What a fantastic six months it’s been for Compass. Shares of the company have skyrocketed 101%, hitting $7.09. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Compass, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.We’re happy investors have made money, but we don't have much confidence in Compass. Here are three reasons why COMP doesn't excite us and a stock we'd rather own.

Why Is Compass Not Exciting?

Fueled by its mission to replace the "paper-driven, antiquated workflow" of buying a house, Compass (NYSE:COMP) is a digital-first company operating a residential real estate brokerage in the United States.

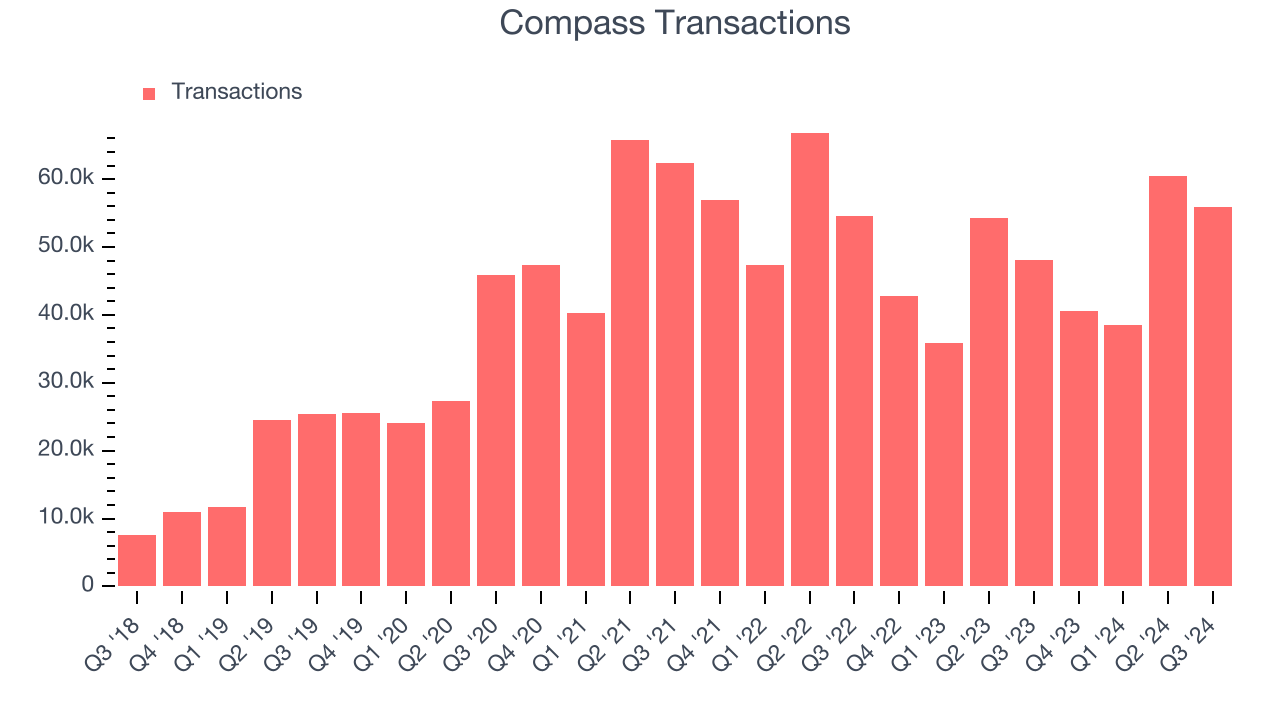

1. Decline in Transactions Points to Weak Demand

Revenue growth can be broken down into changes in price and volume (for companies like Compass, our preferred volume metric is transactions). While both are important, the latter is the most critical to analyze because prices have a ceiling.

Compass’s transactions came in at 55,872 in the latest quarter, and over the last two years, averaged 6.3% year-on-year declines. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Compass might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

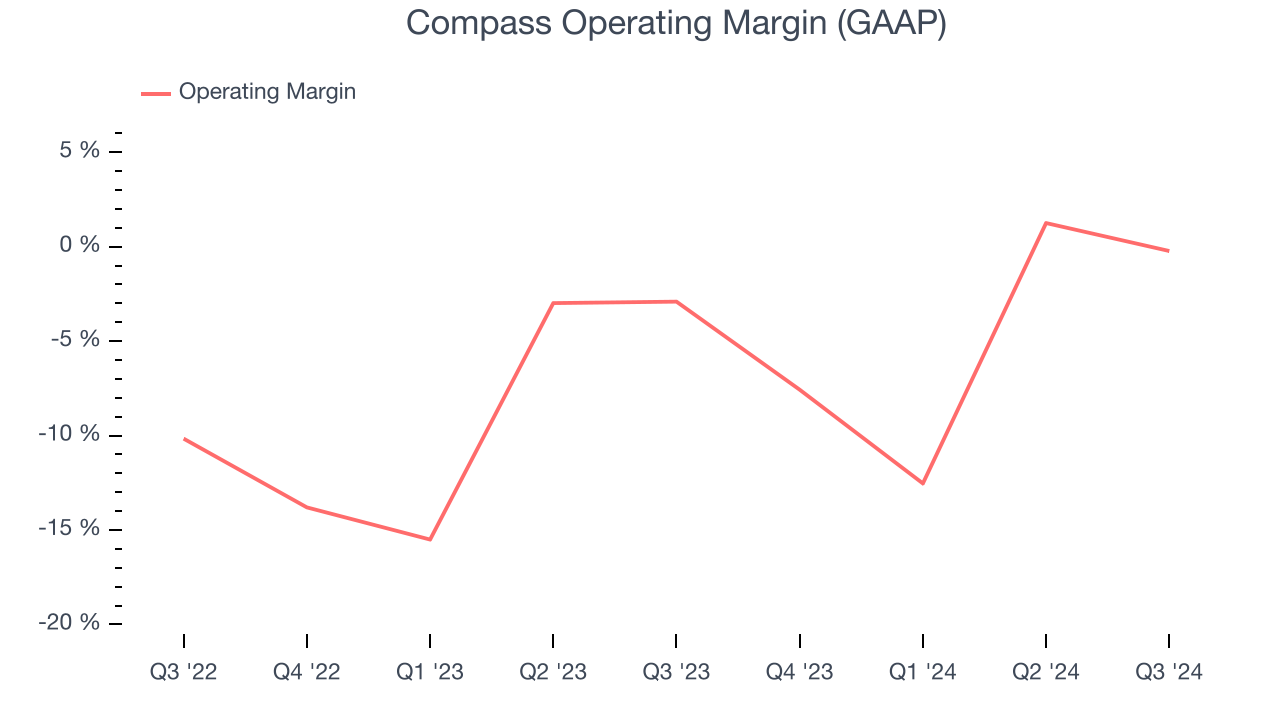

2. Operating Losses Sound the Alarms

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Compass’s operating margin has risen over the last 12 months, but it still averaged negative 5.7% over the last two years. This is due to its large expense base and inefficient cost structure.

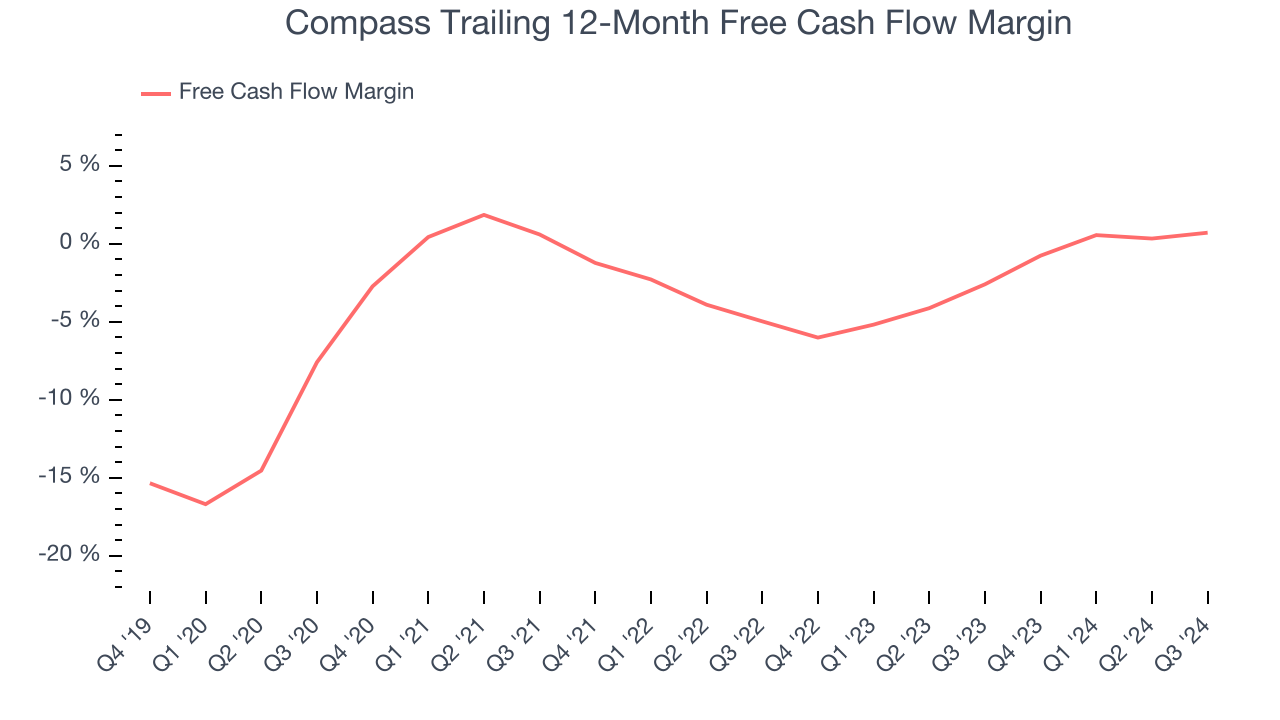

3. Breakeven Free Cash Flow Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Compass broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

Final Judgment

Compass isn’t a terrible business, but it doesn’t pass our quality test. Following the recent rally, the stock trades at 16.8× forward EV-to-EBITDA (or $7.09 per share). At this valuation, there’s a lot of good news priced in - we think there are better opportunities elsewhere. We’d suggest looking at Wabtec, a leading provider of locomotive services benefiting from an upgrade cycle.

Stocks We Like More Than Compass

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.