 0.4% YOY to $3.11 billion, matching consensus estimates. Wayfair closed 2023 with $1.4 billion in cash and cash equivalents.

Growth Metrics Are Positive Overall

Wayfair experienced 0.9% growth in United States sales, while international sales were down 2.7%. Gross margins topped consensus estimates by 60bps at 30.4%. The number of active customers rose 1.4% to 22.4 million. LTM net revenue per active customer was $537, a 3% YOY decrease. Average order value came in higher than expected at $276, down 2.5% YOY. Orders delivered in Q4 2023 rose 2.7% YOY to 11.3 million. Cost-cutting initiatives resulted in 3,400 job cuts during the year. Competitors RH (NYSE: RH), formerly known as Restoration Hardware, and Williams-Sonoma Inc. (NYSE: WSM) experienced sales declines of 14% and 16%, respectively.

Guidance Is Mixed

Wayfair expects Q1 2024 revenues to rise in the mid-single digit range, with gross margins expected between 30% to 31%. EBITDA margin is anticipated to be in the low-single-digit percentage range. The company gained market share for the sixth consecutive quarter. Wayfair also deserves credit for its efficient operations as competitor Home Goods (owned by TJX Co. (NYSE: TJX)) shut down its e-commerce platform at the end of October 2023.

Analyst Actions

Morgan Stanley defended its Overweight rating on Wayfair shares with an $80 price target. Analyst Simeon Gutman sees a cyclical recovery in home-oriented stocks, expecting Wayfair to hit $900 million in adjusted EBITDA by 2025. On March 19, 2024. Mizuho initiated a Buy rating on Wayfair shares with a $72 price target.

The daily candlestick chart on Wayfair illustrates an ascending triangle pattern. The lower ascending trendline formed at $47.32 on February 21, 2024. The upper flat-top resistance trendline formed at $66.63 after three attempts to break out, with the last one finally pushing through. The daily market structure low (MSL) triggered the breakout through $65.04. The daily relative strength index (RSI) is rising through the 65-band. Pullback support levels are at $62.55, $55.30, $51.83 and $47.32.

Wayfair Thriving Despite Difficult Environment

Wayfair CEO Niraj Shah credited the company's expansion of market share to improvements in item availability, shipping speed, competitive pricing, and an increase in active customers and customer loyalty.

“Even in a difficult macro environment, we generated a 3% Adjusted EBITDA Margin and had our third consecutive quarter of positive adjusted EBITDA and Free Cash Flow. In fact, on a revenue base that largely mirrored 2022, our Free Cash Flow in 2023 improved by more than one billion dollars," Shah said.

Shah expects Q1 2024 to be the low point as the company anticipates growing EBITDA by 50% in 2024.