Fastenal (NASDAQ: FAST) and Simpson Manufacturing (NYSE: SSD) are in similar businesses with a similar outlook for growth, but 1 is the better buy for investors today. While Fastenal is growing quicker and pays a higher yield, the trajectory for growth, dividends, and distribution growth at Simpson Manufacturing is far superior. Based on revenue, earnings, and growth, Fastenal is the winner; based on the outlook for distribution growth and capital appreciation, Simpson Manufacturing is a far better buy and will deliver far superior returns.

Fastenal and Simpson Have Solid Business

Fastenal and Simpson Manufacturing have many areas of overlap. Fastenal is far more diversified. Its DTC/vending model drives business and deepens penetration by providing a valuable service for manufacturers, builders, and industry. The company’s Onsite and vending products amount to a quartermaster service to which businesses can outsource their inventory management and distribution needs.

Simpson Manufacturing is also diversified and diversifying. The company expanded its product lines to target manufacturing and automobile OEMs alongside the building industry. The company also leans into technology and provides SaaS for builders and homeowners. Regarding growth, the company is working on a new manufacturing facility in Tennessee and expansion in Europe.

Results in 2023 have been solid for both companies. Both outperform on the bottom line, Simpson on the top and bottom line, producing low-single-digit growth. The outlook for next year is favorable and includes an acceleration of growth on the top and bottom lines for each.

Fastenal is expected to grow at a slightly quicker 6% and 7% compared to 5% and 6% for Simpson, significant because Fastenal’s business is 4X as large as Simpson's, but that is not enough to overshadow Simpson's dividend outlook.

Simpson Manufacturing has Value and Distribution Strength

Fastenal is not a weak dividend. The company pays about 2.4% with shares near the 2023 high, but the valuation, payout ratio, and growth outlook pale compared to Simpson. Fastenal trades at a high 30X earnings partly because it pays nearly 70% of earnings in dividends. The company has increased the payout for 24 years and is about to be dubbed a Dividend Aristocrat, but investors should expect the pace of increases to slow, as seen in the analysts' coverage.

Analysts rate Fastenal a Hold with a price target up from last year but flat since summer and aligned with current price action. On the other hand, Simpson is rated a Moderate Buy with a price target trending higher and 35% above the price action.

Simpson Manufacturing trades at a deep discount to Fastenal, about 15X earnings, because it pays only 13% of earnings in dividends. The remainder is used to invest in growth and future cash flow to support the healthy dividend outlook.

Simpson paused annual increases during the pandemic but has a solid record of increases before and after. Simpson’s distribution CAGR is much lower, about 5%, but the pace could be increased and sustained without damaging the company’s financial health. That would be a catalyst for higher share prices and a price-multiple expansion. The takeaway is that investors looking to capture dividend growth and capital growth over a long duration will be better served by Simpson.

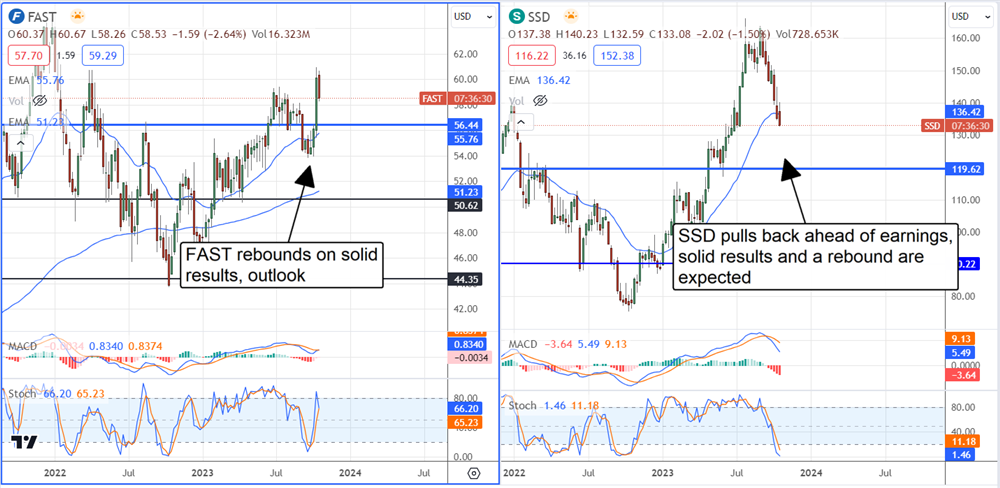

The Technical Outlook: Simpson Outperforms in 2023

Both stocks are up solid double-digits this year, but Simpson’s advance is double its competitor, about 50%, with shares near $130. The market is pulling back now but should find support soon, possibly near $130, and begin to consolidate at that level. The next catalyst is the Q3 results, due out in late October. A solid report could get SSD to the bottom sooner rather than later. FAST shares are already advancing following its report and foreshadowing bullish market action.