Let’s dig into the relative performance of Avnet (NASDAQ:AVT) and its peers as we unravel the now-completed Q3 it distribution & solutions earnings season.

IT Distribution & Solutions will be buoyed by the increasing complexity of IT ecosystems, rising cloud adoption, and demand for cybersecurity solutions. Enterprises are less likely than ever to embark on these complicated journeys solo, and companies in the sector boast expertise and scale in these areas. However, cloud migration also means less need for hardware, which could dent demand for large portions of the product portfolio and hurt margins. Additionally, planning for potentially supply chain disruptions is ongoing, as the COVID-19 pandemic showed how damaging a pause in global trade could be in areas like semiconductor procurement.

The 8 it distribution & solutions stocks we track reported a satisfactory Q3. As a group, revenues beat analysts’ consensus estimates by 1.3% while next quarter’s revenue guidance was in line.

While some it distribution & solutions stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 2.4% since the latest earnings results.

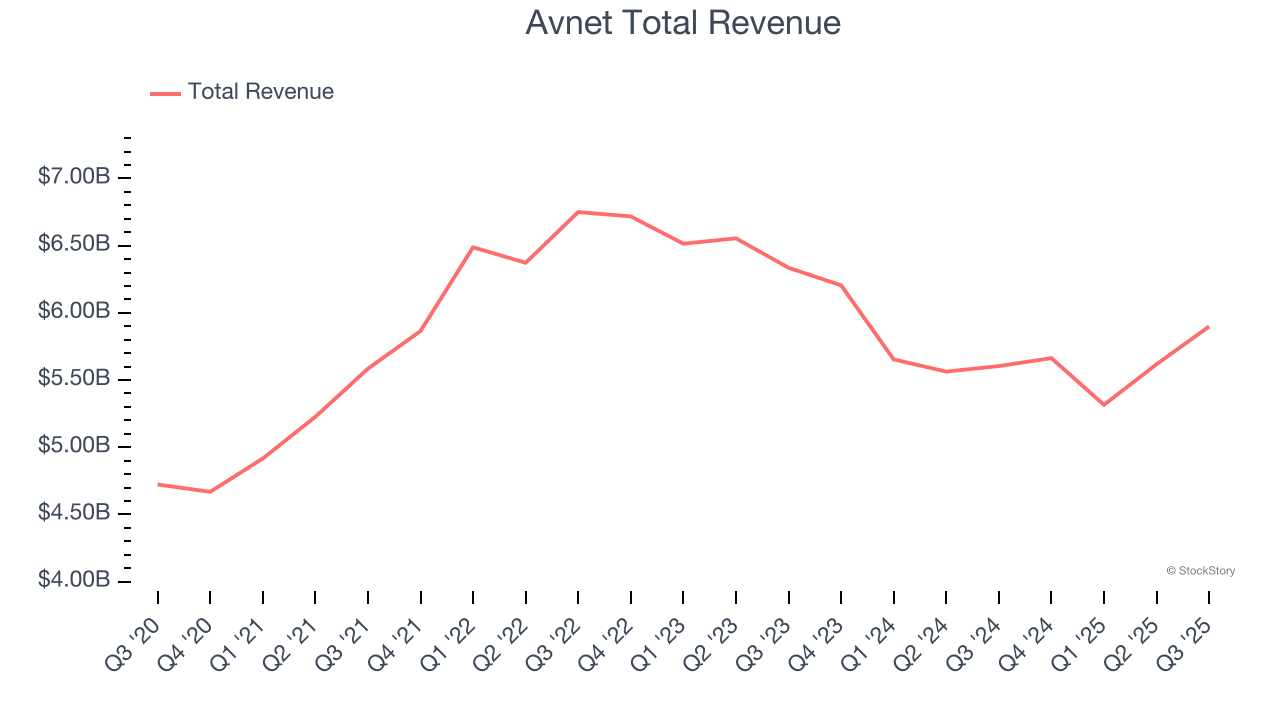

Avnet (NASDAQ:AVT)

With a century-long history of adapting to technological evolution, Avnet (NASDAQ:AVT) is a global electronic components distributor that connects manufacturers of semiconductors and other electronic parts with businesses that need these components.

Avnet reported revenues of $5.90 billion, up 5.3% year on year. This print exceeded analysts’ expectations by 3%. Overall, it was a strong quarter for the company with revenue guidance for next quarter exceeding analysts’ expectations and an impressive beat of analysts’ revenue estimates.

“In the first quarter, our sales and earnings exceeded our expectations, led by double-digit year-over-year sales growth in Farnell and Asia,” said Avnet Chief Executive Officer Phil Gallagher.

Unsurprisingly, the stock is down 6.2% since reporting and currently trades at $47.40.

Is now the time to buy Avnet? Access our full analysis of the earnings results here, it’s free for active Edge members.

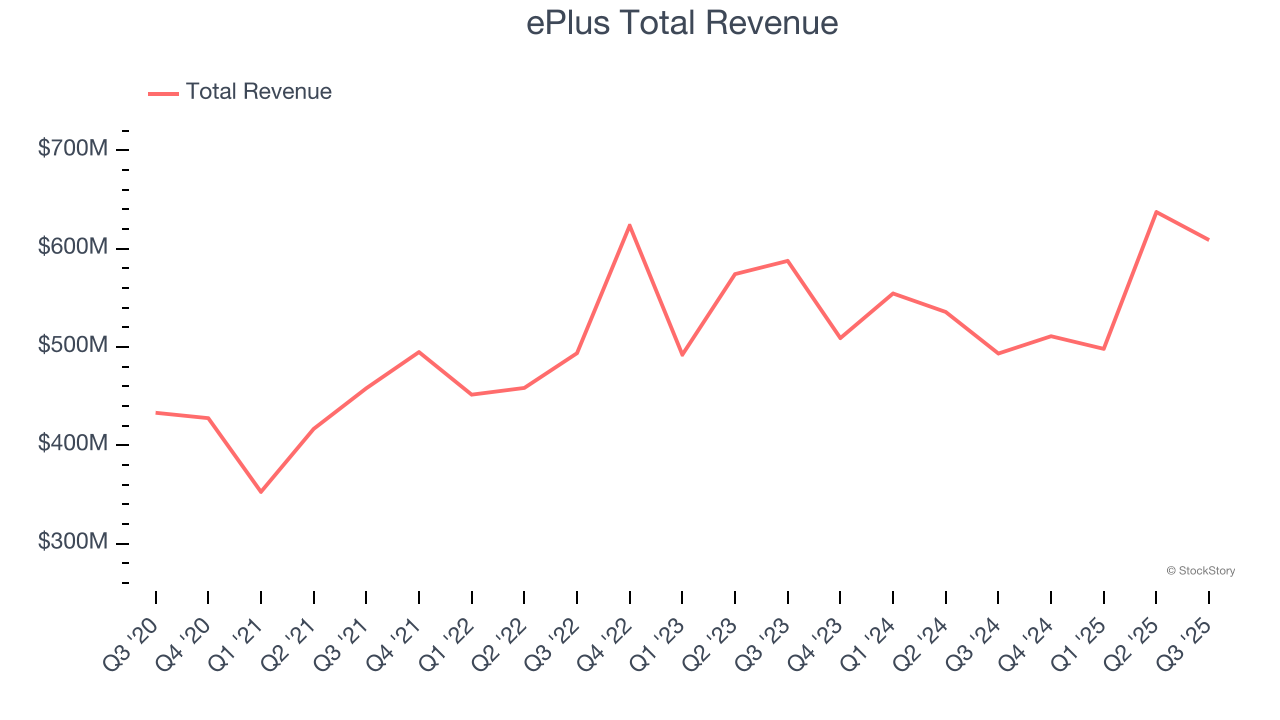

Best Q3: ePlus (NASDAQ:PLUS)

Starting as a financing company in 1990 before evolving into a full-service technology provider, ePlus (NASDAQ:PLUS) provides comprehensive IT solutions, professional services, and financing options to help organizations optimize their technology infrastructure and supply chain processes.

ePlus reported revenues of $608.8 million, up 23.4% year on year, outperforming analysts’ expectations by 17.5%. The business had an incredible quarter with a beat of analysts’ EPS estimates and a solid beat of analysts’ revenue estimates.

ePlus scored the biggest analyst estimates beat and fastest revenue growth among its peers. The market seems happy with the results as the stock is up 19.5% since reporting. It currently trades at $87.67.

Is now the time to buy ePlus? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: Connection (NASDAQ:CNXN)

Starting as a small computer products seller in 1982 and evolving into a Fortune 1000 company, Connection (NASDAQ:CNXN) is a technology solutions provider that helps businesses and government agencies design, purchase, implement, and manage their IT infrastructure and systems.

Connection reported revenues of $709.1 million, down 2.2% year on year, falling short of analysts’ expectations by 4.7%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue estimates and a significant miss of analysts’ EPS estimates.

As expected, the stock is down 4.4% since the results and currently trades at $58.20.

Read our full analysis of Connection’s results here.

TD SYNNEX (NYSE:SNX)

Serving as the crucial middleman in the technology supply chain, TD SYNNEX (NYSE:SNX) is a global technology distributor that connects thousands of IT manufacturers with resellers, helping businesses access hardware, software, and technology solutions.

TD SYNNEX reported revenues of $15.65 billion, up 6.6% year on year. This print beat analysts’ expectations by 3.5%. Overall, it was a stunning quarter as it also logged a beat of analysts’ EPS estimates and a solid beat of analysts’ EPS guidance for next quarter estimates.

The stock is flat since reporting and currently trades at $151.69.

Read our full, actionable report on TD SYNNEX here, it’s free for active Edge members.

Ingram Micro (NYSE:INGM)

Operating as the crucial link in the global technology supply chain with a presence in 57 countries, Ingram Micro (NYSE:INGM) is a global technology distributor that connects manufacturers with resellers, providing hardware, software, cloud services, and logistics expertise.

Ingram Micro reported revenues of $12.6 billion, up 7.2% year on year. This result surpassed analysts’ expectations by 3%. It was a strong quarter as it also recorded revenue guidance for next quarter exceeding analysts’ expectations and a solid beat of analysts’ revenue estimates.

The stock is down 3% since reporting and currently trades at $21.40.

Read our full, actionable report on Ingram Micro here, it’s free for active Edge members.

Market Update

In response to the Fed’s rate hikes in 2022 and 2023, inflation has been gradually trending down from its post-pandemic peak, trending closer to the Fed’s 2% target. Despite higher borrowing costs, the economy has avoided flashing recessionary signals. This is the much-desired soft landing that many investors hoped for. The recent rate cuts (0.5% in September and 0.25% in November 2024) have bolstered the stock market, making 2024 a strong year for equities. Donald Trump’s presidential win in November sparked additional market gains, sending indices to record highs in the days following his victory. However, debates continue over possible tariffs and corporate tax adjustments, raising questions about economic stability in 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.