Bozeman, Montana-based Fair Isaac Corporation (FICO) is a software company. It develops analytic, software, and digital decisioning technologies and services that enable businesses to automate, enhance, and connect decisions. With a market cap of $42.4 billion, Fair Isaac operates through Scores and Software segments.

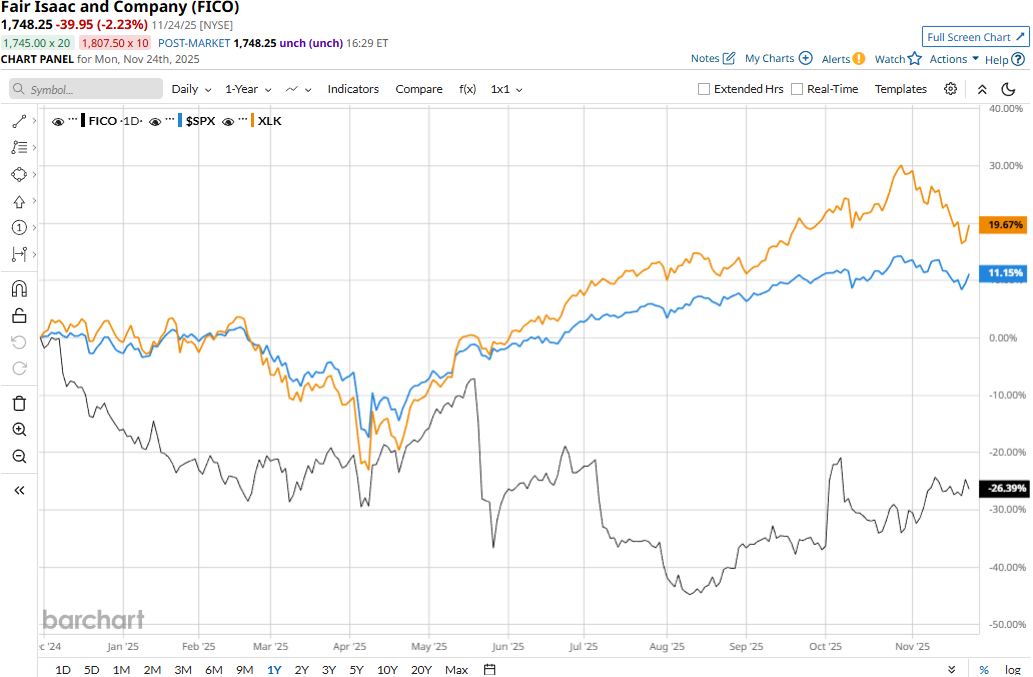

Fair Isaac has significantly underperformed the broader market over the past year. FICO stock prices have plummeted 25.8% over the past 52 weeks and 12.2% on a YTD basis, compared to the S&P 500 Index’s ($SPX) 12% returns over the past year and 14% surge in 2025.

Narrowing the focus, Fair Isaac has also underperformed the Technology Select Sector SPDR Fund’s (XLK) 19.7% surge over the past 52 weeks and 20.3% returns on a YTD basis.

Fair Isaac’s stock prices gained 2.8% in the trading session following the release of its Q3 results on Nov. 5. Although the company’s on-premises & SaaS software and professional services revenues remained tamed, its scores revenues observed a notable surge. Overall, the company’s topline for the quarter soared 13.6% year-over-year to $515.8 million, exceeding the consensus estimates by 78 bps. Meanwhile, its adjusted EPS increased 18.3% year-over-year to $7.74, beating the Street’s expectations by a notable margin.

For the full fiscal 2025, ending in December, analysts expect FICO to deliver an adjusted EPS of $33.66, up 34.3% year-over-year. The company has a mixed earnings surprise history. While it missed the Street’s bottom-line estimates once over the past four quarters, it surpassed the projections on three other occasions.

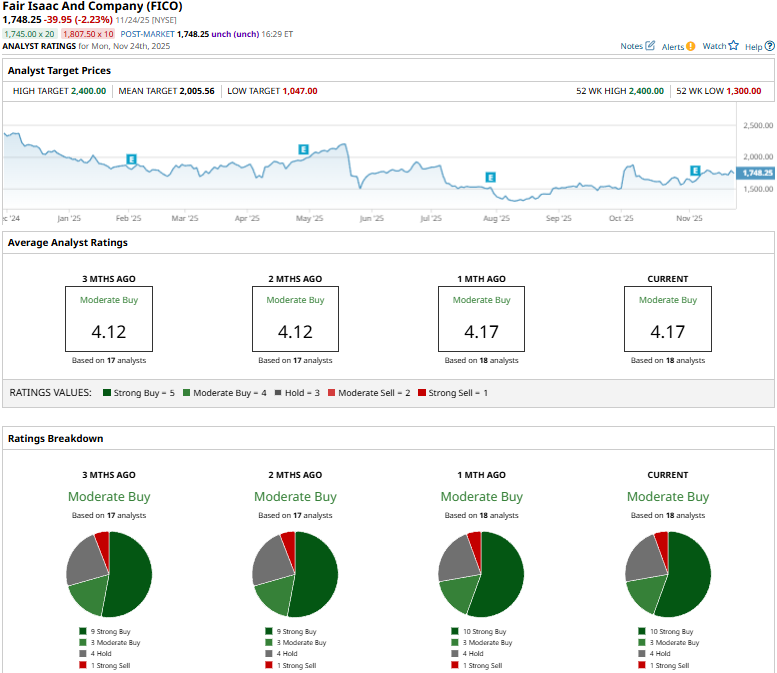

Among the 18 analysts covering the FICO stock, the consensus rating is a “Moderate Buy.” That’s based on 10 “Strong Buys,” three “Moderate Buys,” four “Holds,” and one “Strong Sell.”

This configuration is slightly more optimistic than two months ago, when only nine analysts gave “Strong Buy” recommendations.

On Nov. 6, JP Morgan (JPM) analyst Alexander Hess maintained a “Neutral” rating on FICO and raised the price target from $1,750 to $1,825.

As of writing, FICO’s mean price target of $2,005.56 represents a 14.7% premium to current price levels. Meanwhile, the street-high target of $2,400 suggests a 37.2% upside potential.

On the date of publication, Aditya Sarawgi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart