As the craze of earnings season draws to a close, here’s a look back at some of the most exciting (and some less so) results from Q3. Today, we are looking at travel and vacation providers stocks, starting with American Airlines (NASDAQ:AAL).

Airlines, hotels, resorts, and cruise line companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted from buying "things" (wasteful) to buying "experiences" (memorable). In addition, the internet has introduced new ways of approaching leisure and lodging such as booking homes and longer-term accommodations. Traditional airlines, hotel, resorts, and cruise line companies must innovate to stay relevant in a market rife with innovation.

The 16 travel and vacation providers stocks we track reported a satisfactory Q3. As a group, revenues beat analysts’ consensus estimates by 1.2% while next quarter’s revenue guidance was 0.9% below.

Luckily, travel and vacation providers stocks have performed well with share prices up 12% on average since the latest earnings results.

American Airlines (NASDAQ:AAL)

One of the ‘Big Four’ airlines in the US, American Airlines (NASDAQ:AAL) is a major global air carrier that serves both business and leisure travelers through its domestic and international flights.

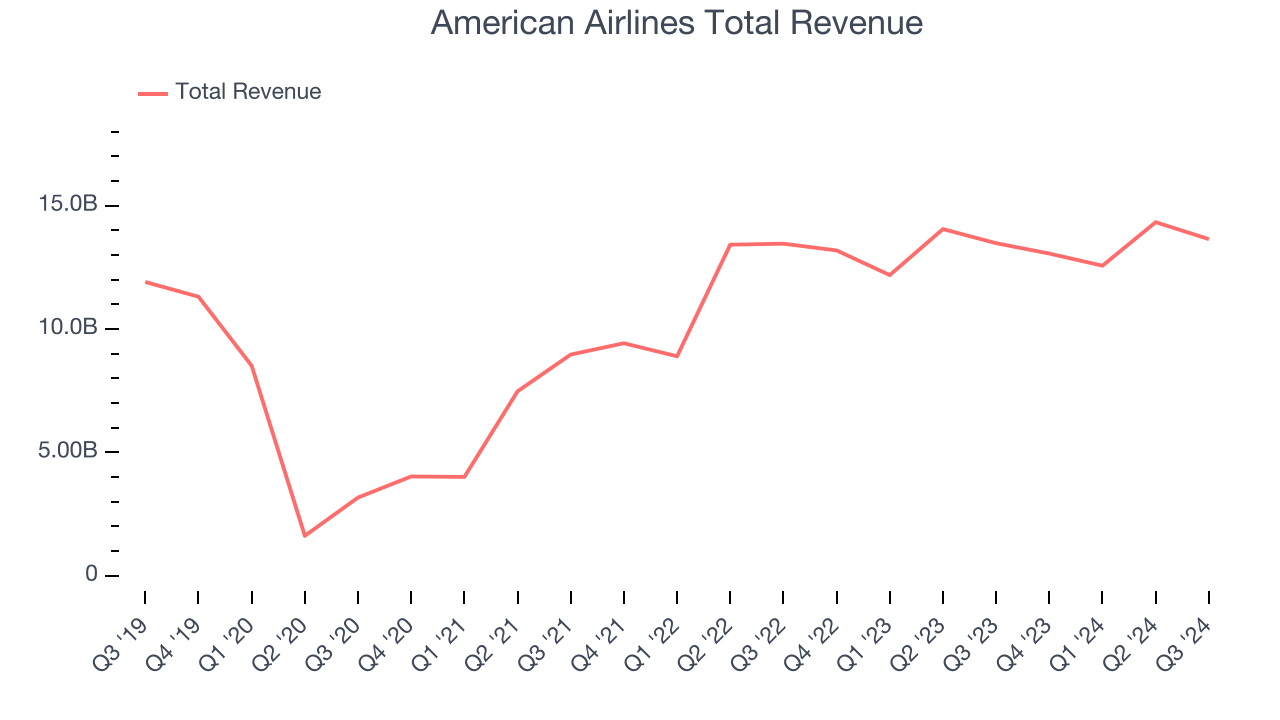

American Airlines reported revenues of $13.65 billion, up 1.2% year on year. This print exceeded analysts’ expectations by 0.5%. Overall, it was a very strong quarter for the company with a solid beat of analysts’ EPS estimates and full-year EPS guidance exceeding analysts’ expectations.

“The American Airlines team continues to focus on running a reliable operation and managing costs across the airline,” said American’s CEO Robert Isom.

Interestingly, the stock is up 10.9% since reporting and currently trades at $14.25.

Is now the time to buy American Airlines? Access our full analysis of the earnings results here, it’s free.

Best Q3: Playa Hotels & Resorts (NASDAQ:PLYA)

Sporting a roster of beachfront properties, Playa Hotels & Resorts (NASDAQ:PLYA) is an owner, operator, and developer of all-inclusive resorts in prime vacation destinations.

Playa Hotels & Resorts reported revenues of $183.5 million, down 13.9% year on year, outperforming analysts’ expectations by 4.1%. The business had a stunning quarter with an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

The market seems happy with the results as the stock is up 6.5% since reporting. It currently trades at $9.60.

Is now the time to buy Playa Hotels & Resorts? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Sabre (NASDAQ:SABR)

Originally a division of American Airlines, Sabre (NASDAQ:SABR) is a technology provider for the global travel and tourism industry.

Sabre reported revenues of $764.7 million, up 3.3% year on year, falling short of analysts’ expectations by 1.4%. It was a slower quarter as it posted a significant miss of analysts’ EPS estimates and EBITDA guidance for next quarter missing analysts’ expectations.

Sabre delivered the weakest full-year guidance update in the group. As expected, the stock is down 16.5% since the results and currently trades at $3.44.

Read our full analysis of Sabre’s results here.

Delta Air Lines (NYSE:DAL)

One of the ‘Big Four’ airlines in the US, Delta Air Lines (NYSE:DAL) is a major global air carrier that serves both business and leisure travelers through its domestic and international flights.

Delta Air Lines reported revenues of $15.68 billion, up 1.2% year on year. This result beat analysts’ expectations by 2.5%. Aside from that, it was a satisfactory quarter as it also produced an impressive beat of analysts’ EPS and EBITDA estimates.

The stock is up 26.3% since reporting and currently trades at $64.40.

Read our full, actionable report on Delta Air Lines here, it’s free.

Carnival (NYSE:CCL)

Boasting outrageous amenities like a planetarium on board its ships, Carnival (NYSE:CCL) is one of the world's largest leisure travel companies and a prominent player in the cruise industry.

Carnival reported revenues of $7.90 billion, up 15.2% year on year. This result topped analysts’ expectations by 1%. More broadly, it was a mixed quarter as it also logged a decent beat of analysts’ adjusted operating income estimates but EBITDA guidance for next quarter missing analysts’ expectations.

The stock is up 30.5% since reporting and currently trades at $24.20.

Read our full, actionable report on Carnival here, it’s free.

Market Update

Thanks to the Fed's series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market has thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.