Hamilton, Bermuda-based Everest Group, Ltd. (EG) operates through its subsidiaries, provides reinsurance and insurance products in the United States, Europe, and internationally. With a market cap of $13.1 billion, Everest operates through the Insurance and Reinsurance segments.

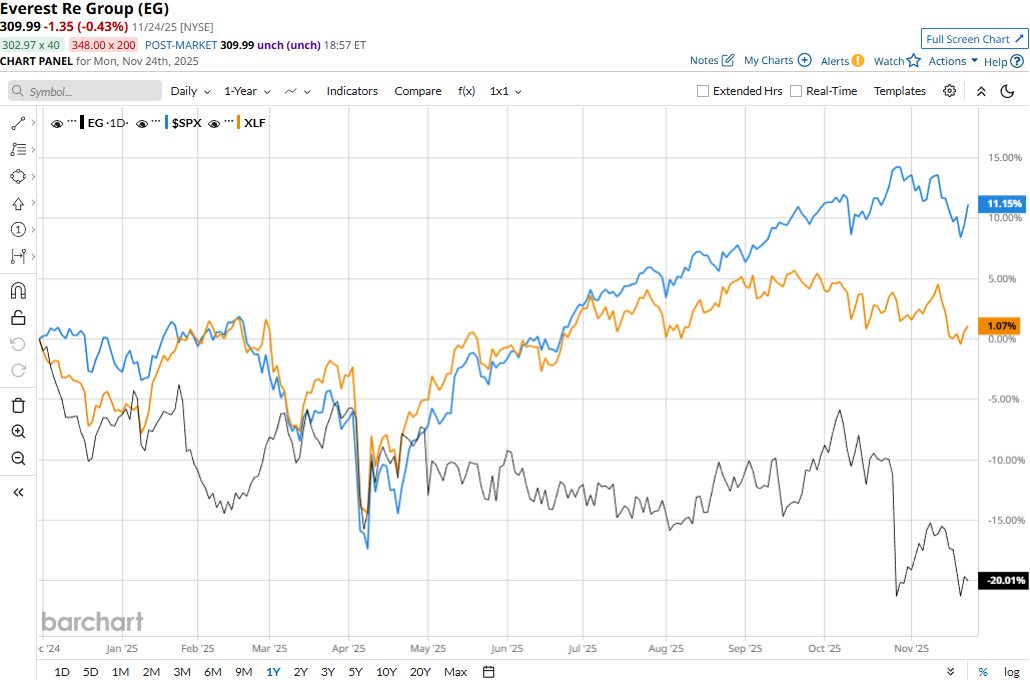

The insurance major has significantly underperformed the broader market over the past year. EG stock prices have plunged 20.3% over the past 52 weeks and 14.5% on a YTD basis, compared to the S&P 500 Index’s ($SPX) 12% returns over the past year and 14% surge in 2025.

Narrowing the focus, Everest has also underperformed the sector-focused Financial Select Sector SPDR Fund’s (XLF) 2.3% uptick over the past 52 weeks and 7.4% gains on a YTD basis.

Everest Group’s stock prices tanked 11.4% in a single trading session following the release of its disappointing Q3 results on Oct. 27. Due to a drop in premiums earned and muted growth in net investment income, the company’s overall topline for the quarter inched up by a modest 79 bps year-over-year to $4.3 billion, missing the Street’s expectations by 2.9%. Meanwhile, its net operating income per share plummeted 48.4% year-over-year to $7.54, missing the consensus estimates by a staggering 43.7%.

For the full fiscal 2025, ending in December, analysts expect EG to deliver an adjusted EPS of $45.02, up 50.9% year-over-year. However, the company has a lackluster earnings surprise history. Although it has surpassed the Street’s bottom-line estimates once over the past four quarters, it missed the projections on three other occasions.

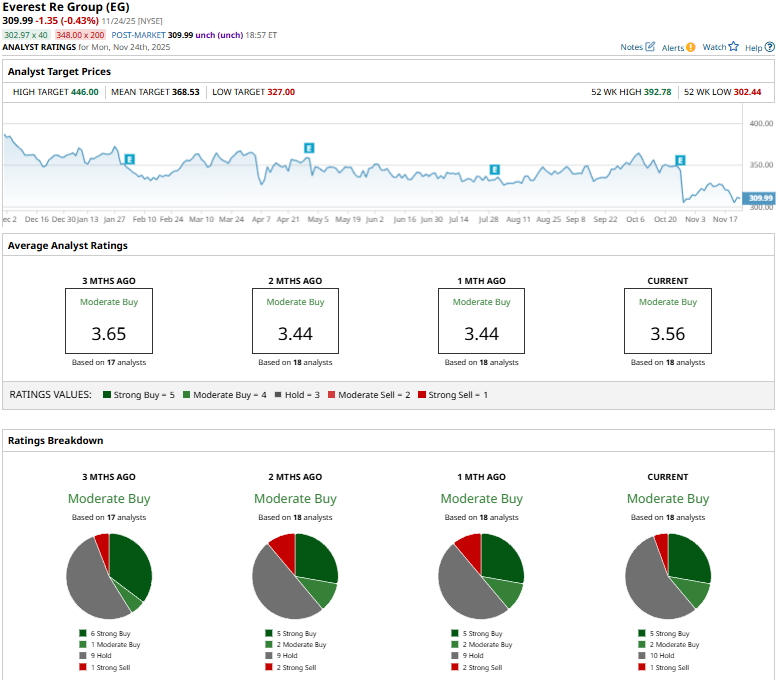

Among the 18 analysts covering the EG stock, the consensus rating is a “Moderate Buy.” That’s based on five “Strong Buys,” two “Moderate Buys,” 10 “Holds,” and one “Strong Sell.”

This configuration is slightly more optimistic than a month ago, when two analysts gave “Strong Sell” recommendations.

On Oct. 24, Keefe, Bruyette & Woods analyst Meyer Shields maintained an “Outperform” rating on EG, but lowered the price target from $424 to $400.

As of writing, Everest Group’s mean price target of $368.53 represents an 18.9% premium to current price levels. Meanwhile, the street-high target of $446 suggests a 43.9% upside potential.

On the date of publication, Aditya Sarawgi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart